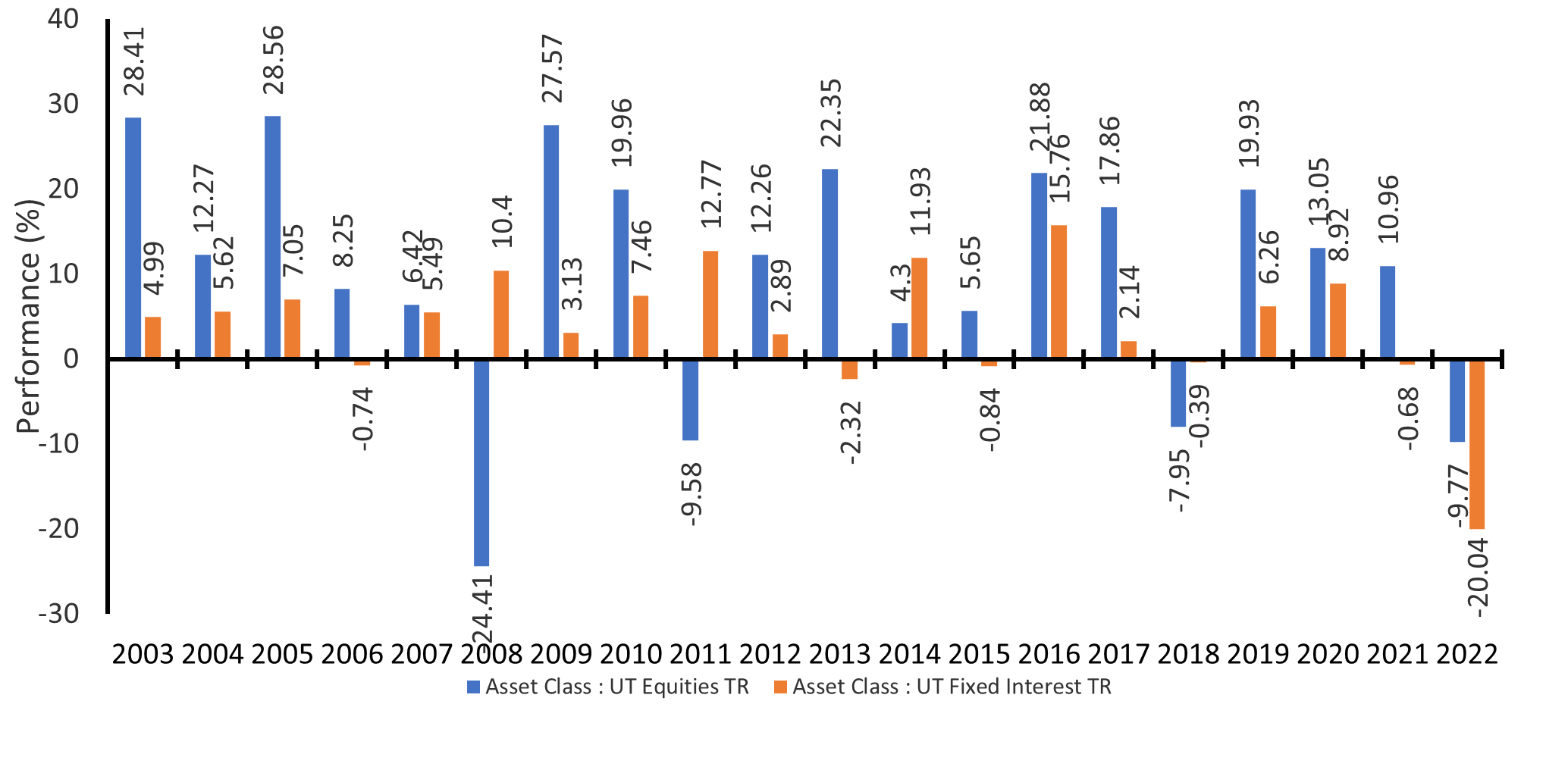

As we approach the end of 2022, it seems inevitable that whatever December has in store for investors, the year will likely go down in infamy, gracing students’ textbooks and exam questions for years to come. Though assets have seen a significant bounce from October to November, the chart below demonstrates (fig 1) the uniqueness of asset movements this year as bonds and equities have fallen parallel to each other. As we sit here at the start of December, your average equity fund is down close to 10%, whilst your average bond fund has seen twice the falls of that, at nearer 20%.

