Beware of the Pivots

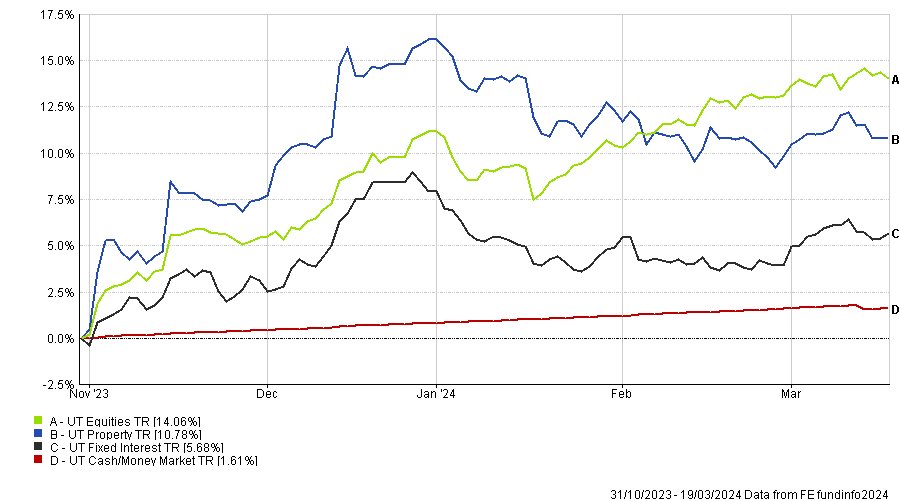

This update covers the period from 14th February to 19th March, but we have taken the basic asset class chart back to the end of October last year. That was about when interest in cash peaked, and it turned out to be right before one of Fed Chair Powell’s infamous pivots.

On the back of one hot CPI print and a Powell speech, risk assets took off in a rally that lasted until the end of January 2024. Since then, we have lived in a more nuanced world with much debate about whether inflation has peaked and, more importantly, its trajectory from here.

Asset Class Performance Since The Last Powell Pivot*

Macro

The Magnificent 7… 6… 5… 4… 3…

The performance of the largest technology companies almost entirely dominated the relative performance of portfolios in January. Since then, understandably, investors began to extrapolate this extraordinary performance into the rest of the year. However, only NVIDIA, Meta, and Amazon have outperformed global equities since February, and companies like TESLA and Amazon have posted markedly negative performance figures for the same period. It is worth remembering that though the Magnificent 7 is admittedly a catchy moniker, these companies have very little in common and, in many cases, compete directly with each other.

Ultimately, whilst the Mag 7 may well present value from here, taking concentrated positions in the most popular areas at the point of peak hype is rarely the most sensible approach. History is strewn with relevant examples, and whether we’re talking about the “nifty fifty”, the “BRICS”, or “internet stocks”, the lessons learnt are usually the same – avoid herd mentality, be cautious of the hype, maintain diversification, and most importantly – don’t ignore the risks.

Portfolio Performance & Positioning

We’re all multi-asset investors

After all, there are two very important reasons we, collectively, look to invest in multi-asset portfolios, and they are directly related to client outcomes.

The first is to smooth out the client’s investment journey, i.e., reduce volatility or risk. Reducing an investment’s volatility to suit a client’s attitude to risk and capacity for loss makes investments accessible to a broader audience. As we are all aware following recent market movements, investing can be incredibly stressful, and reducing some of the more significant market swings through diversification can help keep clients on a journey that ultimately rewards patience and long-term time horizons.

The second, and equally important point of multi-asset investing, is to expose a client’s portfolio to a broader selection of global investment opportunities. We talk about diversification in portfolios a lot, but there is sometimes the misconception that diversification equates to lower returns.

However, it is worth remembering that the areas with the most significant opportunities often have the highest potential risk. This point was articulated in our webinar this month by Hermes Asia-ex Japan manager, Jonathan Pines. He highlighted the potentially once-in-a-lifetime opportunity in his asset class and focused on areas like China and South Korea. (Watch the webinar on demand here)

These regions are up circa 11% since February and would be unsuitable as a stand-alone investment for all but the most risk-hungry clients. However, in a multi-asset portfolio, these assets can contribute significantly to total returns and even help offset the risk of other assets.

Outperformance in rising markets

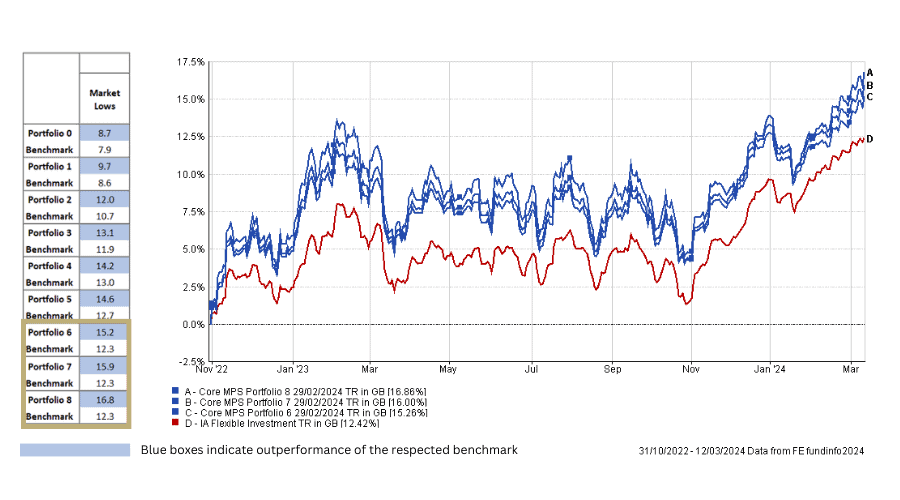

It has now been almost 18 months since the market lows of October 2022. Since then, markets have rewarded investors for a more diversified equity allocation – something which may come as a surprise considering the financial press’ focus on the Magnificent 7.

To highlight this point, we have included a chart below showing the performance of the IBOSS Core MPS range since this market low. As you can see, whilst all core portfolios have done well over the period, the higher-risk portfolios have seen the largest relative outperformance.

It is also worth noting the total returns – which range from 8.7% to 16.8% over the period.

Strong returns since the market lows – 31/10/2022 – 12/03/2024*

Investor Outlook

We maintain a favourable outlook on markets and sectors that offer attractive valuations on a relative basis and contain companies that haven’t excessively capitalised on the AI hype, or the retail investment frenzy. While acknowledging the potential for further growth in certain AI-related stocks beyond the US, we have exposure via Europe, Asia, and Japan.

Our allocation strategy tilts underweight towards the US compared to our peers. However, within our US holdings, approximately 50% is invested in value-oriented companies, a position we’ve upheld for the past two years.

Our overweight position is in the Asia Pacific and emerging markets, with a specific focus on Latin America and India, as we anticipate these regions benefiting from deglobalisation and friendshoring. While we hold a slight overweight position in China, we believe that if China continues to falter then other Asian and emerging markets will be the primary beneficiaries.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 74.3.24