The vaccine announcement appears to have been the catalyst for the value stocks to re-rate versus growth stocks on a global basis (fig.1). The UK, where the FTSE 100 is recognised as a proxy for value stocks, has performed poorly for many years and as result it looks particularly well placed to benefit from any sustained rotation from growth to value.

After the initial announcement, we have had other positive vaccine news and although there has been the occasional setback, the road through the pandemic is now more visible.

MSCI World Growth Vs. Value 5 Years Relative Performance (fig.1)

A change in the wind

There have been so many false dawns for a value recovery that many investors had reached the point of writing off the value style altogether. The global pandemic seemed to be another period which drove growth stocks higher and left value languishing in the weeds.

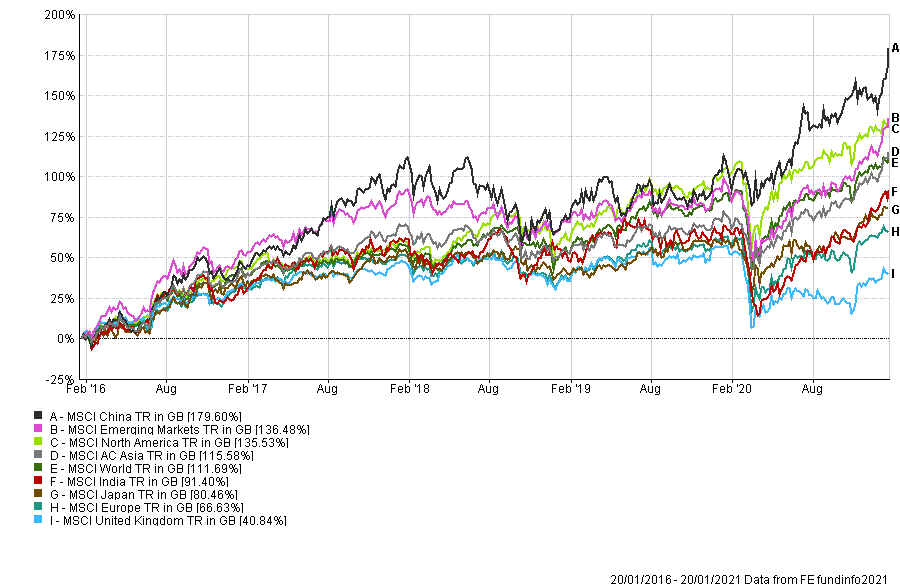

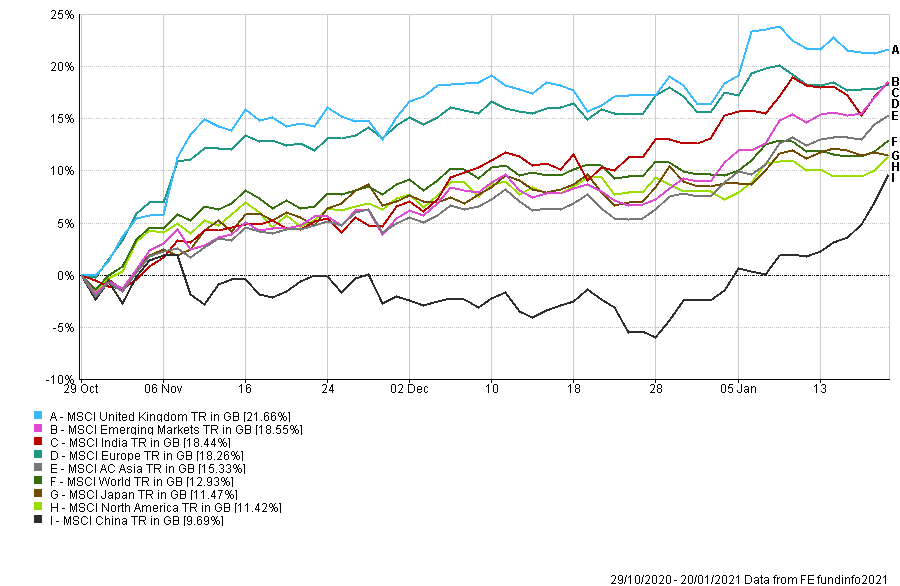

However, what we have witnessed since the end of October seems more than just a temporary mean reversion, the global economic backdrop has materially changed. It’s not just as simple as swapping out the label of value for growth, we have witnessed a change in the overall geographies in the ascendancy (fig.2).

MSCI World Indices 5 Years and 29/10/2020 to 20/01/2021 Performance (fig.2)

The vaccine news has allowed people to anticipate what a post lockdown world could begin to look like for companies and markets. While there have continued to be personal tragedies and we all endure continuing restrictions, most people can start to plan their post lockdown lives.