Discrete Calendar Year performance- bonds and equities (fig 1)

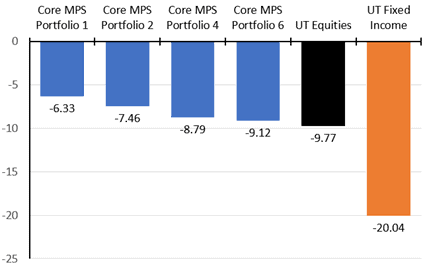

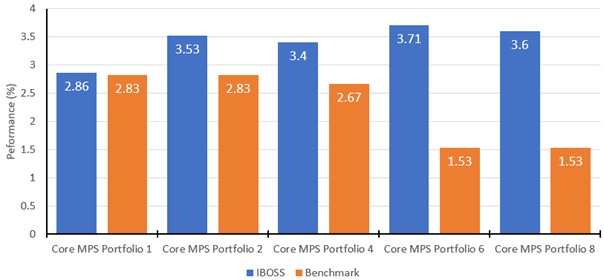

In the main, these movements have meant that lower-risk portfolios, which tend to have a higher weighting in bonds, have struggled relative to higher-risk, equity-heavy portfolios. However, it is worth noting that the IBOSS portfolios have not exhibited these characteristics (fig 2).

IBOSS Core MPS Performance Year to Date (30/11/2022) (fig 2)*

Currency

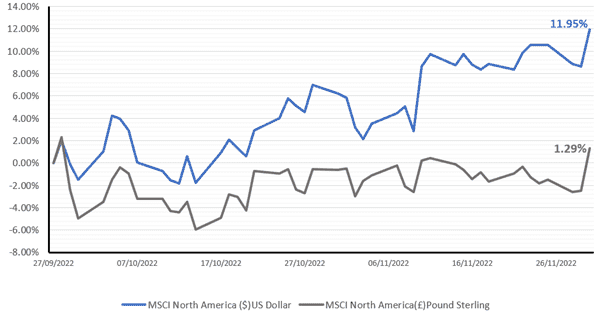

In the October market update, we spoke at some length regarding the impact of currency on portfolio returns. More specifically, we talked about how October was the first month where the dollar had weakened significantly relative to the sterling. November saw a continuation of this trend, with the dollar falling circa 4% against the pound.

This is already a significant movement, and (fig 3) demonstrates the huge effect currency can have on returns; when US stocks were up close to 12%, UK investors saw a gain of only 1%. In short, the bounce in US equities over the past two months was almost entirely wiped out by a weakening dollar.

US Equity Performance in Dollar and Sterling (27/09/2022 – 30/11/2022) (fig 3)*

Our Core portfolios have performed well in this environment, as a more diverse range of equities contributed to outperformance (fig 4).

Core MPS Performance (27/09/2022 – 30/11/2022) (fig 4)

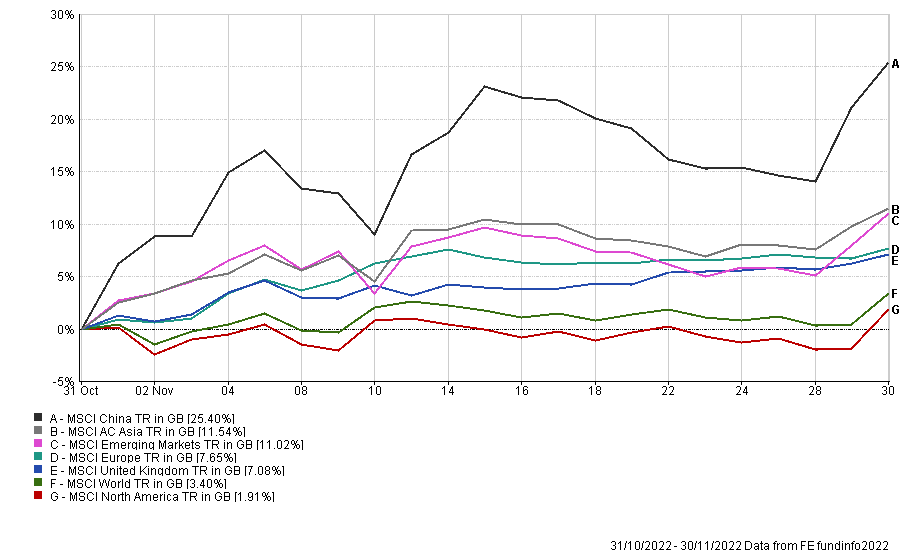

Equities, China, the UK and the US

As alluded to previously, the dollar’s weakness has suppressed the returns of North American equities, which have lagged other developed markets over the month. However, the most significant contributor to total returns in November was an allocation to emerging markets and Asia. This Asian and emerging market outperformance has been led by a rebound in Chinese equities to the tune of 25%.

