April was another difficult month for investors as equities and fixed income assets fell simultaneously. We have seen this dynamic each month throughout 2022 – excluding March, where equities gained 3.3%.

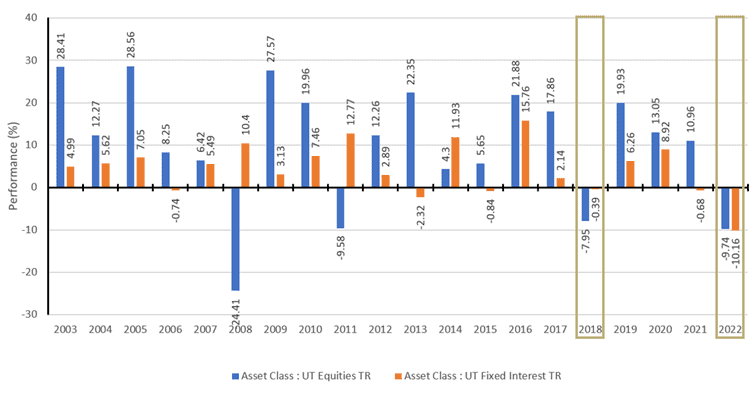

Although we are only partway through the year, the chart below (fig 1) demonstrates how rare this set of circumstances has been throughout the last two decades, as bonds and equities have both fallen circa 10% in 2022. The last time the two most significant asset classes fell together was in 2018. This was a direct response to the Fed’s announcement that they would systematically tighten monetary conditions via interest rate rises and running down the balance sheet.

There are clear parallels with the current situation, but the critical difference this time around is the backdrop of global inflation. The necessary response by central banks and, most notably, the Fed could mean that the next several years may continue to look very different to the last.

For those who want a rundown of our recent positioning, please refer to our latest client-friendly market update (02/05/2022).

Calendar Equity and Fixed Income Performance – 20 Years (fig 1)

Inflation is Not Transitory

Our view is that the world changed at the end of November 2021. The event was a speech given by Jerome Powell, the US Federal Reserve Chair. He admitted what almost everybody else already knew: inflation was not transitory and would become a very big deal. This acknowledgement of inflation is important for markets.

