Since the global financial crisis (GFC), there has been no other event more significant to markets than the creation of effective vaccines against COVID-19. It doesn’t actually matter what an individual’s view or opinion may be on vaccinations; the markets repositioned themselves across all the asset classes post the first vaccine announcement in November 2020.

Although this update covers 2021, markets don’t change based on calendar years but on events.

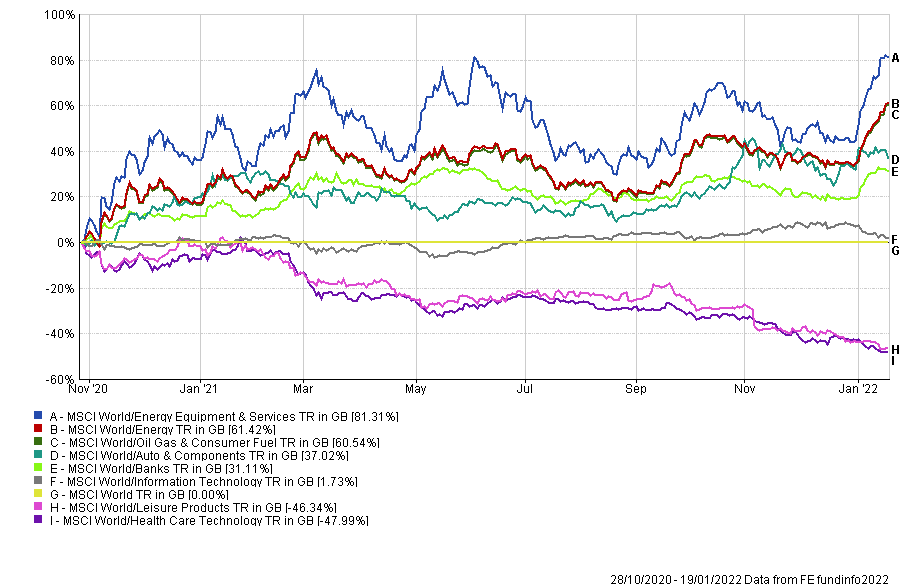

Global Sectors Versus Vaccines

The period since the first vaccines were approved has been marked by unprecedented sector divergence across the globe.

Intuitively one might expect healthcare to be a dominant sector as the world grappled with its first pandemic in many years, however, it continues to lag behind all other sectors. While there have been individual winners within the sector, buying the index has produced inferior relative results to the broader market.

Global Sector Performance Since The First Vaccines | 28th October 2020 – 19th January 2022

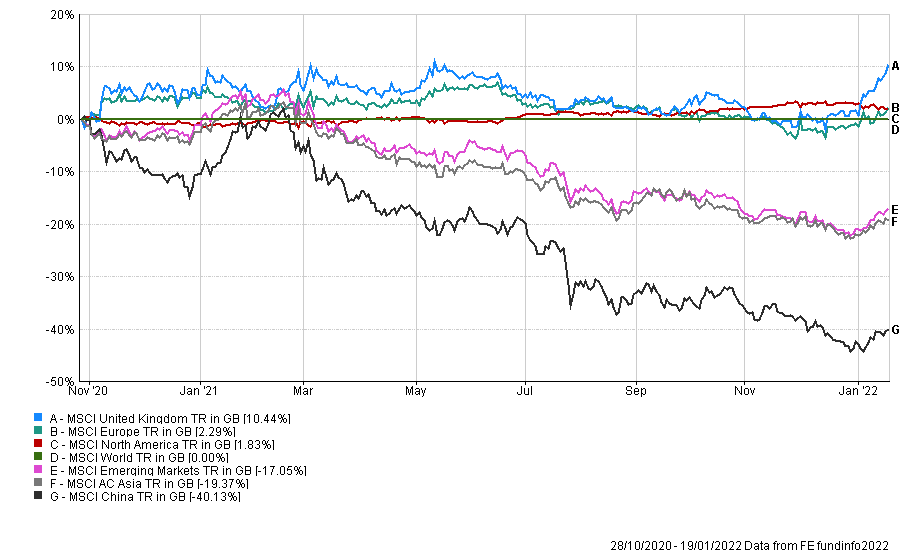

Geographical Location Versus Vaccines

If we look at the pandemic’s effects on countries alone, then China should have considerably outperformed most of its peers. Its zero-tolerance policy has led to an infinitesimally small number of cases, hospitalisations and deaths compared to countries such as the US.

The reality, however, has been very different. The Chinese government’s clampdown on its tech and property companies, in particular, has meant the Chinese equity market has significantly underperformed almost all others. At the same time, whilst much of the developed world was literally throwing money at the economic problems caused by Covid, the Chinese government showed considerable restraint. Risk markets, especially post the GFC, like liquidity and easy money, not fiscal and monetary discipline, and the results are evident for all to see.

