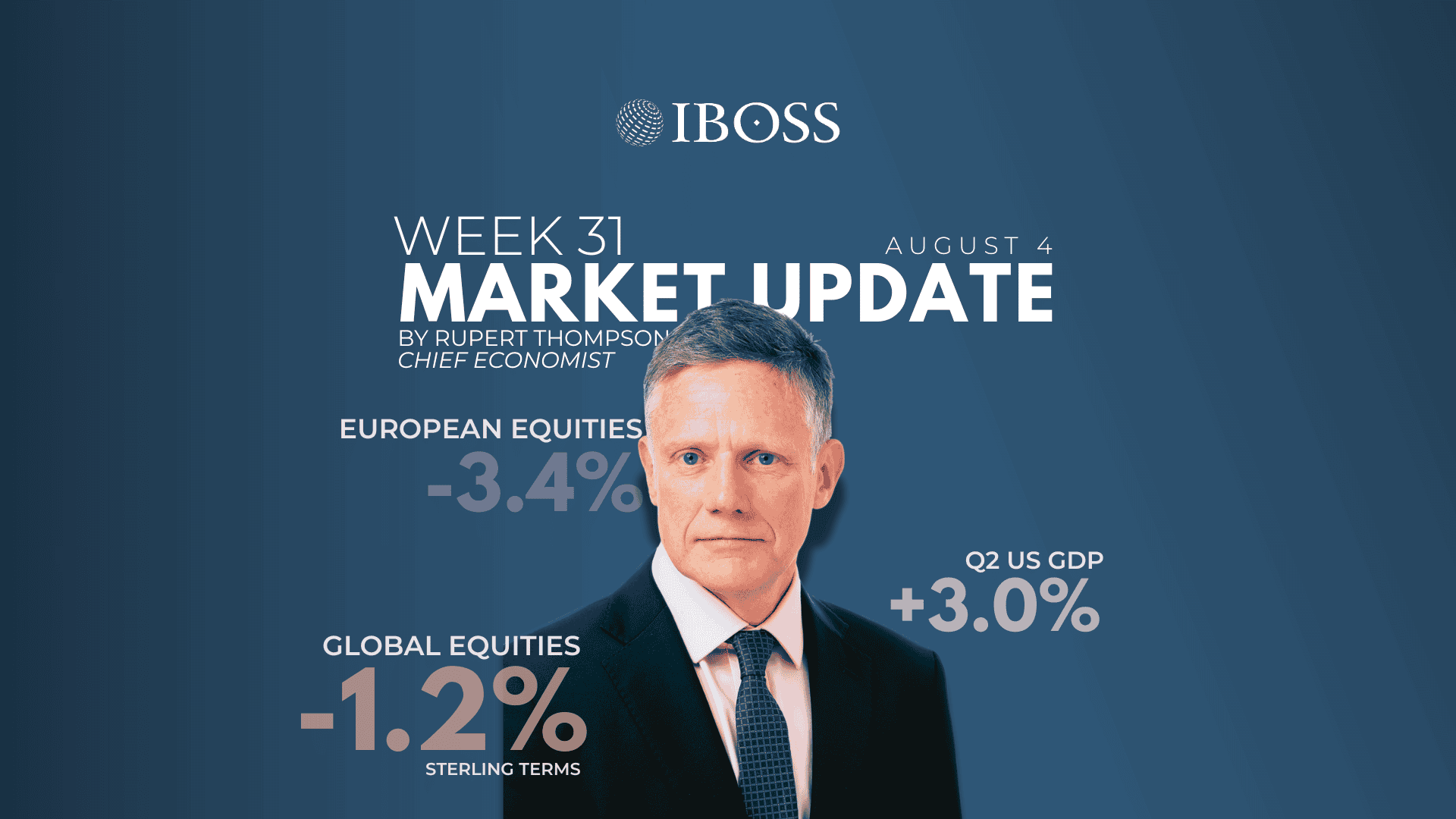

Last week saw equities end the week lower for the first time in over a month. Global equities fell 2.1% in local currency terms and a rather smaller 1.2% in sterling terms as the pound weakened against a stronger dollar. Europe fared worst, falling 3.4% in sterling terms while Japan fared best with a 1.0% gain; the UK and US were down 0.7% and 1.2% respectively.

