FOR PROFESSIONAL FINANCIAL ADVISERS ONLY

Behavioural biases have lured many an investor on to the metaphorical rocks, driven by their natural emotional human responses. As markets have continued to rise independently of stock fundamentals, the siren calls have simultaneously grown louder. Fear of missing out (FOMO) is an incredibly powerful force, as the strength of will of all but the most judicious collapses under the weight of the ‘this time it’s different’ argument. As investment managers, we take the behavioural facet of investing very seriously. What this means in practice is that we try to ensure that we remain fully diversified, despite market pressure to hold an increasingly concentrated basket of assets.

Perhaps the most significant behavioural bias affecting investors currently is recency bias. This is the tendency for people (and investors) to more accurately remember recently presented information. For example, if you are asked to memorise a list of items then you are most likely to recall the items that you studied last. From an investors point of view, this means that investors can be prone to placing a larger emphasis on things that have happened in the recent past and extrapolate that data into the future.

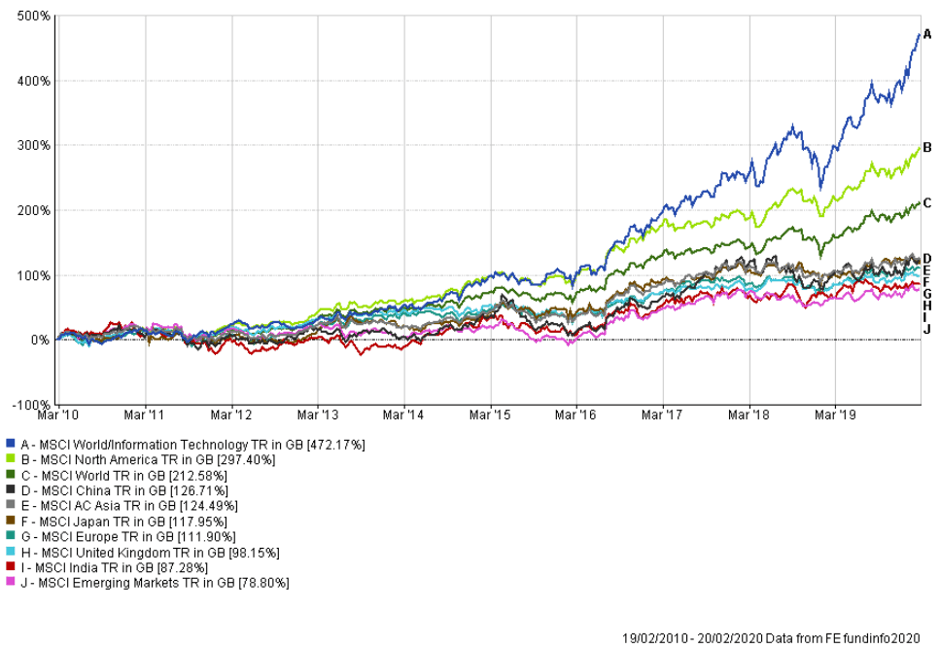

We feel this recency bias is pertinent to some of the areas of the market which have performed the best over the last decade. We have previously written at length about the domination of US technology stocks and their increasing impact on the direction of US stock markets. 2019 was perhaps the starkest example of the supremacy of US tech companies, where Microsoft and Apple accounted for almost 15% of the S&Ps returns and only 5 stocks now account for 19% of the index. This is the highest percentage on record and is, as you would expect, reflected in both passively managed and actively managed portfolios.

The trend however isn’t confined to last year and US stocks, led primarily by technology stocks, have outperformed for most of the past decade. Over this time period many investors have become more comfortable and confident in their technology positioning. It is no coincidence then that many have become increasingly exposed to these areas at the same time they are trading at record high valuations.