Selected Geographical Performance Since The First Vaccines | 28th October 2020 – 19th January 2022

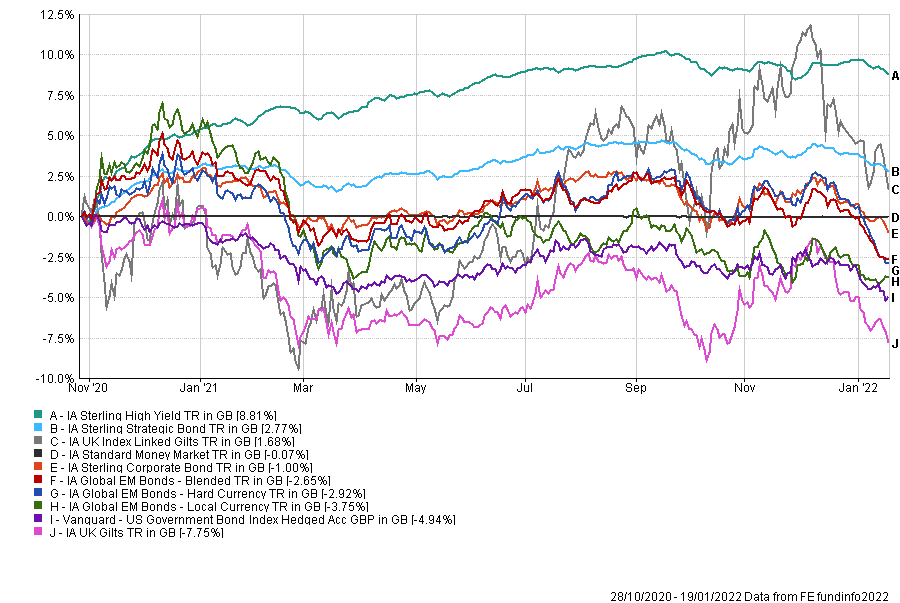

Fixed Income Versus Vaccines

We suggested at the end of 2020 that barring a new variant that was worse than its predecessors, most, if not all, fixed income sectors could produce negative returns in 2021. Except for high yield and a minimal gain for the strategic bond sector, fixed income did indeed lose money, particularly sovereign bonds.

Fixed Income Sector Performance Since the First Vaccines | 28th October 2020 – 19th January 2022

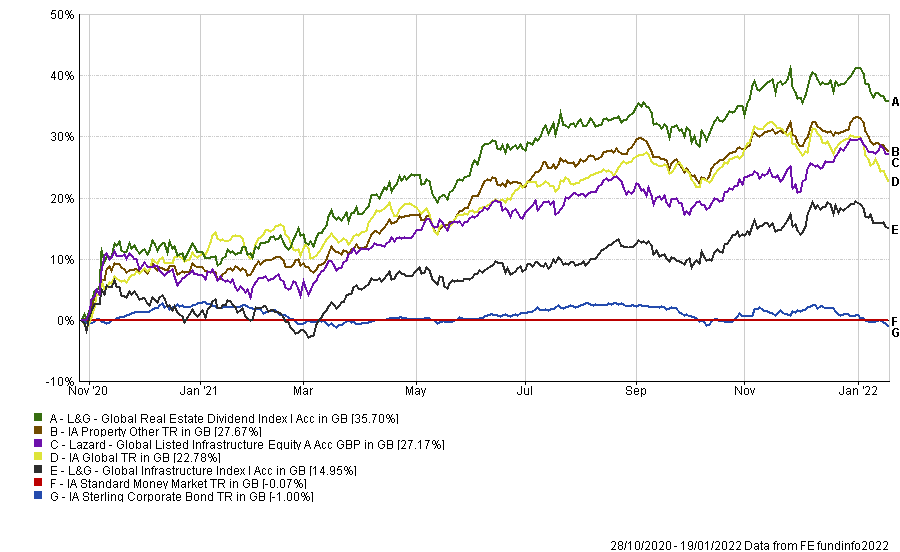

Property Versus Vaccines

Global property was probably the biggest surprise for many investors since the news of the vaccines first broke. It isn’t that a return to some kind of normalcy would be harmful to property, but the headwinds seemed not inconsiderable.

There was already pressure on retail across the globe as more shopping continued to move online. Much commercial office space also suffered from a shortage of people to buy or rent at the same pre-pandemic levels. However, the factor which has been the dominant one, is the inflationary environment and need for real assets. A combination of global property securities and infrastructure worked well in 2021 but has run out of steam in early 2022. Fed policy and bond yields will be critical to returns as life goes back to some kind of pre-pandemic iteration of normal.

Property/Infrastructure Performance Since The First Vaccines | 28th October 2020 – 19th January 2022

Where Are We Now?

Many assets, including certain equities and bonds, benefitted from the governments and central banks actions to counter the negative impact of the pandemic. In reality, this meant even more money printing and easy monetary policies than was already the case. An outcome has been that some of the behemoth growth stocks such as Amazon and Facebook, and stocks like Netflix have valuations that pre-pandemic would have seemed almost unthinkable.

It is said that in investing, the most dangerous phrase is “this time is different.” That might well be true most of the time, but we would contend that the factors driving asset prices don’t stay precisely the same either, and neither will the best-performing countries or sectors in the coming months and years ahead.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 7.1.22