As managers of multi-asset portfolios, we have long preached the benefits of diversification. The problem is, as growth stocks have been on a tear for the last decade, being properly diversified has actually been a headwind for managers like ourselves.

Entering a New World

However, as global economies reopen post-Covid and following a wave of interest rate rises across the globe in an effort to combat inflation, it’s our belief we are entering a new world in which being properly diversified has never been more important.

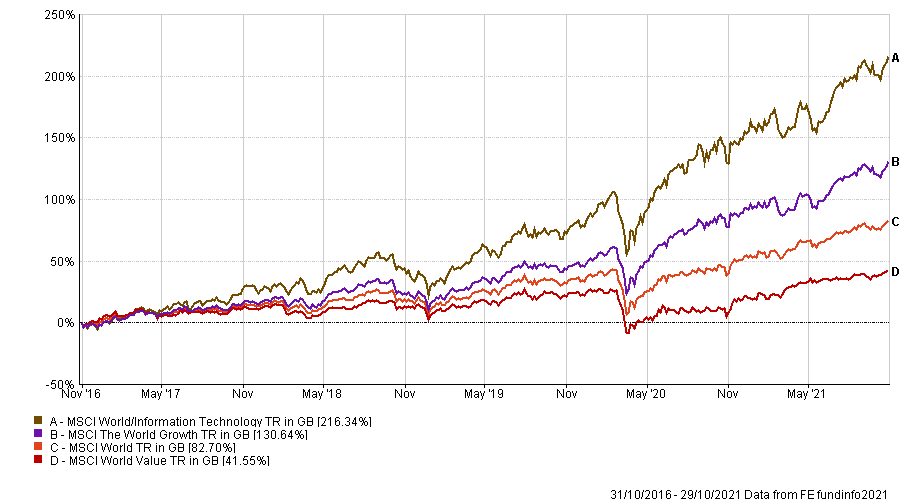

A quick look at the numbers shows just how much things have changed. Over five years, the direction of travel for technology and growth stocks has been on a clear line upwards, whereas a value style has underperformed (see chart below).

5 Year Performance line to 29th October 2021

These areas were driven forwards from the ‘lower for ever’ interest rate regimes and, pre-vaccines, were huge beneficiaries of the staying at home trade. However, these two tailwinds changed almost at the same time. As a result, those areas that worked spectacularly well before may be less likely to do so going forward unless large sections of the global economy go back into hard lockdown.

Do Investors Appreciate what is Happening?

Our concern is that investors do not fully appreciate that what we are witnessing is a fundamental shift, which requires a change in mindset. Whether it’s the US, Europe, or GEM equity, growth investing is under pressure for the first time since the infamous Powell Pivot in Q4 2018. This is because tech and growth stocks are vulnerable to rate rises and changes in support from the global central banks.

So, what can we do as investors in this brave new world? Firstly, it’s not about having growth or value. It’s all about blending the two styles and finding true active managers who can do both. Based on our ongoing concerns about the growth styles adopted by both the Baillie Gifford and BlackRock emerging markets funds, in February this year, we introduced the Stewart Investors GEM Leaders fund into our Core MPS.

In May we also added the Schroder Global Recovery, JPM Natural Resources and Janus Henderson European Focus funds, while we reduced our exposure to the Premier Miton European fund, which had performed very well.

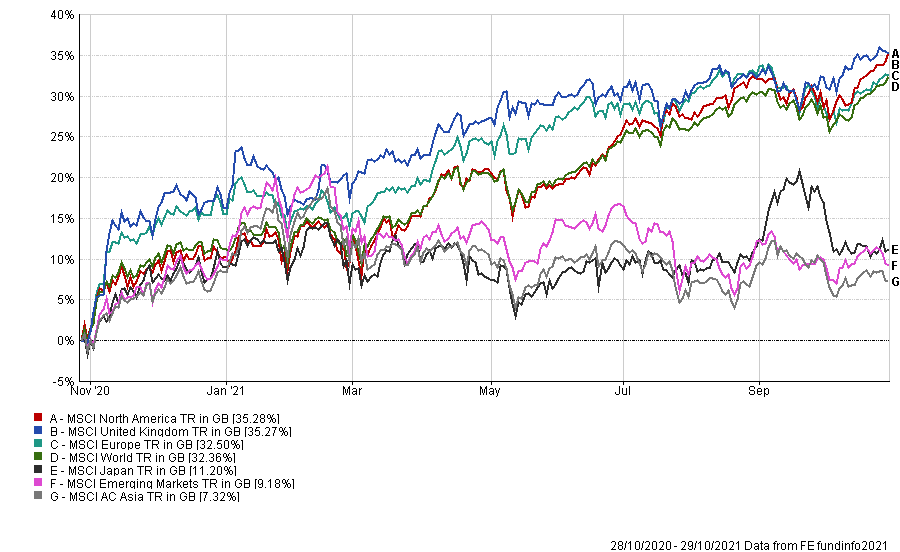

The shift in direction has also led us to be more bullish on the UK, which given its weighting in oil, banks, and miners, has been a region left behind in the last decade. However, these are all the areas which should benefit in the new world, and since the 28th October, the UK has been one of the best performing regions globally (see chart below).

Geographical Performance – 28/10/2020 -29/10/2021

Indeed, while we usually have tracker funds in most areas, we currently have none in the UK given the investment opportunities for UK active managers. The same is true of active managers in Europe, GEM, and to an extent, the US. You also need those active managers who will be brave enough to invest in politically sensitive countries such as Russia.

Diversification is Key

In short, as the FCA always preaches, past performance is no guide as to what will work in the future. But never has this been more so today. In each region we are making sure we have a blend of all styles, both growth and value, to make sure we are as diversified as we have ever been.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same Group, METNOR Group Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 374.11.21