“We are stranded here in the city in the snow, and everybody’s talkin’ but nobody really knows, nobody really know”

lyrics by Van Morrison

Investor Euphoria

We have recently written an update outlining some of the more concerning behaviour prevalent in global markets. FOMO (fear of missing out), TINA (there is no alternative), and BTD (buy the dip) are acronyms that have become part of many investor’s vocabulary and indicate a generally risk-on approach to investing, even if it is somewhat reluctantly. Investing in risk assets based on any or all of these acronyms has worked undeniably well over recent years. The combination of loose monetary policy, low-interest rates, and highly accommodative and market-sensitive central banks has benefited most global equities.

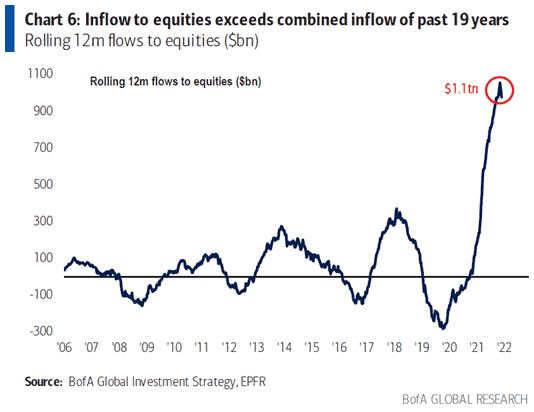

The chart below (fig 1) indicates the current level of investor euphoria. The recent boom in investor inflows into equities equates to a total of approximately $1.1 trillion – more than the previous 19 years combined. While less experienced market participants could see this as a positive, we note that massive inflows (particularly retail flows) rarely, if ever, coincide with stronger future returns.

For more thoughts on the euphoria present within markets, please read other market update in December: Maximum Greed?

(Fig 1)

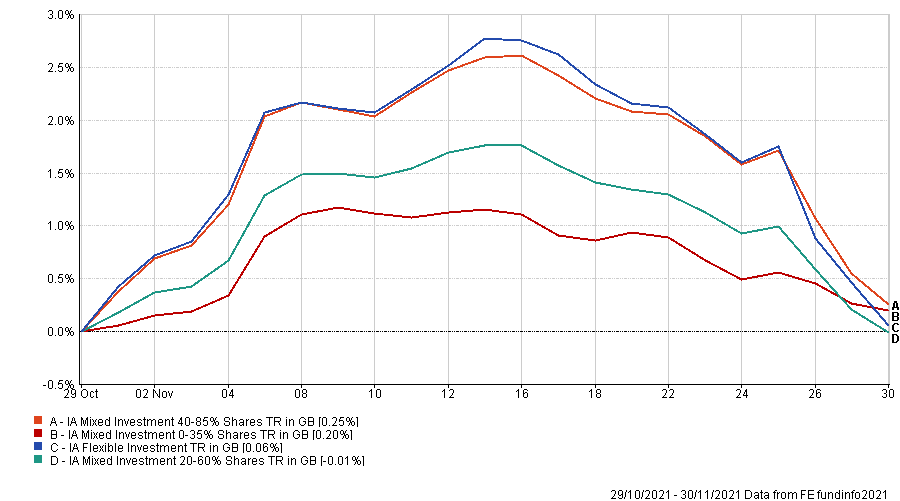

November’s performance was very much a game of two halves. The exuberance felt throughout October continued during the first half of November but faltered into the latter half, leading to essentially flat returns (fig 2).

Mixed Asset performance through November (Fig 2)

There were multiple factors influencing price through the end of the month.

The Fed

Firstly, markets were shaken after the reappointment of Jerome Powell as Fed chair as he “retired” the word transitory and commenced with more hawkish rhetoric. He has now repeatedly indicated that inflation could indeed be a longer-term risk factor. The increasing job openings, wage pressures, and ongoing monetary and fiscal stimulus had already persuaded many market participants that inflation was neither transitory nor under control. Our concern for much of the latecomer retail money still piling into US equities is that the Fed may not be able to have the investors back for the first time in many years. Potential air pockets in both equity and bond markets could be substantial even if the central banks do, in the end, come back in to save the day.

Omicron

Secondly, the new COVID variant Omicron was discovered in South Africa, a situation that, understandably, wobbled markets as the potential for further market shutdowns and resulting economic hurt associated with such shutdowns increased. Interestingly, many of the digital/technology champions of the first COVID wave suffered over the same period. Companies such as Peloton and DocuSign sold off aggressively. However, the largest tech firms (the FAANGs) have so far held up relatively well. It is worth noting that things can change quickly in this space, especially for companies trading at historically high valuations.

China

The debt crisis surrounding Chinese property giant Evergrande continues to rumble on. Over recent days it has been confirmed that they have defaulted on their debt obligations. Though many are currently trying, the repercussions are difficult to quantify, but this is undoubtedly an additional risk factor for any tangentially related assets.

Conclusion

Hopefully, the above brief commentary highlights the dichotomy of historically positive inflows and investor sentiment versus an increasing set of risk factors, led by another Powell pivot. We could get another taper tantrum, seventies-style inflation, or a rerun of Q4 2018, and the bottom line is nobody really knows what comes next because the circumstances are unprecedented. It will come as no surprise to hear that we expect diversification to play an ever more critical role in any outcomes in the coming months and years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same Group, METNOR Group Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 390.12.21