Fools Gold?

It has been a while since we last discussed Gold having introduced the precious metal into our MPS portfolios in November 2017. At the time gold was largely ignored in favour of Bitcoin which haunted the lips and minds of investors everywhere and seemed to many to be a superior store of value. As we now know, the height of Bitcoin mania ended in a violent shudder as the crypto currencies value fell 73% from its $20k December 2017 high. Years later and Bitcoin now trades, rather pedestrianly and neatly flat relative to its November 2017 price. The Journey for Bitcoins shinier, older, and once less popular sibling has been different but in some ways no less spectacular. The price of gold remained relatively stable until the run up to the, now infamous, Powell pivot (Q4 2018). Since then it has largely provided non-correlated returns in an environment where such things are increasingly hard to come by.

The Journey of Gold

Powell Sticks to his Guns (30.09.2018 – 24.12.2018): Gold +9.09% Equities -15.07%

Jerome Powell, at that time recently elected head of the Federal Reserve, indicated to markets that they were to begin the process of removing central bank support, he even uttered the dreaded word “normalisation”. Markets reacted strongly; equities fell aggressively. Throughout the confusion, Gold outperformed not only equities but Fixed Income as well.

Powell Pivots (24.12.2018 – 01.04.2019): Gold -1.90% Equities +15.07%

Following such a severe market reaction J. Powell enacted a monumental U-turn and indicated that the Fed was not in fact going anywhere. The renewed Central Bank support elevated markets back to their previous heights by April 2019 during which period gold largely retained its value.

Coronavirus Crash & Recovery (20.02.2020 – 23.03.2020): Gold +13.69% Equities -2.83%

Once again, the price of gold demonstrated resilience in a period where equity markets were under substantial and understandable pressure falling, on average, 25.66%. Despite this, equity markets very quickly began to look through the coronavirus concerns and concentrate on the massive stimulus from the US government and the Fed. This was replicated in many places across the globe. Panic was quickly replaced with a bout of FOMO (fear of missing out) we joined in on this new found optimism following the market falls in our webinar in March where we declared we were more bullish on equities than we had been for over a decade. We also remained bullish on gold as bond yields were flattening, and debt was growing exponentially.

Gold Miners – do they offer the same benefits?

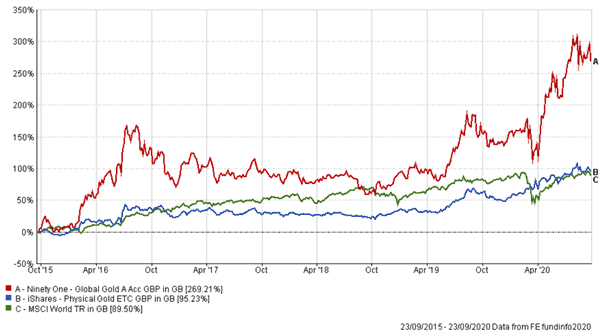

It is more difficult to gain exposure to Physical gold through the MPS and because of this each of the MPS portfolios holds a 1% position in the Ninety-One Gold fund. This fund predominantly holds a selection of Gold Miners which are publicly traded equities and are often correlated with equity markets over the short term. However, over longer periods Gold equities do exhibit a low correlation to wider markers, and a higher correlation to Physical Gold.

As you can see in the chart below, the Gold Equity journey is substantially more volatile than physical Gold, and although the correlation between Gold spot and the Ninety-One fund is meaningful, the magnitude of movements is much more severe. Therefore, and despite the benefits in times of market stress, we feel that only a small holding in Gold miners is enough to make a meaningful impact on portfolio returns.

Gold & Equity Performance – 5 Years to 23.09.2020

Where does Gold go from here?

Gold has come a long way since we introduced the asset into our portfolios, and with the Ninety One Gold fund having risen 42% this year alone the question as to whether we should sell the position is an obvious one. It is our view that despite the stronger performance of Gold miners and physical gold there are still many enduring positive factors. Firstly, the traditional argument against gold is it inability to produce a yield – this continues to be greatly diminished considering that Central bankers strive to keep bond yields low. Secondly, the huge amount of stimulus issued by both Central Banks and governments could further erode the value of fiat money. In this situation Gold acts as a store of Value. Finally, these assets continue to provide a source of diversification in a world where diversifying assets are ever harder to come by. In short, we will continue to maintain our position across IBOSS products, probably until central banks change course and that is a considerable time away.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients.

The MPS range portfolio performance is produced using the preferred share classes, this may differ from platform to platform.

The MPS range is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 280.9.20