Call My Bluff

This update covers from 15th January to 14th February, but we have used year to date charts to give a slightly broader perspective.

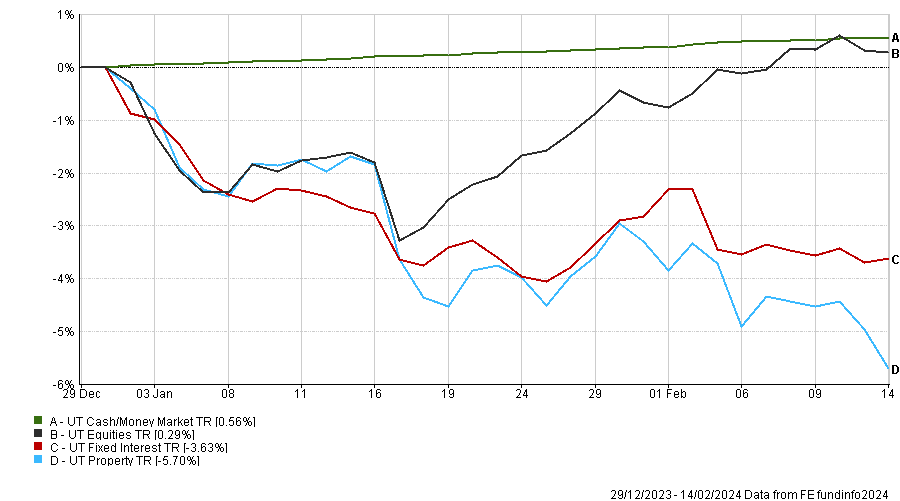

Since our last update, equities have been the clear winner, with a 1.9% gain driven by developed markets, especially US tech stocks. This has meant equities in total are now back in positive territory for the calendar year. The three clear winners in the equity space were the US, Japan, and India, three countries that makeup 36.4% of our current equity exposure. Cash was also positive at 0.4% for the period.

This is in contrast to fixed income and property which lost 1.05% and 4.13%, respectively during the past month, and are still coming to terms with yet another about-face by the Federal Reserve and their current spiel that rates won’t necessarily fall as quickly as the market had priced in.

The market had anticipated numerous cuts in response to signals from the Fed, leading some to speculate that Powell’s actions were primarily aimed at meeting Wall Street’s year-end targets and facilitating bonuses for market participants. Regardless of the motive, fixed income assets, in particular, have retraced approximately 50% of their gains since late October last year.

Asset Class Performance 2024*

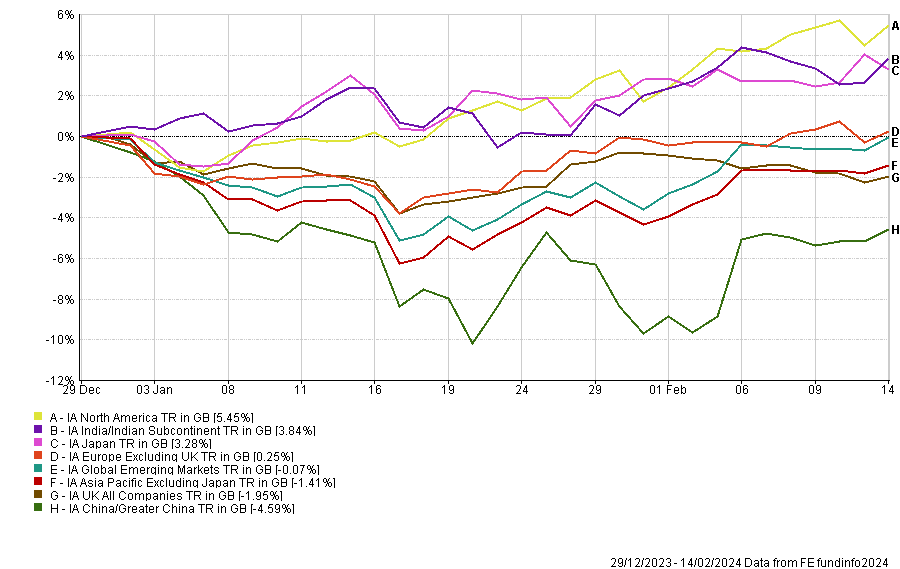

Geographical Performance 2024*

Macro

Central Banks

There were meetings for the Fed and Bank of England during the past month, but neither produced any significant surprises. Both banks kept interest rates on hold as expected and removed any reference to the potential need for further tightening from their forward guidance. It would be interesting to know whether the Fed would have adopted new wording had they known they would get the much stronger CPI numbers released on 13th February. For sure, the proverbial cat is genuinely in and amongst the pigeons. This means we will all be subject to endless finessing of the Fed narrative around future rate cuts, which won’t tell us anything. Right now, the Fed has to be essentially data dependent. The notion that it should be anything other than data-dependent never ceases to amaze us.