Much of the turnaround in the fortunes of Chinese equities relates to its zero covid policy, a stance that has kept uncertainty elevated throughout 2022. The spate of protests against the zero covid policy in November has led to the scaling back of some restrictions, including easing covid testing requirements. As discussed previously, further relaxation is likely in the coming months; however, the table below (fig 5) demonstrates how violent the moves in Chinese equities can be over the short term.

The prospect of a rebound in the Chinese economy next year contrasts markedly with the outlook for the western economies. It is a key reason why we remain broadly positive on Chinese equities. Still, we know from recent experience that the Chinese authorities are apt to throw in the occasional negative and positive curveballs. We are also relatively optimistic about UK equities which are currently the only major market to deliver a positive return this year, albeit only of 1.8%. But our bullishness here is based on super-cheap relative valuations rather than an improving economic outlook.

Global Equity Performance – November 2022 (fig 5)*

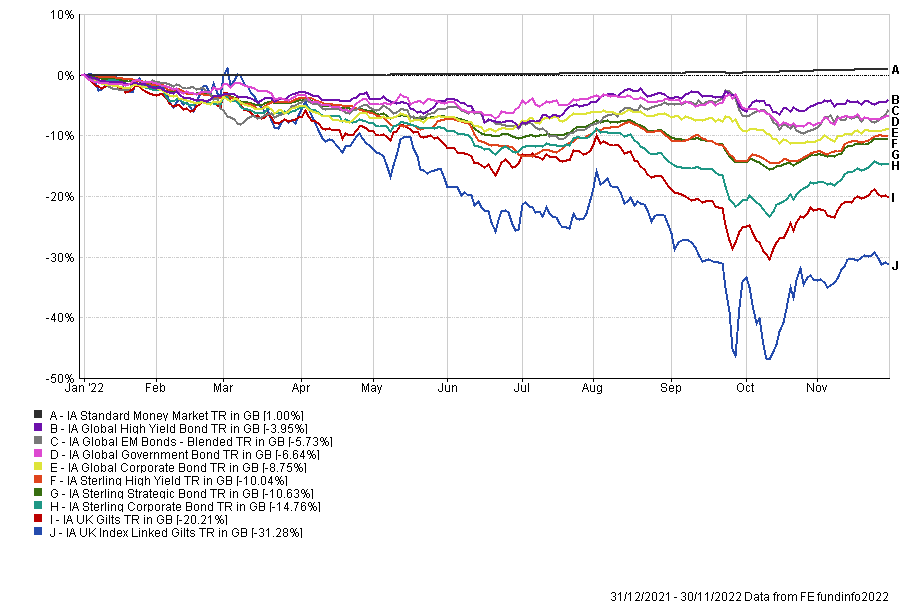

Interest Rates, Fixed Income and Central banks

The November rally was not confined purely to equities, as all fixed income IA sectors rallied between 1% and 4%. Much of these movements can be attributed to comments from the central banks, and as ever, we have had plenty of those throughout recent weeks.

Last week, for example, Powell hinted strongly that the Fed would, at its next meeting on the 14th of December, raise rates by 0.5% rather than by 0.75% as in the last three moves. He also said the Fed did not wish to overtighten. Markets seized on these comments, but in our opinion, they merely confirmed what the Fed had already been pointing toward.

Moreover, Powell’s remaining comments were distinctly less dovish. He continued to downplay the significance of the pace of tightening and emphasise the importance of where rates end up and how long they remain there. He also reiterated that the Fed will stay the course until the job is done and that history argues strongly against prematurely loosening policy.

Even so, the markets, in their wisdom, have scaled back their expectations for Fed tightening and are now pricing in rates peaking at slightly below 5% in the spring. Most importantly, they assume the Fed will cut rates by 0.5% in the second half of next year. This optimism has led to 10-year Treasury yields falling back to 3.5%, a full 0.75% down from their October high of 4.25%.

Whilst constant Fed jawboning impacts sentiment over the shorter term, our longer-term view remains largely unchanged. Following a historic collapse in bond prices this year, there are now undoubtedly opportunities for fixed-income investors that simply didn’t exist at the start of the year. We have been successful in our lower-risk portfolios by maintaining a low-duration position; however, it may be time to expand that position to capitalise on these new opportunities. A direction we began to move toward within the November changes.

Year to date Fixed income Sectors (31/12/2021 – 30/11/2022) (fig 6)*

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 344.12.22