Keep Calm but Maybe Don’t Carry On

Macro & Markets

Q1 was a bruising quarter for investors who maintained a relative overweight to the US assets which had previously performed so well. One new factor came into play on the 26th January and that was the arrival of DeepSeek which we believe heralds the beginning of the commoditisation of AI. The second new factor is the Trump tariffs.

In theory we knew that there would be technological advances in AI and we also knew that Trump would probably inflict tariffs on whoever he deemed stealing from the US. However, what we have so far in 2025 is the spectacular bursting of the AI valuation hype bubble and tariffs of unprecedented and unexpected magnitude which were launched with much with a display to inform the world but appeal to Trump’s voter base.

As we know the tariff announcements tanked global markets which prompted various spokespeople to give constant reassurance this was nothing to worry about however, on the 9th April Trump blinked. It was announced there would be a ninety day pause in the tariff implementation except for China whose tariff level was going to be 125%. In his own inimitable style, his team said that Trump had claimed maximum leverage, everything was going according to plan and promptly took a victory lap and markets rallied strongly.

Any extensions, delays, reversals or exceptions to tariffs are market positive, so from that perspective the overall situation is better than it was. The most commonly asked question we are getting right now is, is the end of the tariff induced volatility or a pause. We would say unequivocally it’s a pause and a short one at that. The collective tariff rate still in force remains far in excess of anything experienced in modern times. The trust in this US administration is likely lower than any other in history and trust doesn’t come back with a tariff climbdown or a Trump speech. The trade between the two largest economies on earth had been thrown into chaos and that is where it remains and will do so for the foreseeable future. Scott Bessent, Trump’s Treasury secretary said in the Q&A following yesterdays announcement that the administration had provided clarity and that should calm markets. This is disingenuous at best, as no clarity has been provided and all companies and counties are just in a slightly amended state of limbo.

From an investor perspective, we reiterate that there will be new winners and losers at a country and company level. We cannot say who they will necessarily be but to drive the point home, neither can the companies or countries themselves. W would also urge investors to not overlook the DeepSeek effect on valuations, especially of the Mag 7. A company like Apple, which is the largest company in the world has is now facing headwinds greater than at any time in its history.

Clients should be properly diversified and certainly not using the playbook pre DeepSeek and pre Trump 2.0. The financialisaton of the global economy means most governments including the US need strong asset markets and that should give people some comfort, but we will not return to the market dynamics of pre 2025. True geographical diversification and preferably across asset classes remains the best way to be invested in the markets as they are today and will likely remain.

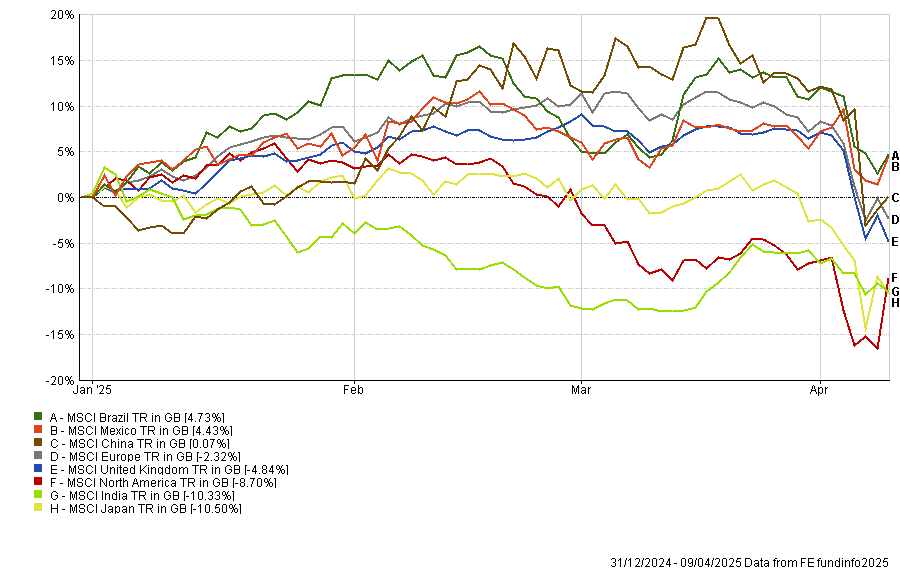

MSCI Selected Indices 01/01/2025 > 07/04/2025

Performance & Positioning

The following comments relate to performance data up to 1st April and, therefore, do not include the ongoing impact of Trump Tariffs on global markets. We will provide further updates in the coming weeks; however, if you have any specific queries, please contact your IBOSS contact, and we will be happy to assist.

