In any given era of investing, intuitively, it can feel like the investing backdrop should remain, if not constant, then at least something approximating to it. History, however, tells us that the only thing certain is change. This feeling of semi-permanence in the prevailing market conditions possibly stems from a sense of markets evolving in more of a linear fashion than is actually the case; the reality is there is no final endpoint. Like life, investing for most people remains a journey, not a destination.

For example, specific geographical equity markets or sectors can become popular for sound economic reasons that make perfect sense at the time. Investors and commentators then often look for reasons for a trend to continue, while the original investment case frequently and conveniently morphs into a new one. This may be justified, but it’s a potential early warning sign of the risks of a valuation correction at some point down the line.

An investor owns an asset because, however they go about it, will have reasoned an investment case for doing so. It can be hard to re-analyse objectively and either reduce exposure or sell it altogether. In an update with a company, even if you have access to the entire C-suite, it is improbable that they will tell you the investment case for their stock has deteriorated to the point you should sell it. The same often goes for sectors and countries; will a Chinese government spokesperson talk objectively about China’s economic prospects? By the same token, will an American government spokesperson speak objectively on China’s economic prospects?

The answers will usually be no and no. If you want objectivity, it’s essential to find people who have no reason to favour one asset or outcome over another, and that’s probably harder than ever.

The Rise of the (Passive) Machines and Social Media

Few people would argue against the statement that passive investing, in all its myriad forms, has dramatically affected global markets. Passive investing started in the seventies but has grown exponentially during the last decade. Passive flows have changed how we perceive an index such as the S&P and how we should value the companies within it.

An ever more significant percentage of investors never look at the balance sheet of the companies they invest in, nor do they spend time looking at the investable qualities of individual stocks. This lack of granularity has not necessarily hindered many investors’ returns but has often enhanced them. The question we need to revisit constantly is whether these returns are due to conditions that still prevail or conditions that may have changed?

With the simultaneous rise of social media influence on markets, which enables narratives to become more quickly embedded in the investor psyche, the components for rapidly changing market conditions have never been greater. We just have to look at Silicon Valley bank to see how quickly confidence can evaporate in an asset, or institution, and how quickly people can move their investments from one place to another.

Who to believe?

Crucially, at this current juncture, we are also in the early innings of the post “lower for longer” period for interest rates, primarily predicated on renewed inflationary pressure. With an overreliance on their models and possibly one of the worst examples of groupthink in central bank history, the Federal Reserve, the ECB, and the BoE all called inflation completely wrong. In fact, for the avoidance of doubt about their ability to forecast inflation (and therefore interest rates) in June 2022, Fed Chair Jerome Powell said, “We now understand better how little we understand about inflation“.

So, if we are looking for guidance on inflation, we should probably limit our exposure to this particular group of experts. Whilst the inflation outlook might vary from country to country, the tailwinds for a sustained resurgence are considerably more abundant than the headwinds.

Just some of the inflationary factors we would cite are:

- Wars/geopolitical conflicts

- The ‘just in time’ supply chains are replaced with ‘just in case’ ones

- Greenflation (prices rising from green policies)

- The outcome of poor energy policies and a historical lack of investment in the commodities needed for today

- Foodnationalism

- Deglobalisation

- Reshoring/Friendshoring

- Shrinking labour pools

Apart from the diminishing base effects of the pandemic, and the immediate commodity price reaction to Russia’s invasion of Ukraine, the only major deflationary factor we see is technological advances, specifically Artificial Intelligence (AI). Whilst the impact of this phenomenon will be enormous, can it really offset all the positive inflationary factors?

Where are we now?

One common error investors make is to directly read across from a company with a good business model to a good investment opportunity, or from an economy in a country that is strong and, therefore, the best place to invest. Even the best companies or countries eventually become what can be described as ‘fully valued’ or just plain expensive.

However, few investors can consistently demonstrate an ability to both realise this moment and then, just as importantly, act on it. One of the difficulties in making this kind of call is that companies can reach their optimal price for their specific circumstances over a vast array of timescales. To further complicate matters, to a varying degree, all companies are similarly subject to multiple factors that will essentially be outside their control. These could extend to either sectors or geographies or, in an extreme situation, both simultaneously.

