The Iran conflict isn’t a fire that keeps starting; it’s a peat fire that never truly goes out

The Iran conflict is like a peat fire: it rarely goes out; it simply burns below the surface. Ceasefires may extinguish the visible flames, creating the impression that the danger has passed, but the underlying fuel in the form of energy supply, regional rivalry, proxy networks, ideology and deep mistrust, continues to smoulder. When conditions change or one side thinks the time may be opportune, the flames inevitably return. This has been going on since the revolution in 1979 when the current regime swept into power. The conclusion we came to some time ago was that unfortunately without regime change, the conflict would roll on indefinitely and this remains our base case.

So, why isn’t oil hitting new all-time highs?

Several factors have conspired against those traders who believed all the ingredients were in place for $200+ oil. First and foremost, and perhaps counterintuitively, China has been the single biggest factor in keeping a lid on prices. It has done this partly by drawing down inventories but, more importantly, by simply not adding to them, creating a significant drop in global demand.

As ever, Chinese data is difficult to verify, but there is broad agreement that China’s restrained buying has been instrumental in preventing oil prices from spiralling higher, despite the unprecedented shock of the Strait of Hormuz being closed.

That, however, raises the inevitable questions. How long would China be willing to maintain this policy? And what would happen if it abandoned it and returned to stockpiling, even as prices were rising? A resurgence in Chinese demand at a time when supply remained constrained could quickly transform today’s surprisingly calm oil market into a far more volatile one.

War, what is it good for?

In almost any conflict, some people and companies will profit from dreadful humanitarian situations. This can be straightforward, such as defence contractors benefiting from a simple supply-and-demand dynamic, or energy and logistics suppliers seeing increased demand. In some cases, the same countries involved in bombing later participate in reconstruction programmes.

While it is often said that countries can profit from wars, in reality this is rare. What is more likely is that individual companies become beneficiaries, while the government itself seldom profits in the end. At a country level, it is usually far better to avoid military conflict wherever possible.

If we look at the two highest-profile conflicts still in play, Ukraine and Iran, both Russia and America have poured billions into trying to achieve their objectives, and many would argue both have failed to do so. Due to the length of the ongoing Ukraine conflict, it has so far proven far more costly for Russia than the Iran conflict has for the US. But neither conflict is yet at an end.

Global Equity Markets in Trump 2.0

When we are looking at the global equity markets, we use beginning of 2025 as the most useful reference point. This is because for the for the first few weeks of Trump’s second presidency, it remained unclear what would be his modus operendi and how his administration would affect amongst many other things, global risks assets. We have all since witnessed a president who feels empowered, is determined and aggressively seeks to deliver on what he perceives to be in the best interests of America. This robust line of ‘America first’ policy has led to many unprecedented actions from seizing the leader of another sovereign state in the case of Venezuela, to demanding that Greenland comes under US control to ringing the president of FIFA and demanding a player who would have missed the World Cup match between the US and Belgium due to suspension, be allowed to play.

Be careful what you wish for

What Trump’s actions brought about however with his call to FIFA was to galvanise the footballing world behind Belgium which many could have predicted as the unintended consequence of his actions. We think there is something of a metaphor here for some of the actions of this administration where publicly at least they appear to get their will by whatever means possible. In reality, countries and companies are disappointed in the US and behind closed doors are working on their own best interests and this could actually be to the disadvantage of the US in the longer term. The US is the biggest economy in the world and by far the most successful by most measures, but we feel some of the goodwill built up over many decades has diminished and only time will tell whether that can ever be truly reinstated. In the meantime, there remain lots of new opportunities for countries and companies to prosper within the new economic world which has few, if any, precedent. The US remains the key market for global assets, but the Trump 2.0 administration has somewhat inadvertently helped level the playing field. The key question now is which nations will seize the opportunities that are presenting themselves and how quickly can they execute on their ambitions?

