Mirror, Signal, Outmanoeuvre

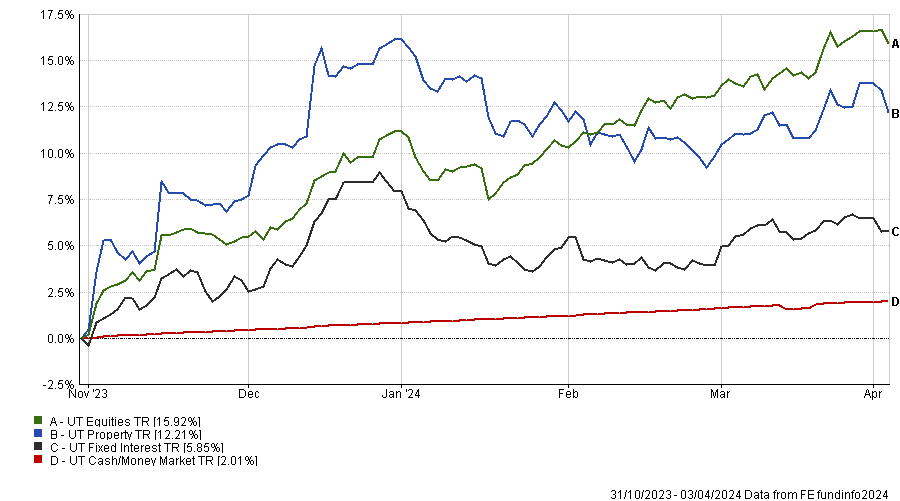

This update covers the period Q1 of 2024, but in many cases we have taken the basic asset class chart (fig.1) back to the end of October last year. With hindsight, we can now say with certainty that this was a market inflexion point. Risk assets have performed well to varying degrees since Powell appeared to waive the victory flag in their belated attempts to address the inflation issue they thought didn’t exist.

Despite geopolitical events, diverging economic prospects, and individual country idiosyncrasies, the central banks, led by the Fed, continue to dictate market movements.

Asset Class Performance Since the Last Powell Pivot* (fig.1)

Macro

Unfortunately, it’s not just the Fed press conferences that are seen by some as shining a light on future interest rate policy. The markets also have to cope with the blizzard of ‘Fed speak’, some days as many as half a dozen members will procrastinate about monetary policy. As an example, this week, Neil Kashkari opined, “If we continue to see inflation moving sideways, then that would make me question whether we need to do those rate cuts at all?” Later on saying that if current rates were insufficient to remain strong, further rate rises were “not off the table, but they are also not a likely scenario given what we know right now”.

Firstly, Mr Kashkari has said nothing we didn’t already know. Secondly, though he is not even a voting member of the Fed right now, it didn’t stop the US markets moving directly into the red and closing down 1.2% for the day. Currently, the Fed is leading markets by the nose, and their messaging will get increasingly complicated as we move towards the November US election. To quote Mickey Rourke in the film “Rumble Fish – “If you’re going to lead people, you have to have somewhere to go“. Right now, we are not sure even they really know where they are going, and still less, how they might get there.

In answering the question this week on the “what will be the equilibrium (neutral) interest rate?” The Fed Chair said “it doesn’t really matter for policy today.” This was something Havards Larry Summers described later as “a mistake”.