Market wise, stocks particular tend to react badly to certain inflation data and then slowly shrug it off as the equity melt-up continues.

The European Central Bank also took a similar line, and all three central banks are again singing from the same hymn sheet – interest rates look set to be cut significantly over the coming year, but not before April or May.

Elections

We discussed politics and elections at length in last month’s investment update, where, in our opinion, the actions of the Fed and other central banks are much more important for markets than those of the presidents or ministers, suggesting the November elections stateside are not as critical as generally thought. A noteworthy announcement from Trump in recent weeks is one to keep an eye on though, as he said he would sack Fed Chair Powell if he won, upping his relevance to investors.

In what will probably be seen as a positive outcome for Asian markets, former Defense Minister Prabowo Subianto, appears to have won the battle to succeed Joko Widodo as President of Indonisia. His promises to continue the polices of the incumbent and very successful campaign to woo the younger people vote. At 72 he can be added to the list of rather senior males either retaining or gaining power.

Diversity in political power looks like it still has a ways to go.

Earnings Season

This earnings season was dominated by the Magnificent 7. The results are available everywhere, but it is worth highlighting the positive results from Meta (Facebook), which saw Wall Street’s largest-ever daily gain in market capitalisation with a rise of $196bn. On the flipside, Tesla’s numbers and the company call were disappointing. The shares have now fallen circa 35% since the highs of summer 2023, so maybe we will need a new catchy title for the remaining six stocks. Overall, this earnings season has been reassuring for the equity outlook, though it might not be as well received by the Fed, at least in private.

Overall, US tech continues to be the main driver of the gains in the US market; however, the elevated valuations of these companies and the narrowness of the recent market increases mean we retain our cautious view on US equities at an index level. We have noticed in recent weeks more investor concern about the US performance, especially for obvious reasons those who were involved in the markets between 1997-2001. Yes, this time is different, and no two periods are the same, but ultimately, unless you are a trader rather than an investor, the price you pay for an asset is of the utmost importance.

The Broader Tech Market

Our explicit Japanese holdings stood us in good stead throughout January and very much continued into February. It is often overlooked that countries other than the US have tech and tech-enabling companies. M&G are invested in some of the current stars in Japan and has produced some stellar returns.

Another fund proving to be best of breed is the Comgest European Growth fund. This fund has circa 8% in ASML Holdings and again highlights that the tech sector, particularly the Chip and AI-related stocks, has a broader reach than simply the US. This fund is number one in the IA Europe sector over the last year.

China

The general malaise surrounding Chinese investments continued until a few days before the week-long Lunar holidays. The liquidation of Evergrande, the property developer, has been a long time coming and was no real surprise. However, it still refocused attention on the problems facing the property sector. Sentiment was also not helped by the authorities’ failure, as yet, to follow through with concrete measures following their recent acknowledgement of the need for further policy support.

The big new news out of China was the cabinet replacing Yi Huiman as chairman of the China Securities Regulatory Commission (CSRC), replacing him with Wu Qing, a veteran securities regulator and a former deputy in Shanghai’s municipal government. Historically, changes to this post have led to strong equity markets, but it’s a small data set, and we wouldn’t want to extrapolate too much from the move. That said, it would indicate that Xi Jinping realises that something of significance needs to be done if confidence in the Chinese markets is to be restored to any significant degree.

As with some managers and investors citing words of caution around some US assets, in the last few weeks, there have been some Asian and emerging market managers allocating more towards China. Interestingly, Michael Burry, who came to prominence in the film The Big Short ( a must see if somehow you haven’t already) has doubled down on his bullish China bets, especially in the tech space.

