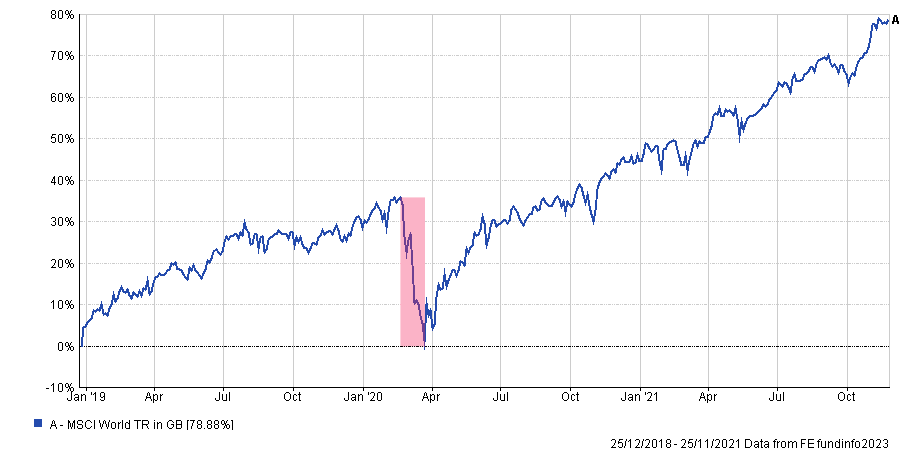

It has been a long time in markets since Christmas 2018, when the original ‘Powell Pivot’ abruptly stopped the market falls and a great bull run in stocks began. In fact, it ran for thirty-five months (fig.1) and all the way to his rude awakening about inflation, disturbing his slumbers at the end of November 2021.

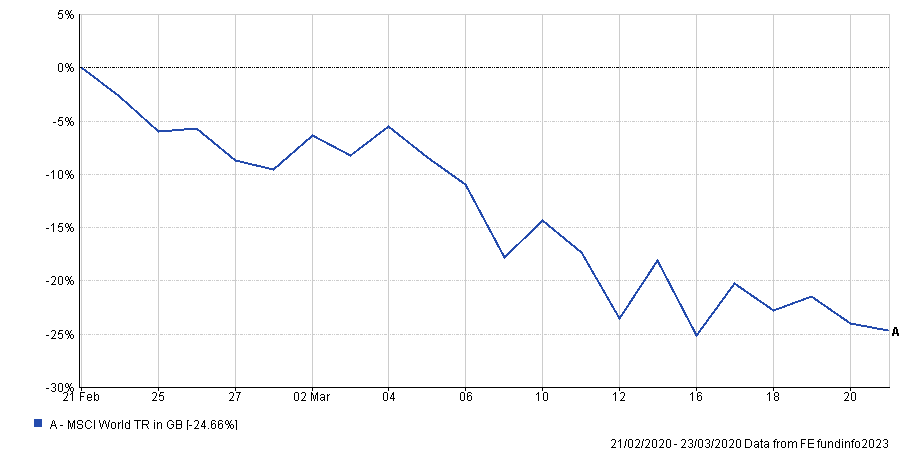

There was only one significant drawdown in this golden period for investors: the Covid slump, which lasted precisely one month (fig.2). There was a very particular reason why the markets fell so dramatically for that brief period between 21st February and 23rd March 2020, namely, nobody could be sure the Fed had their back, especially the Fed themselves. Once they announced they would buy corporate bonds it turned out to be the green light and that’s all the markets needed to know; from then on, it was very much game on!

MSCI World 25/12/2018 – 25/11/2021 (fig.1)*

MSCI World 21/02/2020 – 23/03/2020 (fig.2)*

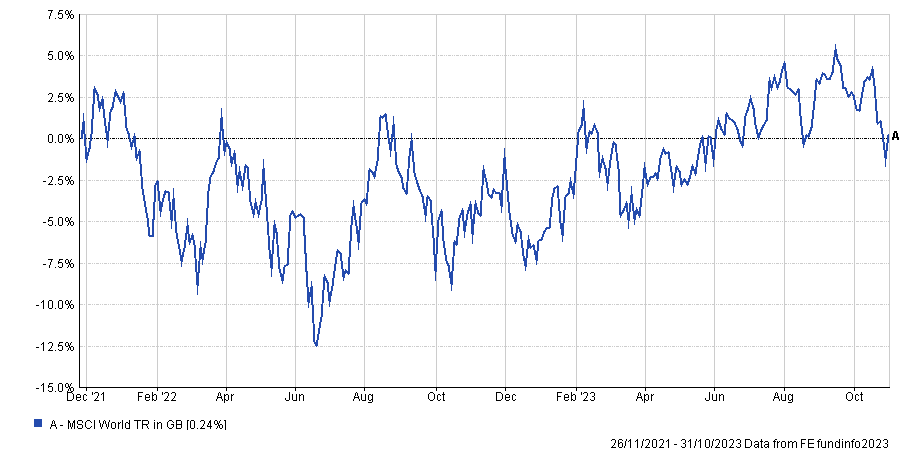

Once Powell realised he had been asleep at the wheel on inflation, he took every opportunity to warn the world of the risks of it getting out of control. Within relatively short order, the ECB and the BoE joined in, and the fight against inflation became the number one issue for many of the world’s central banks. To the general dismay of investors, this led to the period (fig.3) where, in aggregate, stocks went absolutely nowhere but with larger drawdowns and increased volatility. The Fed ‘put’ was absent, and every effort by the markets to climb the wall of worry was thwarted.