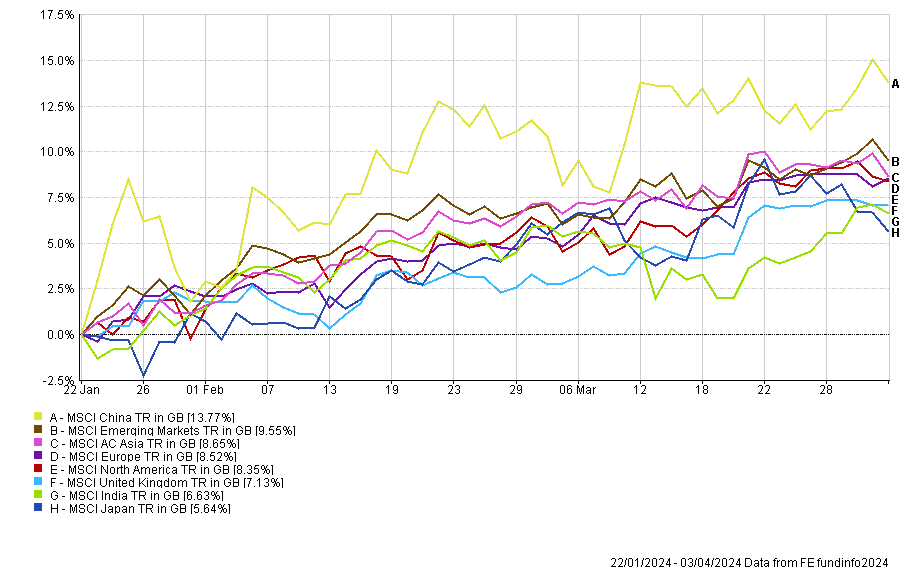

However, despite North America continuing to dominate the headlines, 2024 has been characterised by a geographically more broad-based rally, especially since 22nd January (fig.2). This is when China appears to have convinced sufficient investors that the worst may be over for the stock markets of the world’s second-largest economy. This time, the more buoyant Chinese markets appear to be due to many individual incremental changes by the government and central bank, whilst several pieces of economic data have finally surprised to the upside.

Listening to the financial media in the last few weeks, we no longer, with due solemnity, hear the word ‘uninvestable’ being pronounced when it comes to China. This has been replaced with words like opportunistic, cheap, attractive, etc.

Geographical Performance Since 22nd January* (fig.2)

Portfolio Performance & Positioning

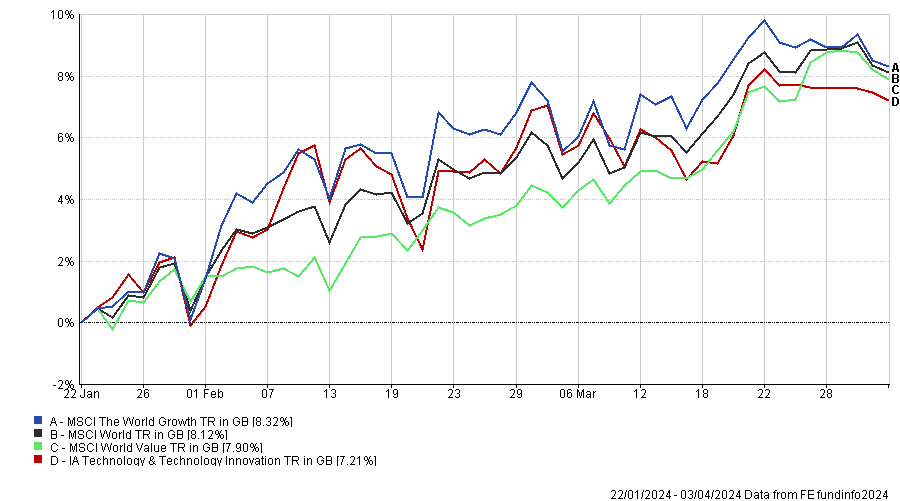

Another, potentially significant, market development is that we are seeing an increase in growth and value correlations, and that tech is no longer outperforming them as a high beta play on the growth style. In this admittedly short-term period (fig.3), one observation is that the recent winners appear to be high-conviction active stock pickers rather than passive vehicles.

Growth Versus Value

Growth Versus Value Performance Since 22nd January* (fig.3)