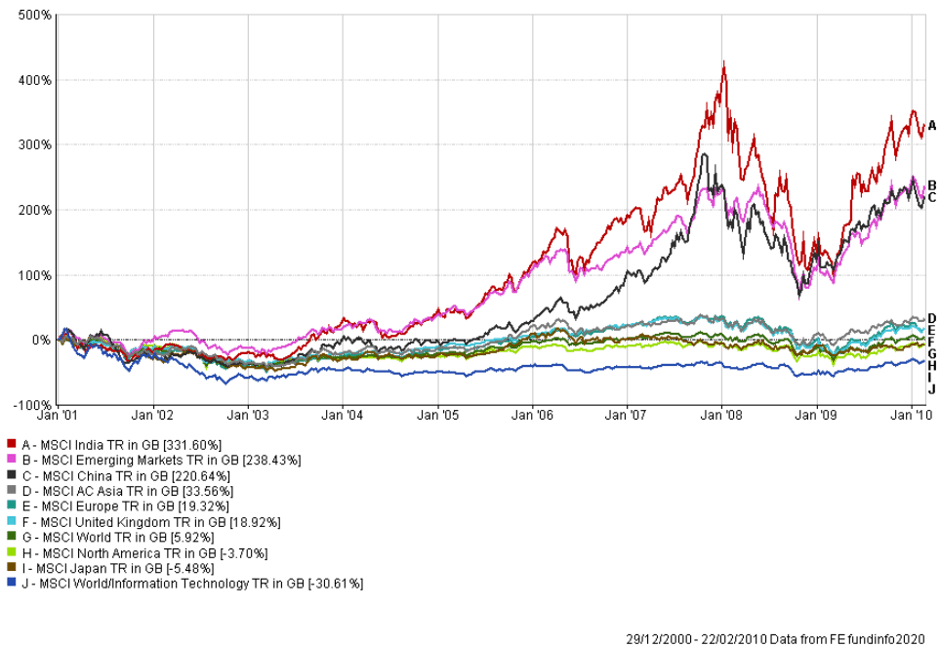

The risk here is that many investors put too much emphasis on the recent past and are almost blindly investing in a basket of very similar assets, on the basis that tomorrow will look the same as yesterday. Although 10 years isn’t by any means short term, the last decade can be characterised by two major factors; namely loose central bank policy and accelerated globalisation. This method of central bank intervention has bid up asset prices, but some assets have benefited far more heavily than others. Technology stocks, US stocks, and growth stocks have all outperformed a rising market thanks to this very specific tailwind. However, we need only look back to the decade prior to see that technology and US equities haven’t always been the one way bet they currently seem. In fact, investing in technology between 2000 and 2010 saw a loss of 31% against a positive return of 6% for the average global equity (MSCI World). Over the same time period, value stocks significantly outperformed growth stocks, something that is currently viewed as an impossibility, with the former generating healthy positive returns of 30% against growth returns of minus 16%. Globalisation and the integration of international supply chains probably peaked in 2019, neither globalisation nor central banks are likely to be as effective at moving market prices in the coming years.

It is worth considering that in the 2000’s many investors, like investors today, were slowly but progressively being lured by the sweet siren call of recency bias. The song was however very different. US and global equities were viewed as wasted investments, technology was a liability and it was an accepted norm that valuation was the key driver to investment returns – value over growth.

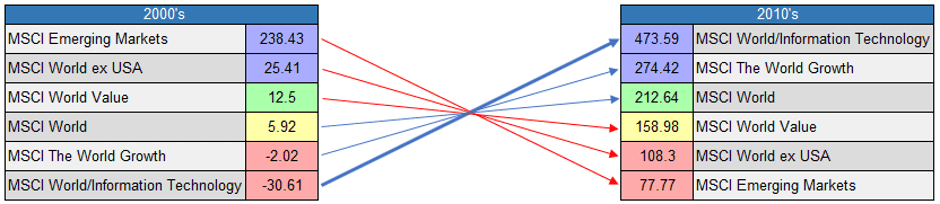

The chart above demonstrates the complete reversal of those trends in the next decade as, period by period, investors who had followed the winners in the 2000’s lost out significantly heading into the 2010’s. This is reflected from a fund manager perspective too. Many of the most popular managers of the 2000’s (largely due to their performance figures) struggled in the next decade – see Tom Dobell and Alistair Mundy – not to mention the swath of popular 2000’s managers who are no longer in the industry.

As ever, we are not looking to time markets, but it is vital for investors to consider the emotional side of investing and look forward rather than backwards. We would suggest that there is a high probability that whatever the next decade holds in store, it is highly unlikely to look like the last one.

Finally, in Greek mythology Odysseus managed to successfully navigate and conquer the siren calls (which rendered men incapable of rational thought) by lashing himself to the mast, plugging his men’s ears with wax and ordering them not to change course under any circumstances. It could well benefit investors to metaphorically adopt a similar position. Lash yourself to the mast of diversification and under all circumstances ignore the sugared siren call of recency bias. After all, the prospective returns of technology stocks are known to render all investors incapable of rational thought, but then maybe this time it’s different?