Markets decided to throw investors a curveball coming into 2022 as, following a largely positive 2021, investors began to consider the impact of looming macro and geopolitical concerns. Though we will discuss a broader range of these in our monthly performance and market update (issued week commencing 7th February), the combination of inflation and the prospect of higher interest rates out of the US seem to have contributed most acutely to ongoing volatility.

The US Central bank (the Fed) stated last year that they are looking to increase interest rates and begin tapering – the process of reducing bond purchases and raising interest rates. Markets have historically performed poorly in the face of these proposed changes (see Q4 2018) and previously the Fed have quickly eased off as asset prices became threatened.

However, there is an additional factor in play this time around as US inflation rose from 1.4% in December 2020 to 7% in December 2021, the fastest rise since 1982. These remarkable inflation figures have had a direct impact on investor sentiment as they, and us, try to decide whether Powell will either:

- Raise rates to combat inflation and negatively impact asset prices, or

- Support asset prices by leaving rates alone but allow inflation to continue unchecked.

In theory, the results should already be in, following Jerome Powell’s address last Wednesday. However, his address seems to have left markets as unsure as they were previously as to the potential actions of the Fed come March. This continued uncertainty has contributed to the volatility of markets so far this year.

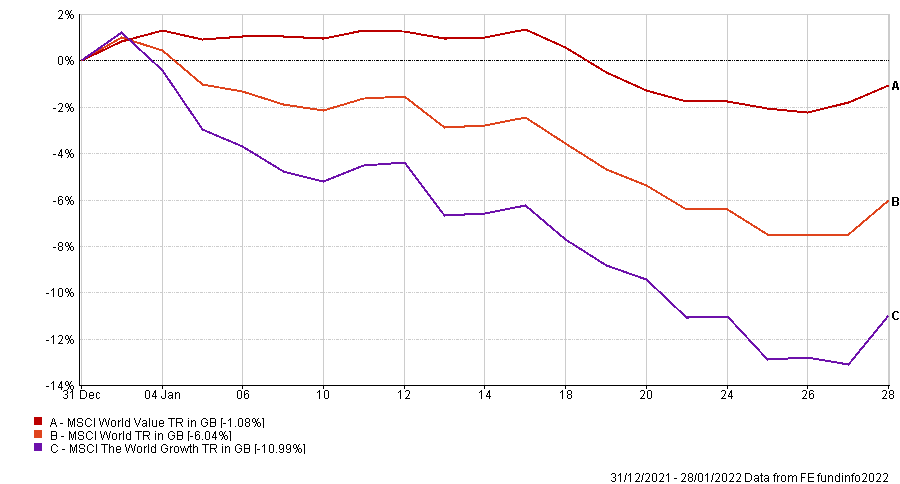

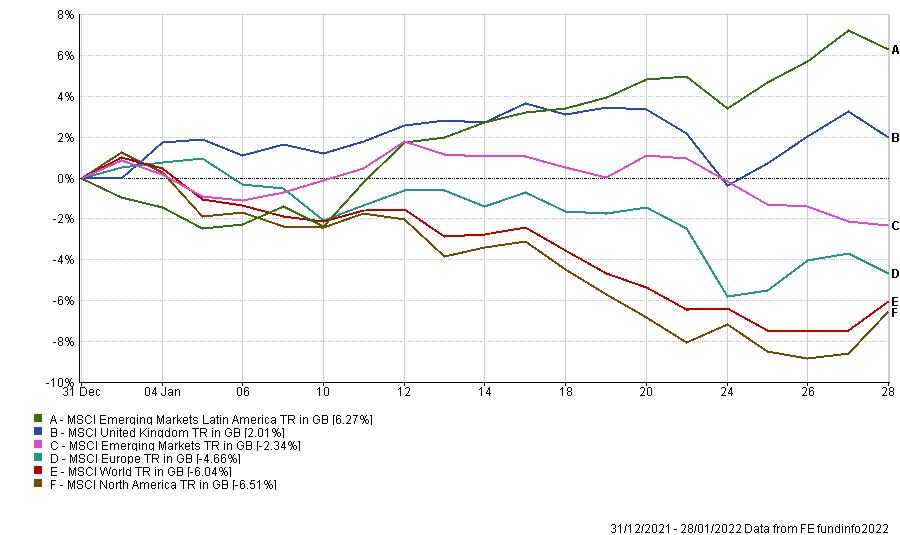

At this stage, it is tough to say how markets will respond for the remainder of the year, never mind the following week. However, it is worth considering that if inflation persists and Powell is forced to act, the winners could look very different from those of the past few years. A point evidenced by the year-to-date outperformance of styles and geographies that had been out of favour for many years, i.e. value, income, UK and emerging market equities (fig 1 & 2).

Year to Date Investment style – 31.12.2021-28.01.2022* (fig 1)

Year to Date geographical performance – 31.12.2021-28.01.2022* (fig 2)

Buy the Dip

As a final point, it is worth noting that there continues to be significant action from retail investors who, like many investors, have been conditioned to and have been historically rewarded for “buying the dip”. Interestingly, many of last week’s positive US stocks were primarily those stocks that are incredibly popular with retail investors. It remains to be seen whether this period becomes another opportunity or whether they are ultimately looking to catch the proverbial knife.

IBOSS Portfolios

At a portfolio level, we remain focused on maintaining high levels of diversification within each of our portfolio ranges. This focus has resulted in the portfolios being underweight US equities relative to peers and, therefore, slightly overweight to other geographies.

Nevertheless, the position has contributed to relative returns as an allocation to Europe, emerging markets and particularly UK equities has been beneficial versus North America year to date (fig 2).

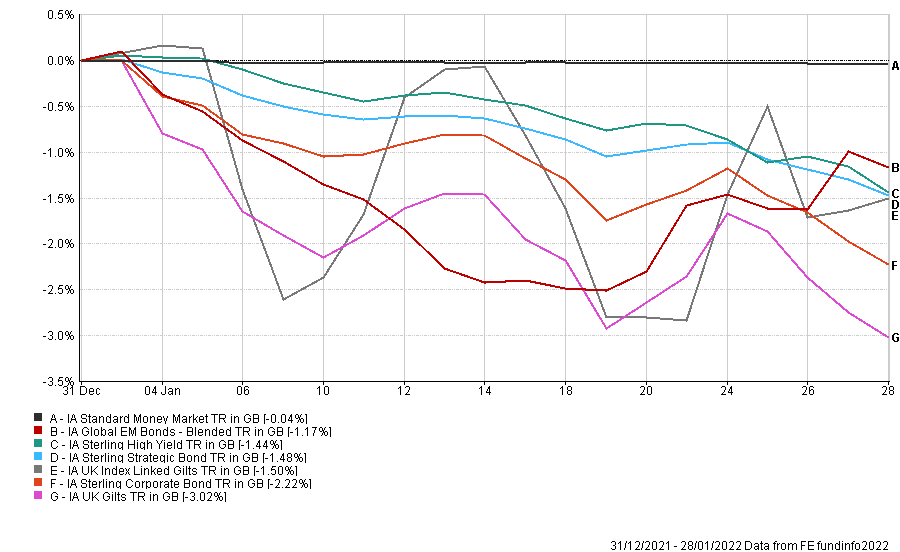

Though not strictly in the remit of this update, it is worth highlighting that most fixed income assets are negative year to date (fig 3), our dual position of low duration and cash has been particularly beneficial.

For more performance information, please get in touch with a member of the IBOSS team. Alternatively, look out for our aforementioned monthly performance and market update, scheduled to be released next week.

Year to date fixed income performance – 31.12.2021-28.01.2022* (fig 3)

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.