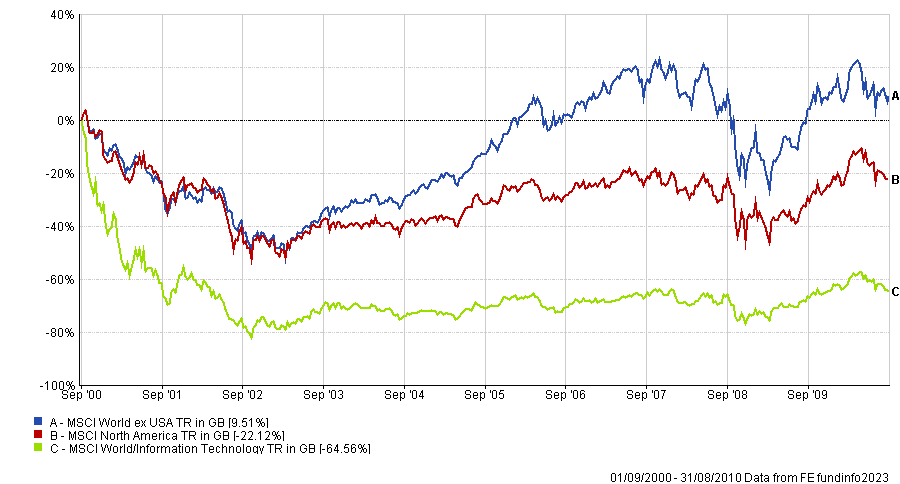

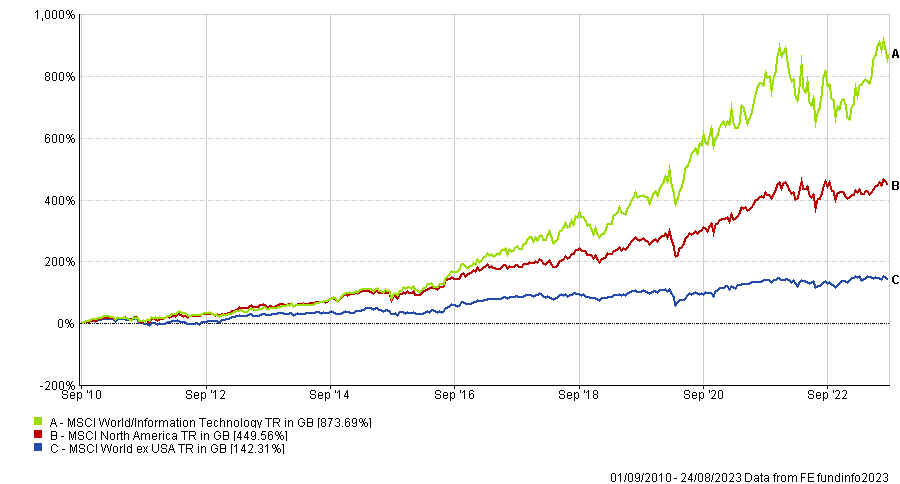

Examples of this could be new anti-trust rules, nationalism, positive geographical discrimination, changes in public opinion, or Artificial Intelligence, to cite the current in-vogue investment case disrupter again. A geographical and sectoral example of the significant changes to the investing landscape was the decade from September 2000 to August 2010 (fig 1). One of the principal countries to avoid was the US, and the sector allocators bete noire sector was information technology. What has followed has been an incredibly strong period for both the US as a whole and US tech stocks in particular (fig 2).

Throughout much of the period shown since September 2010, the investing backdrop has had the following characteristics:

- Increasing globalisation

- Fiscal largess from tax cuts and handouts

- Little (if any) regard to burgeoning debt piles

- Low inflation

- Low interest rates even going negative in some cases

- Markets are convinced by the actions of central banks that they will come to the rescue if asset prices fall

Most of these factors have now ceased or are in reverse. What this means is – not that investment opportunities have gone, in fact, far from it. However, it does mean we must look for winners amongst countries, sectors and individual companies who will benefit from the seismic and ongoing changes to the investing backdrop. That will undoubtedly include significant investment in both the US and their still dominant tech sector. However, the net will have to be cast much further afield for investors to give themselves the best chance of capturing the available investment returns.

In a future blog, we will highlight the best opportunities in the investable world right now.

Global Equity Performance 2000 – 2010 (fig 1)

Figure 2: Global Equity Performance 2010 – 2023 (fig 2)

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 237.8.23