Whether the number of people vaccinated reaches critical mass in Q2, Q3 or Q4 is not really the issue, as the crucial point is that the end is in sight. Whatever your thoughts on how various governments have handled the situation, it doesn’t change the facts. No government, and this is especially true of democratic countries, wants economy destroying lockdowns to go on a day longer that they feel they need to.

Sterling surge

Returning to the UK, we see that the stellar relative underperformance in recent times has been owing to several idiosyncratic issues, not just the blanket Covid equity sell-off.

The FTSE 100 is home to many stocks which have traditionally paid attractive dividends including banks, but these dividends had been slashed or cut to zero. Although dividends may take time to reach their pre-pandemic figures, they will undoubtedly increase from their current depressed levels.

Outside of dividend cuts, Brexit uncertainty has made many investors shun the UK. This is especially so of overseas buyers who saw the UK as too risky, not least from a currency perspective. Paradoxically, one of our current concerns is the outcome of a rapidly strengthening Pound in a post-Brexit world and what effect this will have on our exporters.

In the first few weeks of 2021, the UK hit the ground running on the vaccine roll-out. The roll-out should help the economy recover quicker than some of our European neighbours. However, we ultimately need Europe to reach vaccination critical-mass if travel is to regain its pre-pandemic levels. If this occurs, we expect a degree of reflection on the ESG agenda.

Green versus sin

A further headwind, and one that is still very relevant, is the current emphasis on this ESG agenda. In the short-term this investing method is likely to receive a boost from the incoming Biden Administration, as it is hard to argue that Trump’s tenure was anything other than a headwind for ESG proponents.

However, many value stocks are ‘sin’ stocks, and 20% of the FTSE 100 consists of oil and basic material companies, whereas it only has just over 3% if the TMT sector. We now have (some) Brexit clarity and we expect a pick up in the commodities sector, banks, and travel and leisure. It is a pure coincidence that both a Brexit resolution and the vaccine occurred within the same few weeks, but these two pieces of news are likely to be positive for UK stocks.

Sin stocks could outperform in 2021, but in any event, the world needs basic commodities, many of which are listed here in the UK. Therefore, we expect commodities to perform well in the coming quarters, assuming the vaccines remain broadly effective against all the virus strains.

To take advantage of this, we hold a selection of UK funds that would be considered value plays and should benefit the most in a post lockdown world, alongside other funds of a similar nature in other sectors – such as the global equity sector.

As with UK dividend-paying stocks, global dividend payers were hit much harder than their growth peers during pandemic conditions. We expect funds such as Lazard Global Franchise, Guinness Global Income and Fidelity Global Dividend, to continue to benefit from a mostly normalising world. Some fund managers have re-positioned their funds throughout the pandemic period and continue to perform well. Margaret Lawson manager of the SVM UK Growth fund, and the highly successful team managing the Baillie Gifford International fund, are two such funds.

The Biden boom

With the Biden administration now in charge in the US, we can expect massive fiscal stimulus which we think will be inflationary but it will also be a positive in the short term for GDP. We expect many projects to be undertaken, mainly in the infrastructure space, and even if they turn out to be the ill-judged, there will be money to be made in the meantime.

The Biden team includes ex-Fed Chair Janet Yellen, and we see the combination of Yellen, Biden and Powell to be the debt dream team. Expect policies based on Modern Monetary Theory – in short; debt doesn’t matter, at least not now. This policy approach should be dollar negative, a situation that is likely to be positive for emerging markets and many Asian countries.

New challenges = more opportunities

To summarise, we need to invest based on how things are and not necessarily how we think they should be, given the many issues facing the world’s population. On this basis, we remain overweight to the emerging markets, Asia and the UK and retain our small underweight to the US. We continue to have significant exposure to the US growth stocks that performed well for many years, but we remain mindful that if new tax rules are introduced, this could hamstring some of the largest tech names. We have already seen examples of this in China, and we know the EU would like to do more to level the playing field if it could. Politicians want to be popular, and the new US government could gain some popularity by targeting companies that many voters feel game the system.

There is what appears to be a growing global central bank consensus to introduce some kind of cryptocurrency. In tandem with their respective governments, central banks will not want to give up their power over their citizens even as they debase their fiat currencies. This could mean new legislation that might negatively affect cryptocurrencies or, in the worst-case scenario, render them potentially valueless.

We wouldn’t rule anything out in this high stakes game, and it’s not just the authoritarian regimes working on digital currencies as Mme Lagarde has recently demonstrated. We are eagerly anticipating the post-Covid world, and whilst it brings new challenges, it also provides even more investment opportunities.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 40.1.21