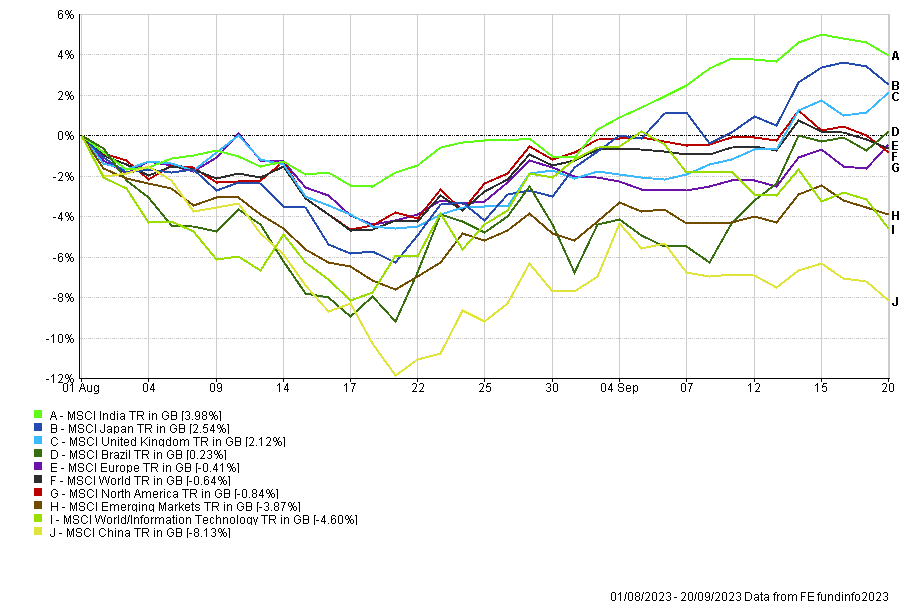

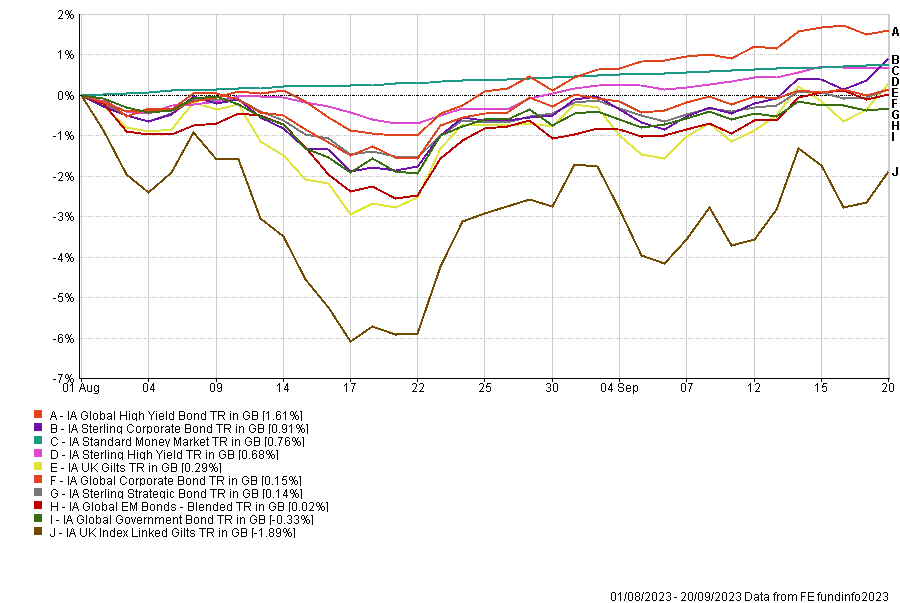

There were broad equity losses in the first three weeks of August, followed by a rebound from the lows. However, at the time of writing (21/09/23) and post the latest Fed press conference, equity markets globally (fig.1), particularly the US, have sold off heavily. At the same time, global bond yields (fig.2) have been falling, but have responded to central bank policy and words by reaching new cycle highs in the US.

Global Equity Performance – 01/08/2023 – 20/09/2023 (fig 1)*

Fixed Income Performance – 01/08/2023 – 20/09/2023 (fig 2)*

We have been highlighting for some time, that for most investors in multi-asset portfolios, three factors will drive their investment outcome:

- The starting price of their equity and bond baskets

- The closing price of their equity and bond baskets

- Changes in the relative value of their currency

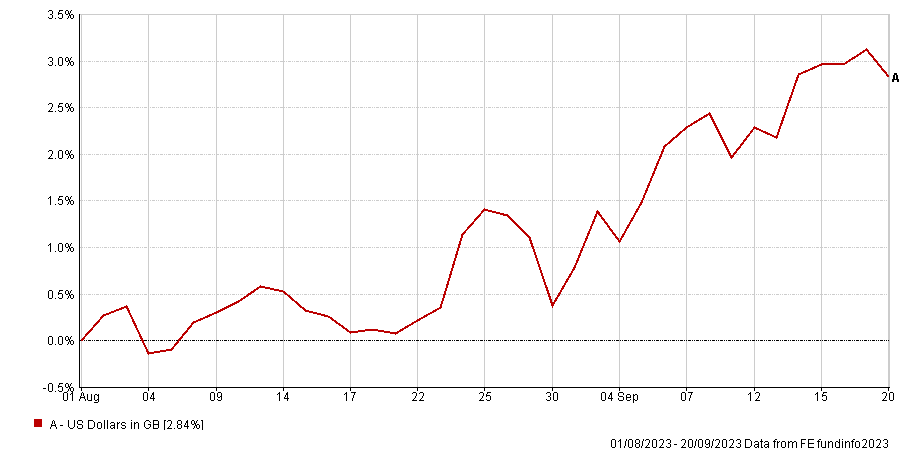

Any, or all three, of these factors have the ability to add or destroy investor value with almost no limits if a situation is extreme enough. This isn’t meant to be unduly alarmist; it merely acknowledges the obvious significance of the first two factors but highlights the one so often overlooked, which can be just as important as the first two. Thankfully for UK investors, the recent market turbulence coincides with a renewed period of relative sterling weakness against the dollar (fig.3). This boosts the overall returns for clients from overseas assets or stocks with overseas earnings.