Bonds performed as one would have hoped, providing an offset to the falls in equities. US Treasuries and UK gilts saw yields decline 0.1-0.2%, leading to positive returns of 0.8% and 1.1% respectively.

So what was behind the market’s abrupt change in mood? In three words, US nonfarm payrolls. Friday saw payroll employment post a weaker than expected gain in July and more importantly there were substantial downward revisions to previous month’s increases.

The data now show unequivocally a marked weakening in employment growth in recent months although the unemployment rate has risen only a little and remains on the low side at 4.2%. This is because of the crackdown on immigration which means the labour force is barely growing any longer.

The data triggered an immediate response, not just from the markets. In a sign of the shock – or maybe not, given it doesn’t take much to suffer this fate – Trump immediately fired the head of the government agency putting out the numbers.

Paradoxically, Friday’s numbers followed news on Wednesday that US GDP posted a larger than forecast 3.0% annualised gain in the second quarter, rebounding strongly from the 0.5% drop posted in the first quarter. In reality, however, this gain exaggerated the economy’s strength, just as the first quarter numbers exaggerated its weakness.

The GDP numbers have been distorted big time by Trump’s tariffs and the front-loading of imports and build-up of inventories ahead of their implementation. The underlying picture – now backed up by the employment numbers – is that US growth has slowed significantly this year to a sluggish 1-1.5% from the robust 2.5-3% pace seen over the previous couple of years.

Wednesday also saw as expected the Federal Reserve leave rates unchanged – albeit with two of the seven Fed governors dissenting for the first time in 30 years and voting for a cut. Chair Powell’s message was little changed from the previous meeting and left markets continuing to forecast the Fed to lower rates in September.

But following the payroll data, markets upped their expectations for rate cuts. They are now anticipating the Fed following up their move in September with another 0.25% reduction in October.

Last week also saw a blizzard of US tariff announcements as the 1 August deadline for negotiating a trade deal to reduce the threatened reciprocal tariffs came to pass. These tariffs now go into effect this Thursday and show that markets became rather overconfident in the so-called TACO trade (Trump Always Chickens Out). The average US tariff now looks likely to end up being around 17%, up from all of 2.5% last year.

For some countries such as Switzerland, which seem to have been led up the garden path and ended up with a tariff as high as 39%, there were some nasty surprises. More positively, the mood music from the ongoing China-US trade talks remains quite positive and points to an extension of the current trade truce which ends on 12 August.

The damage done to US growth by the tariffs and the uncertainties surrounding them is now quite evident and their boost to inflation is also starting to become more apparent. The Fed’s favoured measure of core inflation was unchanged in June at 2.8%, some way above the Fed’s 2% target, and looks set to move back above 3% over coming months.

Last but far from least, we had second quarter results from four of the Magnificent Seven tech titans. Microsoft and Meta both beat expectations but Apple and Amazon both disappointed for one reason or another. We have now had six of the seven report – although the leader of the merry band Nvidia doesn’t do so until late August – and there are some conclusions that can be drawn.

First, the Magnificent Seven moniker is looking increasingly past its sell-by-date given the diverging fortunes of these companies. We highlighted in last week’s commentary the big divergence in performance year-to-date and this continued last week. Meta and Microsoft ended the week up 5% and 2% respectively while Apple and Amazon were down 5% and 7%.

Second, the big question of whether their massive and still increasing AI-related expenditures will prove worthwhile is still unanswered. Meta, Alphabet and Microsoft do now appear to be reaping some reward but as yet far from the size needed to justify the AI-related arms race.

Third, as we saw in the spring sell-off and indeed last week, which saw the initial gains of Meta and Microsoft reduced substantially by week-end, these companies are far from immune to the wider fortunes of the economy and the market. We have been warning rather prematurely of renewed market volatility over coming months but recent events mean this continues to look likely.

The unusual speed of the rebound in equities is grounds for some caution, particularly as the recovery has been very narrow in breadth and led by increasingly few companies. Valuations which are back on the high side (although as ever only down to the US), along with the marked slowdown in US growth and continuing uncertainty over the impact of the tariff hikes and prospects for Fed policy, are all grounds for a pause and possibly renewed volatility in the thin markets looming with investors now headed to the beaches.

That said, this coming week at least could be a quietish one with no major macro releases. The only big event – at least for UK investors – is the BOE meeting on Thursday which should see rates reduced a further 0.25% to 4.0%.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 228.8.25