MSCI World 26/11/2021 – 31/10/2023 (fig.3)*

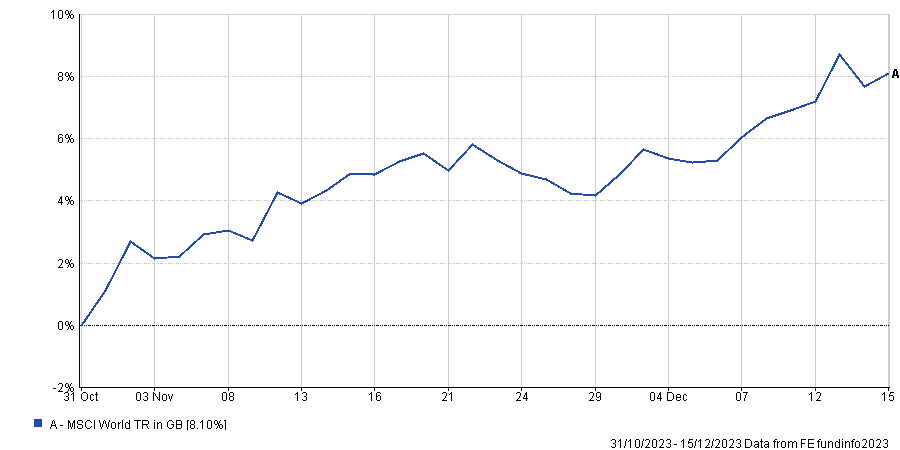

That all appears to have changed at the end of October 2023 (fig.4).

We wrote a piece in early November, last month, entitled “Dress Rehearsal?” where we looked at the possibility of us being in another new central bank era. A few short weeks down the line and it appears that it wasn’t a dress rehearsal, and Powell signalled it really was safe to go back in the water with his speech on the 13th of December 2023.

MSCI World 31/11/2023 – 15/12/2023 (fig.4)*

Some of the ‘Z’ listers from the Fed have since tried to talk down market expectations, and certainly, Lagarde and Bailey were less dovish than Powell, but none of them dictates global markets; that’s still the head of the Federal Reserve’s job, and he has spoken unequivocally.

So what of the fears?

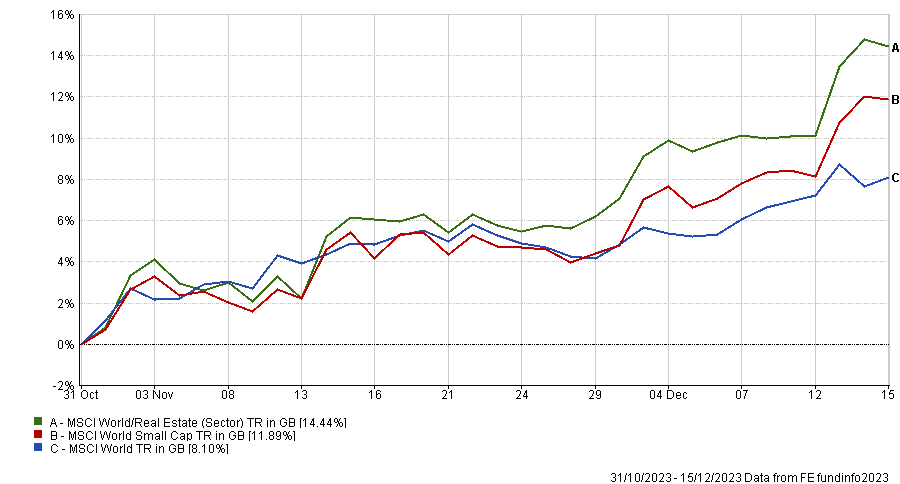

Since the 31st of October, the markets have been on an incredible run, with equities rallying, led by small caps and real estate jumping higher (fig.5).

This is all well and good for now, but we have remaining fear that inflation will return at some point later in 2024, and that will cause these central banks new problems. We also question central bank independence in what will be potentially the most bitter, controversial and polarising election in US history.

We limit ourselves to thoughts on what the Fed may do in reaction to this backdrop and we feel, if anything, they will be more dovish than maybe the data would dictate, and that would be, again, good for risk assets. At some point later, the inflation piper would need to be paid, but that’s unlikely to be a 2024 issue.

MSCI World Equity, Real Estate & Small Caps 31/10/2023 – 15/12/2023 (fig.5)

Current IBOSS Positioning

We had already been increasing our exposure to small and mid-caps stateside and in the UK, our managers have a semi-permanent weighting to this space. While a negative contributor for much of 2023, this small-cap exposure has benefitted us following the sharp reversal in fortunes of large and small caps. We expect this new trend to continue for some time yet.

In the bond space, we have been increasing duration across the portfolios and with possibly a further small increase in duration in some areas, we feel comfortable without relative positioning. Our reintroduction of property proved timely and, again, we expect a further modest increase in this sector, but still very much underweight relative to our own history, which stretches back to the very different world of 2008.

In currency terms, the dollar has been weakening significantly in recent weeks and that should prove to be a tailwind to much of our emerging market and Asia positioning.

Despite the recent rally in almost all risk assets, there remains good potential for much of the equity, bond, property and infrastructure markets. If you exclude the magnificent seven, prices are not that elevated and some are still relatively cheap. If the pound continues to behave reasonably, and a change of government here is unlikely to move the needle significantly, then there are certainly grounds for optimism.

The markets could perform well while the global news continues to be alarming, if not outright frightening. Share and bond prices are not moved by human joy or misery; they are moved by fear and greed. 2024, like every other year, will bring us endless risks and opportunities. As ever, humility is essential in investing, and a well-diversified portfolio is the acceptance of the fact that there is always much we cannot know. However, buying assets that are cheap relative to their history and relative to the alternatives but with catalysts to reprice is something we can take advantage of, and we see plenty of those right now.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 355.12.23