Passive or Active – for us, the aim remains the same

Both our Core and Passive Managed Portfolio Service (MPS) have the same aim, namely ‘To beat the relevant benchmark over as many periods as possible, with less than benchmark volatility, lower drawdowns and across all risk ratings’.

Based on our evidence collated over twelve years, we expect our Core range to outperform our Passive range and both to exceed the respective benchmarks. There will, of course, be periods where this isn’t the case, and this could even be over several years if a trend persists, but where we feel the risk/return function has broken down. It is worth reiterating that although our Passive range holds passive funds, there is active fund selection within equities at a geographical level and cap size level. Within the Fixed Income portion of the portfolio, the duration and credit quality are subject to an active overlay.

When should we expect the IBOSS Core range to outperform the Passive and vice versa?

Certain market conditions will favour one approach over the other at different times from both a style and geographical standpoint. In periods where the US outperforms the rest of the world – as has been the case many times over recent years – our Passive range benefits from its relative overweight to the region. Similarly, when growth ascends relative to value, which again has often been the situation in recent times, our Passive range is likely to outperform our Core approach.

It is not just the IBOSS propositions that exhibit these characteristics. We have witnessed periods of strong performance from the likes of Vanguard’s Life Strategy range and other passive offerings. Understandably some investors have extrapolated the outperformance of passive indices far into the future. We would caution that ‘recency bias’ seems to have crept into the investor psyche and we must be open to the possibility that the next decade will not necessarily be a repeat of the last.

For example, Asia and many emerging markets, spearheaded by China, could be better placed for economic growth than much of the developed world. This is a view we at IBOSS subscribe to and believe that it is a mistake to write off any region for the long-term. The UK would be a prime example of an underloved area of the world, but one which undoubtedly has excellent companies within it. The vast majority of these UK companies will remain excellent regardless of any Brexit outcome. As ever, we feel that sufficient diversification is necessary to take advantage of these opportunities.

![]()

Past performance is not a reliable indicator of future performance, please refer to our important information slide for a full list of risk warnings.

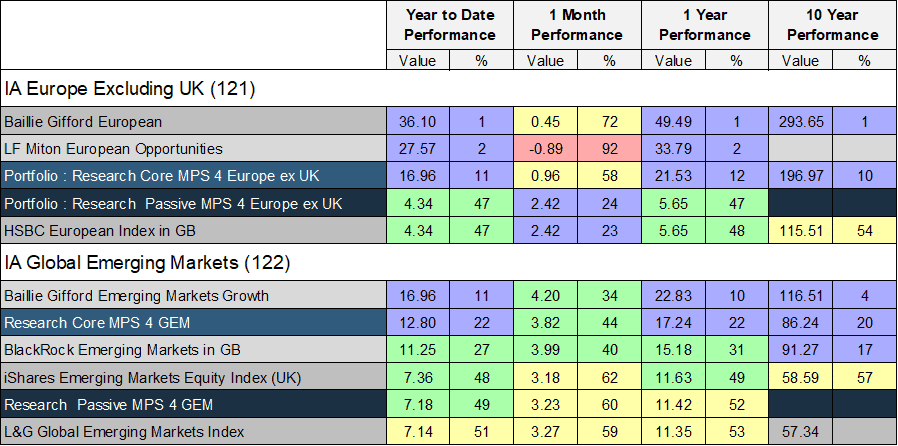

Not all Indices are representing the same kind of stocks

The HSBC European Index, which is the fund we use for our passive European exposure, has a natural tilt towards value. That is why, as can be seen in the table (above), it has done exceptionally well in the recent and dramatic rotation from growth to value. Conversely, we have seen our two active European funds struggle somewhat, especially the Miton European Opportunities fund. This period is obviously very short, but it is at times of violent market rotations or falls that you can often best observe a fund’s characteristics.

Within our Core range, we aim to blend different types and styles of funds. The table (above) demonstrates that the combination of our European funds – Miton, Baillie Gifford and HSBC – provides significant diversification. A potential catalyst for a sustained change in the momentum of growth stocks could be triggered by a genuine breakthrough on the vaccine front. This could reverse the appeal of some WFH shares which have been seen as both growth and latterly defensive plays. In these conditions, we would expect our Core range to outperform as hopefully some of the value orientated and the truly active managers see their stocks rerate.

The Conclusion

If the price is the overriding driver for the client, then our Passive range offers a very attractively priced proposition and has historically displayed strong risk-adjusted returns. If a client is price-conscious but also wants the best risk/return characteristics IBOSS offer, then the Core range has delivered that thus far. Of course (platform permitting) it is possible to blend both ranges, and this approach has been proving popular in recent months. There is no one size fits all, but whatever you, the adviser, and your clients’ investment needs are, we potentially have solutions for you.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients.

The MPS range portfolio performance is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 363.11.20