Portfolio Performance & Positioning

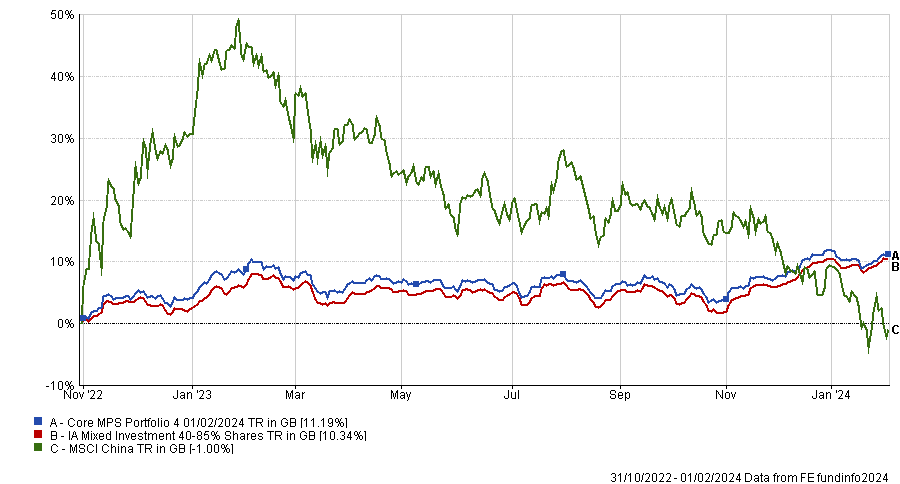

Debunking the Myth of IBOSS underperformance in a rising market

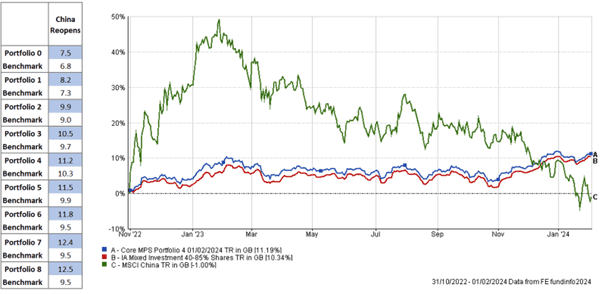

Whilst the positive returns of last 4 months are understandably the focus for many investors, markets began rallying in earnest on 31st October 2022 – when China’s market reopened following the nationwide COVID lockdowns.

It is worth noting that whilst the catalyst to more favourable market conditions was the reopening of China, Chinese equities were down 1% over the same period and the China reopening was counterintuitively not all about the outcome for Chinese markets.

Since the market has turned around, all IBOSS portfolios in the Core and Passive MPS ranges have outperformed significantly into a rising market – beating all IA benchmarks by a considerable margin

This should go some way to demonstrating that the portfolios are positioned to take advantage of a broad market rally.

IBOSS Performance in a rising market – 31/10/2022 – 01/02/2024*

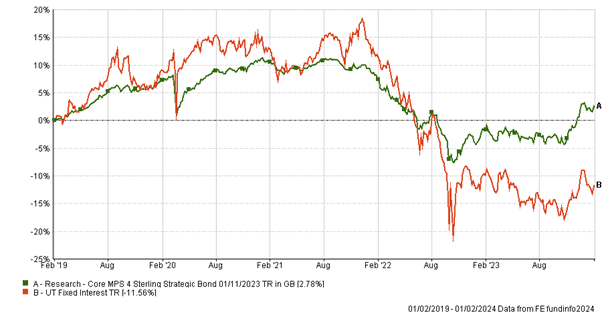

A Short Note on Fixed Income

We have highlighted before that 2022 was one of the worst years for bonds on record, however these periods of weakness present opportunities for investors. Those portfolios which had positioned more defensively in the bond space are best placed to take advantage of higher yields and the potential for capital growth.

The chart below demonstrates the performance of our fixed income position over 5 years versus the average bond fund. It is worth noting that since 12/10/22, our bond position has risen by over 11% and is, once again, a positive contributor to returns over 5 years.

5 Year Performance – IBOSS Fixed Income against UT Fixed Interest*

Investor Outlook

Chinese equities look very cheap, but just as many investors are ignoring the expensiveness of the US market, so too is the cheapness of the Chinese market dismissed by increasingly large numbers of market participants.

Valuations have proven to be a good indicator of long-term return potential, even while providing little guide to short-term market direction. Japan is close to hitting all time highs, several decades after they last reached these dizzy heights. To almost everybody’s surprise they have just slipped into recession, but once again the markets prove they are not the economy. We remain bullish and overweight Japan despite its run up in values and, as well as a host of positive factors around improving corporate governance, their markets are often driven by country specific idiosyncrasies, often exhibiting lower correlations to most developed markets.

After a positive earnings season, the US looks like it can continue its strong run. At the same time, the UK once again looks relatively attractive at these levels.

Overall, there are more grounds for optimism than pessimism for the coming months.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 45.2.24