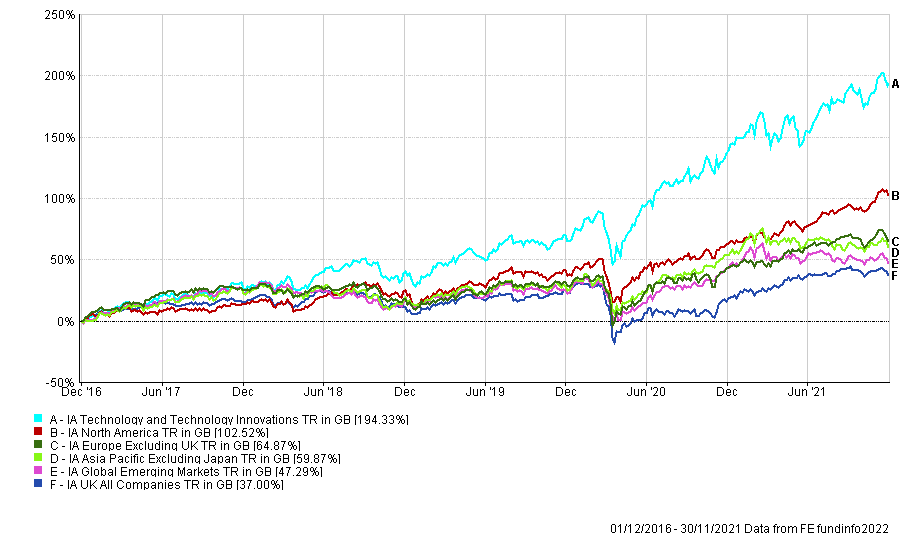

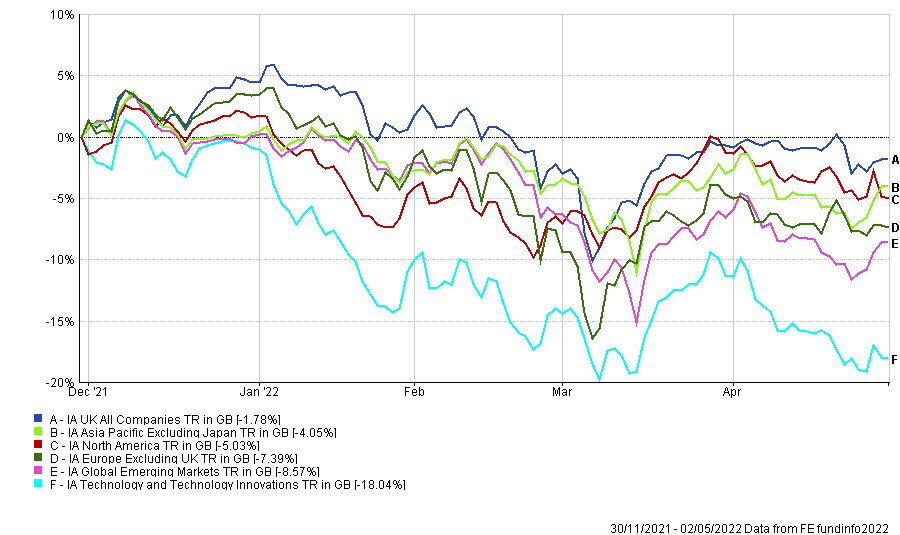

For most of the period since the Global Financial Crisis (in 2008), central banks have been able to keep interest rates at historically low levels, principally due to minimal inflationary pressures. This, in turn, has been an excellent backdrop for companies classed as growth stocks. The technology sector, in particular, has produced stellar returns, as can be seen in the chart below (fig 2). However, what is equally clear is that growth tech stocks have been struggling ever since that speech (fig 3). This includes April, when US equities fell harder than other developed markets (-4.57%), led by Technology (-7.56%).

Global Equities 5 Years Performance to 30/11/2021 (fig 2)

Global Equities 5 Month Performance 01/12/2021 to 02/05/2022 (fig 3)

So far, we have seen the most significant falls in the stocks that were once the most expensive. Retail investors had flooded into so-called “meme-stocks” following the pandemic. They experienced super-normal returns in stocks such as Tesla, Roku, DocuSign and Peloton and adopted a technology first approach to investing.

However, today the investment case looks less compelling, with strategies like ARK Innovation down 70% from peak to trough and the Roundhill Meme Stock ETF down 30% since launch (12/08/2021). In addition, we have started to see larger index constituents struggle and companies like Microsoft, Alphabet, and Apple have had a torrid April.

We would expect volatility to remain high whilst markets and commentators spend considerable time assessing the impact of a rate hike of 0.5 vs 0.75. What is of much greater significance to us, is that the direction of travel for developed country interest rates is clear; it is up!

Chinese Equities

Another area that has seen something of a capitulation has been Chinese equities. In the first quarter of last year, the Chinese government aggressively added regulations for its largest technology firms, imposing restrictions on gaming to tackle addiction and destroying for-profit education services almost overnight. These self-imposed regulations, combined with the situation facing many of their property companies, such as Evergrande, and continuing COVID-19 lockdowns have led to significant investor uncertainty. As a result, Chinese equities have lost over half of their value from February 2021 to mid-March 2022.

However, the medium-term outlook has somewhat improved. On the 15th of March, the Chinese government expressed the desire to be more supportive of its markets – a situation entirely different from that of the developed world. Since then, Chinese equities have been up 15% from their lows. April saw Chinese equities outperform most developed Markets (ex UK) by posting a marginally positive return for the month, albeit with significant volatility.

Of course, investing in Chinese equities in isolation does come with a considerable degree of risk. Still, the combination of lower valuations and more supportive government policy could be a potent combination for investment managers with the ability and expertise to invest in the area.

The considerable headwind of their zero COVID policy is having a dramatic effect on parts of their economy, but as medium, to longer-term investors, we need to look past this. The Chinese government have an array of weapons they can use to maintain economic growth, and history tells us they will not be afraid to use all means necessary to support their economy.

Fixed Income, Growth Stocks and Interest Rates

We have been asked recently why growth stocks have performed poorly in an environment with rising interest rates. The simple answer is – that growth companies may have a more difficult time financing the growth of their companies as the cost of borrowing increases. Not only that, but higher rates make bonds look more attractive as the yield on these instruments rises by necessity.

Investors, ourselves included, now have to address the current situation and the changing risk/return profile between bonds and equities. Our fixed income position has successfully protected capital through April, and 2022, due to our cash position and focus on short-dated bonds, which has contributed significantly to relative performance. However, as with equities, we need to assess future investment opportunities rather than invest using the rear-view mirror. With 10 year treasuries currently yielding above 3%, we are now looking to potentially increase our sovereign bond holdings for the first time in over three years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 130.5.22