The predictive powers in 1, 3, and 5-year data

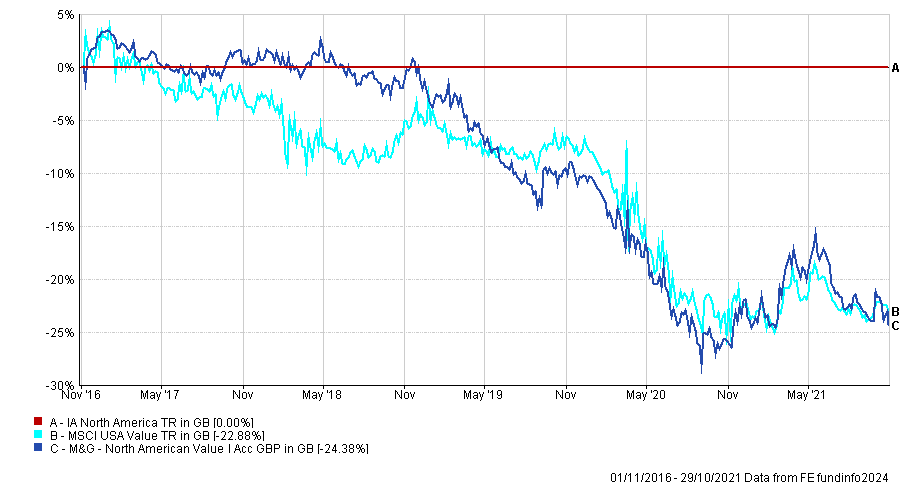

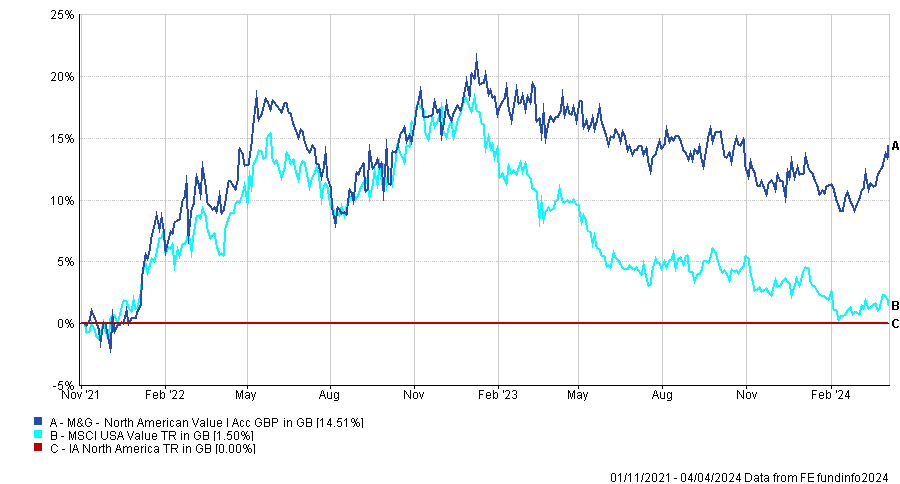

One of the ways active managers can add value (or not destroy it) is to know when they can potentially outperform within a style or a sub-index and when the odds are stacked against them. One of our successful fund picks has been the M&G North American Value fund, which we introduced in November 2021. This is an example of why looking at 1, 3, and 5-year cumulative data is unhelpful in determining which managers will outperform going forward.

The charts (fig.4.1 & 4.2) show the performance of the M&G fund and the US Value sector relative to the IA North America sector before we brought it in and in the subsequent period thereafter; there is little in this graph that might have indicated what was to happen.

Our decision to include this fund was basically for two reasons – firstly, value-style stocks were extremely out of favour and reminded us of the period at the end of the nineties. Secondly, there are notoriously high-value traps within this investing style, and we wanted an active manager who could potentially pick through the stocks and find the winners. The manager, Daniel White, has shown he knows how to execute both parts of what we sought.

M&G North American Value vs. MSCI USA Value & IA Noth America Relative Performance > 01/11/2016- 29/10/2021 (fig.4.1)

M&G North American Value vs. MSCI USA Value & IA Noth America Relative Performance > 01/11/2021- 04/04/2024* (fig.4.2)