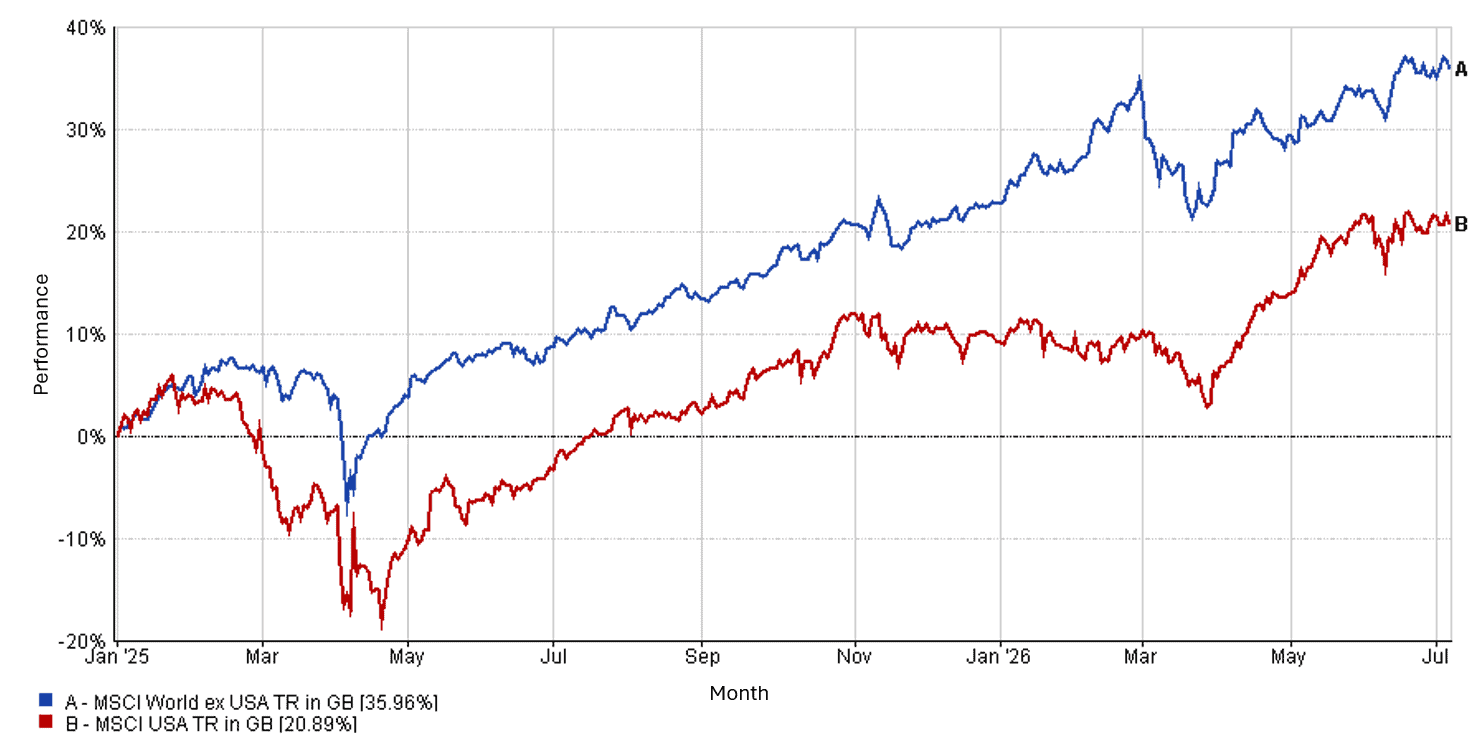

Performance Line Chart- 2025 to 07/07/2026

Source: FE fundinfo

Looking Forward

Despite an increase in global conflict, equity markets at the time of writing (09/07) have held up reasonably well. With echoes of the effect on markets from covid, the Iran conflict caused markets to fall for approximately a month. The reasons are certainly different this time, after the covid market falls governments and central banks started almost literally throwing money at their citizens, whereas this time its been a tech and AI driven rally that lifted markets. The similarity though is that once again buying the dip has proved a successful strategy. Each time this works it helps reinforce investor behaviour which suggests all dips, and for whatever reason, should be seen as opportunities to buy more stocks. Many market commentators have called the end of this as a winning strategy, but it has now prevailed for the last 18 years, since the GFC. We understand the arguments from both sides, and we remain of the belief that the best way to invest is to stay in the markets but hold a truly diversified basket of assets. That doesn’t eliminate drawdowns but it does offer a way to remain participating in the economic growth of the world economy but without putting too much emphasis on one country or sector.

Performance Update

Despite some volatility at the start of the month, June was relatively uneventful from a performance perspective, with IBOSS portfolios delivering returns ranging from -0.1% to 0.8%. More broadly, the average global equity fund delivered 0.8%, the average fixed income fund delivered 0.5%, and property outperformed them all at 2.7% for the month.

The drivers of performance varied across the different ranges. Commodities and gold faced notable headwinds during the month, which impacted the Core range more significantly due to its specific allocation to these areas. It is important to remember, however, that these same investments have previously been key contributors to performance.

Elsewhere, the portfolios’ allocation to US smaller companies contributed positively, while areas such as infrastructure, Japan and parts of the bond market also delivered positive returns. This demonstrates the benefit of diversification, with different parts of portfolios contributing at different points in the market cycle.

More broadly, one of the key themes of 2026 so far has been the changing sources of market returns. After a prolonged period where US large companies and technology stocks dominated performance, we have seen a broader range of regions, sectors and asset classes begin to contribute. Artificial intelligence remains a significant driver of markets, but the benefits have extended beyond the well-known US technology companies. Companies involved across the wider AI supply chain, including areas of Asia and emerging markets, have been some of the strongest performers. However, not all technology companies have performed equally, and even the Magnificent 7 remain down for the year, highlighting the importance of maintaining a diversified approach even within these more exciting areas.

Looking over a longer timeframe, portfolios have continued to perform well since the start of President Trump’s second term, despite the uncertainty surrounding changes in US policy and the wider global environment. The majority of IBOSS portfolios remain ahead of their respective benchmarks across the different ranges, highlighting the importance of maintaining a balanced approach rather than relying on any single market, sector or investment theme.

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.