As global equity markets continued their ascent through October, we thought it would be worth reflecting on some of the factors influencing markets, as well as addressing some of our concerns that continue to lurk in the background, despite the recent positivity.

Chinas Evergrande woes

Though the Evergrande situation has partially faded out of mainstream media’s focus, the situation continues to rumble on in the background. So far, the Chinese property giant has avoided outright defaults by making overdue payments just before the grace period ends. To do this, they have sold various assets, including a UK-based electric car business; however, the firm has struggled to sell its eclectic mix of other assets.

We mention these points to stress that the Evergrande situation has yet to reach a head, and therefore the final impact is still unknown. The potential for defaults has caused a relatively minor stir, but there is genuine potential for contagion outside of China for fixed-income and equity markets. We do not know the ultimate destination, but we are cognisant of the risks, which could remain for some time longer.

A New Fed chair – more accommodative than ever?

Investors have become increasingly aware that central bankers have heavily supported risk assets throughout the last decade. The constant debates about whether the US central bank is looking to tighten monetary policy have also endured since Q4 2018, and the infamous ‘Powell pivot’. The Fed has maintained a consistent approach to monetary policy irrespective of chair, which in a nutshell has been super-accommodative.

As Biden looks to elect a new Fed chair, markets have begun to look at the prospective candidates closely to assess how hawkish or dovish each one is and extrapolate the path of interest rates from there. We suspect the outcome for monetary policy will primarily be the same regardless of whose name is above the door. It is worth remembering that Jay Powell was considered a more hawkish candidate before his confirmation than many of his peers. It seems that for whatever reaso once you are the one leading the Fed, and not just feeding information into the committee and using your single vote, your mindset changes. Watching markets fall because of your actions as Powell experienced back in 2018 seemed to be a life-changing experience for him, and he has been dovish ever since.

Ex Chair Janet Yellen recently commented that any new chair would need to be sensitive to equity market participants. This comment supports our view that whoever ends up as chair will face the same problems as their predecessors and will more than likely be beholden to the equity market.

COVID – is it too early to look in the rear-view mirror?

Though the human impact of COVID-19 remains a very present threat, investors are looking at the lows of 2020 in the rear-view mirror as global equities rose on average 75% from the 23rd of March 2020 and are 27% higher than pre-COVID lows. Additionally, investor flows have been highly positive into risk assets as flows into global equities exceeded 1 trillion dollars in 2021, more than the previous 20 years combined.

In this environment where investors have a seemingly insatiable appetite and positivity is in abundance, we look to identify factors that could shake this mindset. COVID-19 remains one such factor. Though most countries have now adopted a less stringent policy regarding COVID restrictions, Hong Kong and China continue to follow a zero-tolerance policy. These countries remain a substantial part of the global supply chain, a situation that could prove problematic for specific geographies and companies which rely on Chinese imports/exports. Additionally, there is always the potential for further lockdowns across almost all geographies.

Income stocks – the lost decade

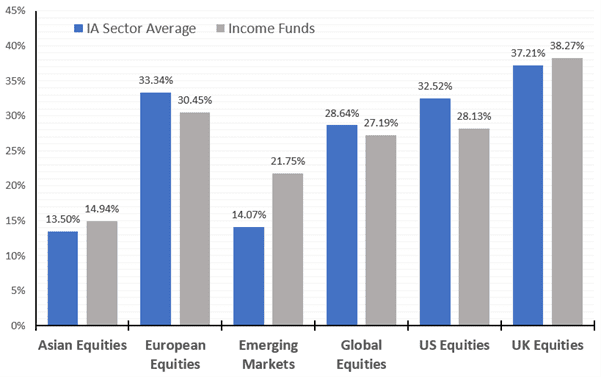

We thought it would be interesting to highlight the recent performance of income producing assets. Following more than five years of significant underperformance relative to their whole of market peers, income-producing stocks have performed relatively well over the past year. Though still underperforming relative to global equities, the table below demonstrates that allocating to dividend-producing stocks within the UK, Asia and emerging markets has been a not-insignificant benefit.

We have warned for some time that relying on any one approach to investing can result in prolonged periods of underperformance as often as outperformance. Equity income funds are have been a good example of this. Though they have underperformed versus the currently popular growth/technology investments, income orientated investing could see a stronger relative performance as the covid headwinds hopefully dissipate. Additionally, we hold some funds in the income category to further diversify a portfolio’s positions.

1 Year performance of Income funds*

*Income funds defined as funds in the IA Sector with Income/Dividend or Distribution in the name as at 01/01/2021

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same Group, METNOR Group Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.