Outperformance in rising markets

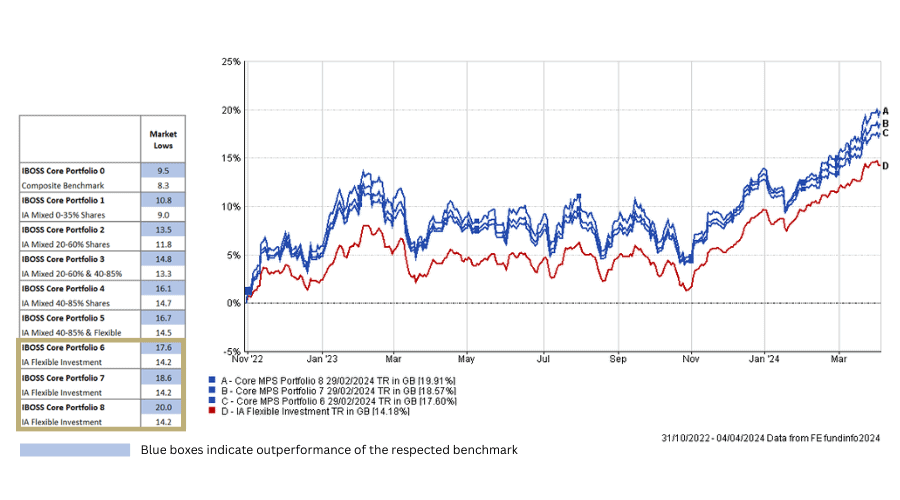

IBOSS Core MPS returns since the market lows – 31/10/2022 – 04/04/2024*

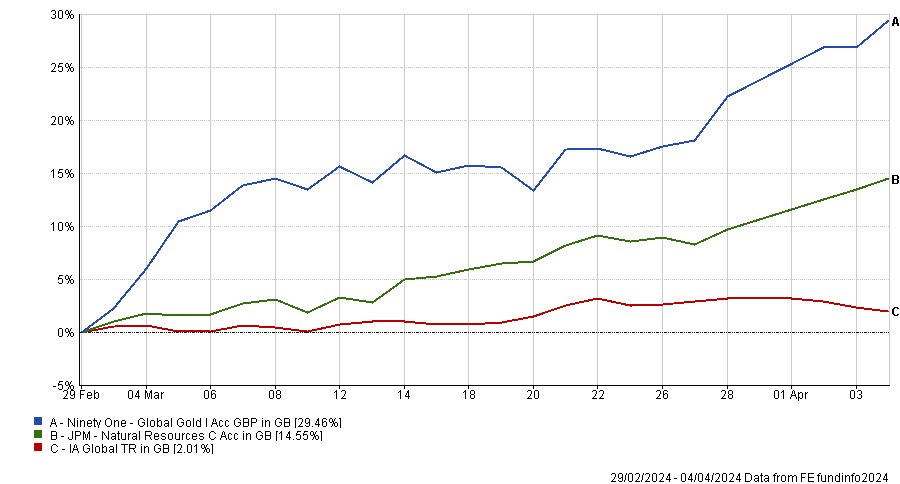

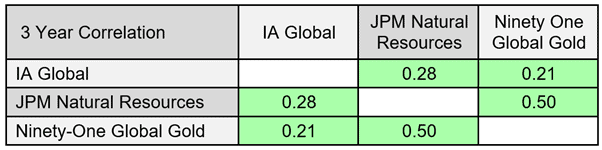

The portfolios have benefitted strongly from their high levels of diversification since the market lows of October 2022. The standout performers since the beginning of March have been the gold and commodities funds, and our active managers continue to add alpha more broadly. A primary reason for holding the Ninety One and JPM funds is their low correlation to global equities, as seen in the table (fig.6).

Gold & Commodities > 29/02/2024 – 04/04/2024* (fig.6)

![]()

Elsewhere in equities, the higher conviction active managers are adding the most relative and currently absolute value. Particular standouts in the UK are Artemis UK Select, the number one fund in the IA UK All Cos sector over most periods, a resurgent Polar Capital UK Value Opportunities, and Man GLG Income fund.

In the bond space, Royal London UK Government Bond continues to perform well in very tricky sovereign markets. In the corporate and strategic sectors, Rathbone Ethical Bond and L&G Strategic Bond have again been out in top decile performance since the beginning of March. Complimenting the strong UK funds is the M&G Emerging Markets Bond fund, which has been the number one fund in its sector over the last seven years and continues to add non-correlated alpha to our fixed-income position.

Investor Outlook

While many risk assets are undeniably expensive relative to their own histories, there are still investment sectors that remain attractive and, in the case of commodities, for unfortunate reasons. As geopolitics continues to flare up worldwide, we must also deal with poor and naive investment decisions made in the last few decades in areas such as energy. We can still find opportunities in every asset class, but in current market conditions, we favour the best active managers’ opportunities over their passive peers.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 83.4.24