The IBOSS portfolios have had a positive start to the year despite more challenging market conditions. We often talk about the benefits of holding diversified assets, and this year has acted as a stark reminder of why discipline is necessary for any investor.

Encouragingly, 39 of 42 IBOSS MPS portfolios have outperformed their respective benchmarks this year. Particularly noteworthy have been the Core and Decumulation ranges, both of which have delivered positive returns for clients, even as many benchmarks have fallen.

As discussed previously, much of the success can be attributed to the portfolio’s equity position. However, it’s also important to recognise the contribution from a broader mix of assets. Allocations to Fixed Income, Property, Commodities, and Cash have all helped to enhance the defensive qualities of the IBOSS portfolios in this more difficult environment.

Active management has also played a key role in driving performance — both through regional positioning at the portfolio level and the selection of underlying actively managed funds. To illustrate this, over 75% of the funds held within the Core MPS portfolios ranked in the top 50% of their respective sectors during Q1. This strong fund selection has benefited all portfolios but has been particularly impactful within lower-risk strategies, where active managers have capitalised on positive — albeit volatile — moves in bond markets.

Survival Guide: Helping Clients Stay Focused Through Geopolitical Uncertainty

Periods of heightened geopolitical tension and market volatility can understandably lead to investor concern. However, it’s worth remembering that markets have faced, and recovered from, a long history of geopolitical events and uncertainty.

Looking back over the last 50 years, markets have navigated wars, recessions, oil crises, political shocks, global pandemics and even Tariffs. Importantly, history shows that while these events can drive short-term volatility, their long-term impact on well-diversified portfolios is often limited.

We have put together a few soundbites below, which are hopefully interesting, if not useful, for end-client conversations.

Geopolitical Events and Their Impact on Markets

Research from Fidelity and JP Morgan shows that, following major geopolitical events, such as the Gulf War, 9/11, or the Ukraine conflict, markets typically experienced an initial short-term sell-off, but often recovered quickly. In fact, on average, the S&P 500 was higher 12 months after such events in over 80% of historical cases.

Trade Wars – A Recent Example

Take the US-China trade war in 2018-2019. During this period:

- Headlines were dominated by tariffs, retaliations, and slowing global growth fears.

- Global equity markets experienced sharp sell-offs and the MSCI World Index fell nearly 14% between September and December 2018.

- by April 2019, approximately four months later, it had recovered to its previous high.

The Cost of Missing the Best Days

Periods of heightened volatility are often when markets experience both their worst and best days. Attempting to time markets (by exiting during uncertainty and re-entering later) can be extremely costly.

The information below is based on a study by AXA and looks at the MSCI world index from 1980- 2021. The graphic highlights the importance of remaining invested and how impactful missing the best days of a market can be for even longer-term investors.

Source: AXA Investment Managers, MSCI World Index (1980-2021)

In summary, missing just a handful of the best days can significantly reduce long-term returns. However, staying invested, staying diversified and avoiding emotional decision-making in times of stress can be a more reliable way to build wealth over time.

The Price of Admission

Geopolitical risks are an unavoidable part of investing, but history shows that staying invested, staying diversified, and maintaining a long-term perspective have consistently rewarded patient investors.

Unfortunately, volatility and uncertainty are the price of admission, and without some uncertainty, one cannot expect to achieve returns over and above cash over the long term. It is worth considering that more difficult markets can present opportunities for patient and long-term investors.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.