This year, investors’ returns have come under significant pressure as bonds and equities have experienced an unprecedented and simultaneous fall in value. As this situation becomes more prolonged and pronounced, it is only natural that clients become nervous and ask increasingly complex investment questions.

We have collated these and shared our top four ghoulish client questions following a very scary month in what has been, for many investors, a particularly frightening year.

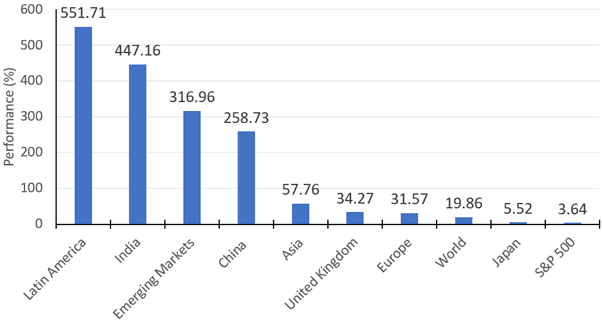

“What is the possibility of the markets going down and never recovering, or staying low for an extended period?”

Individual investment styles, regions, or assets can suffer prolonged periods of underperformance. One of the most famous examples is the “Lost Decade”, which saw the S&P 500 between 2000 and 2010 produce an annualised return of -0.95%. However, over the same period, we saw other equities perform well, with emerging markets annualising a return of 9.78%, highlighting the need to remain diversified as long-term investors.

We have put together the chart below demonstrating the majority of the period; however (due to the length of data available), the chart ranges from 2001 and 2010 rather than from 2000.

Regional performance from 2001 – 2010 using MSCI Indices

“Markets look plagued with uncertainty and volatility, how is the outlook for inflation affecting them?”

Though the performance of bonds appears to make for rather depressing reading, it is worth considering that some fixed income assets are trading at much more attractive levels, which already reflect an environment of more persistent inflation. Nobody knows where these levels ultimately settle (though everybody has an opinion), but we believe they will remain higher for longer than central banks admit.

Regarding positioning, we remain meaningfully underweight government bonds, but have begun incrementally allocating to high-quality sovereign bonds to take advantage of the more attractive valuations.

In equities, we believe energy will remain a crucial factor in the returns for many sectors and companies. Russia’s war with Ukraine will undoubtedly impact prices and supply, but the energy crisis in Europe was years in the making and cannot be rectified in a few months. This being the case, exposure to physical assets within the portfolio should benefit medium, and longer-term returns. Still, as always with such assets, they will have periods of heightened volatility. However, we must be conscious that the Fed will inevitably pivot. When this occurs, many digital assets that had performed well in recent years could well do so again, especially considering many are coming from distressed valuations. In short, the range of outcomes from here is as extensive as ever.

At the beginning of the year, bonds and growth-like equities looked more expensive than they have for many years, but this is no longer true. As such, we caution against taking too strong a position in any one area and instead focus on ensuring that your investments are as diversified as possible.

Though we are in an environment plagued with uncertainty and volatility, we believe it also presents a significant opportunity for investors with a three to five-year time horizon, as opposed to a three to five-month one. Potentially, the real risk here is being overly concentrated in a specific asset or region – something that has been the undoing of some managers with overweights in government bonds from the start of the year.

“Passive funds have been killing active strategies this year, what is your view on the active versus passive debate?”

We have tackled this query with respect to our MPS Core range, which can hold both active and passive funds.

Our fundamental approach to the active versus passive debate is that they both offer potentially distinct benefits in different situations. Therefore, we always start with the balance of probability test, which is effectively: ‘do we think a given active fund can outperform a passive alternative net of fees provided the market conditions?’ So, the use of passive funds tends to ebb and flow over time, given the market conditions.

There are also situations where we want to keep a greater degree of control. For example, in the last few weeks, we have increased the duration of our bond allocation, and we have done this via the Vanguard US Government Bond Index (Hedged). This gives us a high degree of certainty about the asset make-up, duration and currency. We blend several funds together in each sector, and if we used purely active managers, we would have limited visibility of the overall make-up of portfolios.

We currently use roughly 75% active and 25% passive weighting within our equity allocation. It’s imperative to understand what a passive vehicle is tracking when it will do well, and when it will struggle. We use the L&G US Index Trust, which closely follows the S&P500 and is very growth orientated, so we know what to expect from it. We currently pair this with the active M&G North America Value fund. These funds have little commonality, but it’s the M&G fund that can take advantage of market volatility. The manager had indeed benefitted from buying value assets before the Fed realised that inflation wasn’t transitory and, in fact, is now the biggest issue facing the US economy.

In the coming months, we expect to add further to active funds as we see new opportunities opening up in the fixed income sector. This will bring to an end our extremely short-duration position which we managed via passive funds and has helped protect capital for our lower-risk clients.

It is worth noting that passive funds have gone through one of their best performance periods, having outperformed most active strategies this year (IBOSS portfolios included). A large part of this is due to the strength of the dollar and the fact that large companies have outperformed mid/small cap equities.

What recent trades/changes have you done to reflect opportunities and outlook?

The US, buoyed recently by a strong dollar, has been the stand-out performer of the last decade, so much so that investors have been holding increasingly concentrated positions in these names. As a result, we contend that the most significant risk to investors is investing based on the rear-view mirror.

As such, we have looked to ensure that portfolios have a diverse holding of regions, styles and assets. This approach should allow the portfolios to make returns over the long term, irrespective of whether any singular style falls out of favor for an extended period, as per the lost decade.

In the last decade (pre-December 2021), risk asset returns were made against a backdrop of “lower for longer” interest rates, but that period is now very much in the past. Therefore, the portfolios are exposed, or are becoming more exposed to areas we feel present the most attractive opportunities in the new era, including;

- UK equities, which are trading at historically low valuations.

- Chinese equities have faced headwinds for much of the last two years and have fallen 47% since Feb 2021.

- Latin America is an area that could be a direct beneficiary of global energy issues.

- India, these equities are influenced by very different factors than global markets.

- Government bonds, following a significant fall in the face of rising inflation/interest rates, we have begun to introduce these as a specific allocation to reflect lower valuations.

- Commodities, there has been multi-decade underinvestment in many commodities, and an end to Russia’s invasion of Ukraine will not solve it any more than it caused it.

The Halloween effect

In years gone by, Halloween has often marked the beginning of a strong period for equity market returns. The phenomenon known as the ‘Halloween effect,’ can be described as a market timing strategy, proposing that stocks perform better between October 31st and May 1st than they do the months in-between. Without a logical explanation for its occurrence, it’s hard to comprehend the Halloween effect phenomenon, however, data suggest that it may not just be folklore.

We could all do with some more market positivity to end a challenging year, but only time will tell if the Halloween effect will come to the fore in 2022.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 288.10.22