Dollar Performance – 01/08/2023 – 20/09/2023 (fig 3)*

Ongoing confusion in markets, much of which is caused by the aberrative effects of pandemic fiscal and monetary policies, looks set to continue for the foreseeable future, as does elevated volatility. The uncomfortable truth is there is no playbook for central banks and governments which contains a chapter on ‘enlightened monetary and fiscal policy for the 21st century following a pandemic’.

So, even if governments and central banks act in good faith (not a given) on the data as they see it, errors will be made, and the wrong conclusions will be drawn. We only need to remind ourselves of a direct quote from Jay Powell, US Federal Reserve Chairman – “we now understand better how little we understand about inflation.” By the time he uttered those words, many market participants had already come to that conclusion.

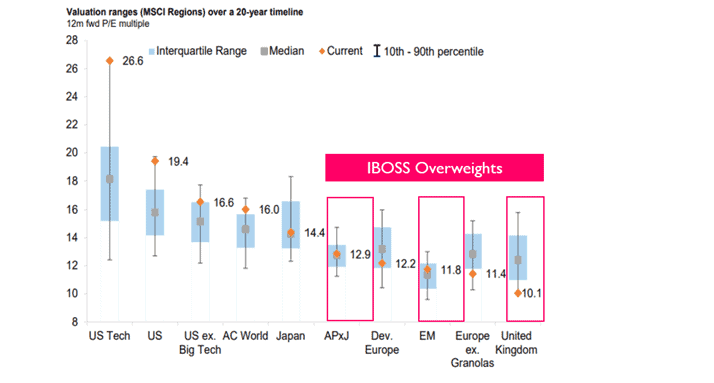

What we do know is, which markets are cheap and which are expensive in absolute and relative terms (fig.4). We need to concentrate our efforts on understanding where true relative lies and what could be a catalyst for a given asset to move significantly either up or down in price. As the chart shows, parts of the US market remain extremely expensive, but this is limited to a relatively small number of stocks. Many attractively priced companies have not ‘benefitted’ from the AI hype, or the retail investing frenzy driven by the fear of missing out (FOMO).

For years, some investors saw these growth assets as almost risk-free, especially after the infamous Powell pivot of Q4 2018, where he quickly changed Fed policy to save the equity market. In 2023, it is no longer just America proclaiming to its electorate that it is putting its own interests first; it is becoming a popular vote-winning strategy around the globe.

Regional Equity Valuations Relative to 20-Year History (fig.4)

Source: Kingswood

Source: Kingswood

Market conditions going forward, rather than being seen through the rearview mirror, must be different. This new era will bring new winners both sectorally and geographically. Diversification is more critical than ever since there are so many factors now to consider rather than just the central bank reaction function. The evolving macro backdrop should present the ideal hunting ground for active managers to harvest alpha. This is in contrast to merely following the trend set by old-world dynamics, one which often favoured a passive approach.

A final point on the new paradigm is that cash has been paying the highest interest levels for decades and there is always a temptation to move money into what appears to be a sure winner. However, moving into cash is never the actual issue, the tricky part is knowing when assets other than cash will give you greater returns. Whatever any number of experts might suggest, it is unarguable that market timing, even for people who live and breathe the markets, is notoriously difficult.

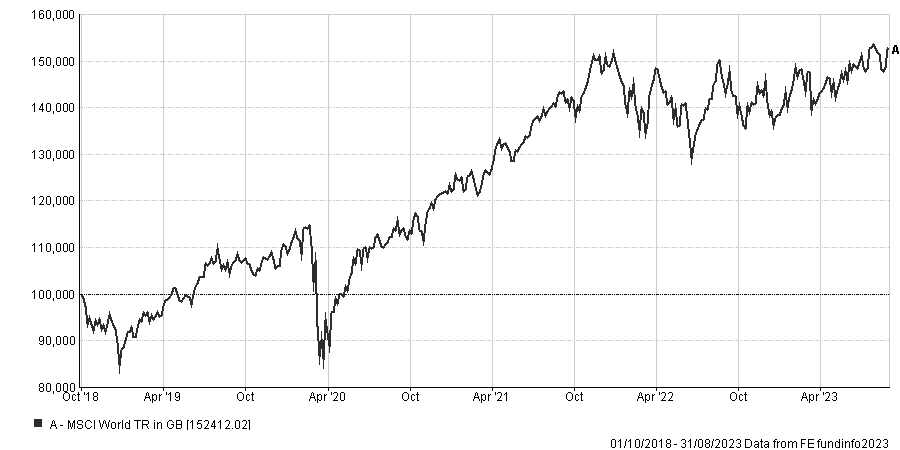

As an example, take the period around, and since, the pandemic (fig.5). The reasons equity markets recovered and powered on were central bank and government policy. We believe there is a reasonable degree of probability that at some point when economies and markets falter sufficiently, central banks and governments will once again find ways to rekindle animal spirits. It doesn’t really matter that we don’t know what the catalyst will be; few predicted that in 2020 it would be the Fed buying corporate bonds, or in 2018 it was basically just the speed of equity market falls to cause a total policy reversal.

We do know that if you were sitting on the sidelines in 2018 or 2020, you wouldn’t have realised what the catalysts were or when they would come.

£100,000 Invested in MSCI World Equities (fig.5)*

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 256.9.23