A handful of companies have increasingly dominated the US stock market in recent years. Previously well-known as the FAANGs, they developed into what we know today as ‘The Magnificent Seven’, incorporated by — Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia, and Tesla.

At the end of 2023, the top 10 stocks in the S&P 500, the largest by market capitalisation, represented 27% of the index, nearly double the 14% share from a decade earlier. In practical terms, for every $100 invested in the index, about $27 went to just ten companies. This rate of concentration increase is the fastest since 1950. The trend has continued into 2024, with the top 10 stocks now accounting for 37% of the index as of June 24.

Despite The Magnificent Seven stocks’ remarkable performance in 2023, as we approached 2024, there seemed to be a noticeable divergence in their fundamentals, analyst opinions, and, crucially for investors, stock performances. In reality, the similarities around the Mag Seven stocks are limited, apart now from all.

Run your winners?

Momentum trading is an idiosyncratic investing style, and the dangers of getting in the way of a bullish narrative supported by a seemingly endless stream of positive newsflows are well-documented and very real. If you are in any doubt about this, just ask anybody who has tried to short Tesla over the last few years!

When you get momentum based on a positive narrative around new technology, scarcity, future demand, a perceived wide moat, insatiable demand, and future profitability extrapolated on all supporting factors staying in place for many years to come, you get a stock priced like Nvidia.

When we say like Nvidia, it’s arguable that there has never been a stock with such an utterly positive backdrop as Nvidia before. It is for this multitude of reasons, rather than any pretence to have ‘an edge’ on the future profitability of AI chip companies, that we are increasing our allocation to a fund that has been investing in the stock for many years. Rathbone Global Opportunities manager James Thompson (who is scheduled to appear as a guest on our Sector Spotligh Webinar in September) has consistently held a 4% weighting in this stock and regularly trims it back to fund other ideas for his global equity portfolio. We have held this fund in our Core MPS portfolios since 2016, and the fund has been a top decile performer for us within the IA Global sector.

The Perils of Market Timing

Whilst the case for momentum can quite rightly be made, stock prices that diverge from fundamentals and whose investment case is predicated on a super optimistic outlook for future profits bring risks very much from the future, into the here and now. It is notoriously difficult to time changes in market dynamics, and momentum is probably more challenging than most.

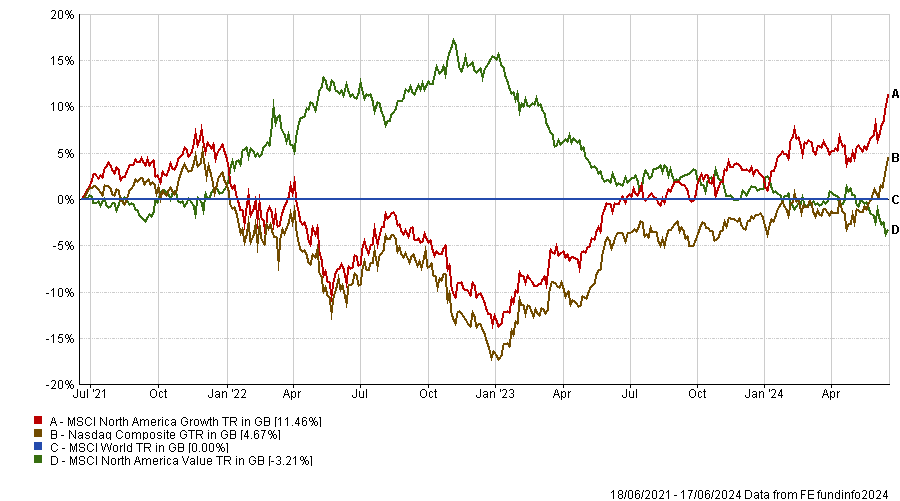

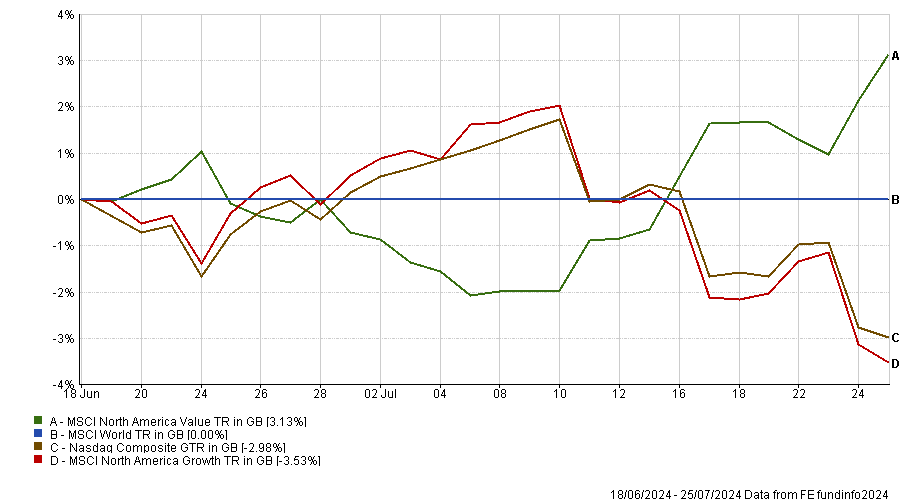

This year, in the middle of June, we saw some early signs of stock price fatigue in many growth assets, only for prices to quickly recover, and the BTD (buy the dip) approach worked again. During the back end of July (fig 2), we have seen something a little more unsettling for growth stocks, especially The Magnificent Seven, but so far, not enough to challenge the conviction of a sufficient number of investors. With the first of “The Seven” already having reported earnings, the market seems somewhat underwhelmed, but the bar remains incredibly high.

3 Year Performance Relative to MSCI World to 17/06/2024 (Fig 1)*

Performance Relative to MSCI World 17/06/2024 – 25/07/2024 (Fig 2)*

Past Performance is Not a Guide to Future Performance

For all of us within the financial services industry, we are very familiar with the risk warning that “past performance is not a guide to future performance”. So, it’s also important to consider the opposite side of the concentration risk argument.

While some view the concentration of investments in a few top-performing companies as a potential risk, others argue that these companies have robust financials that justify their market dominance. This perspective suggests that today’s market leaders are fundamentally more robust and profitable, reducing the likelihood of a scenario similar to the dot-com bubble burst.

Big US companies generally have the profits to support their lofty valuations, unlike during the peak of the late 1990s and early 2000s dot-com bubble. Present-day market leaders tend to have higher profit margins and equity returns than those in 2000. This argument has merit, but our many years of investing have taught us that when change happens, it is often for unforeseen reasons, but ex-post appears obvious.

Our Conclusion

In conclusion, the current market environment underscores the importance of diversification. While Nvidia and similar tech stocks offer significant growth potential, their volatility and concentration risk require careful management. As demonstrated by strategies like James Thompson and his Rathbones Global Opportunity fund, a diversified portfolio can help mitigate these risks and ensure more stable, long-term returns.

In conclusion, it is all about Nvidia.

Nvidia’s dominance and outsized impact on the S&P 500 are so well known now that almost everybody can spell their name. The company is the most expensive in the S&P; notably, 30% of the S&P’s returns this year have come from Nvidia alone. This heavy reliance on one company’s performance should raise concerns about the sustainability of market gains driven by a narrow segment of stocks.

The critical question is how long Nvidia can continue to drive the stock market higher or when it will trigger a downturn. The answer lies in the company’s future performance and market dynamics. While the AI sector’s growth potential remains robust, any adverse earnings reports or unforeseen challenges could significantly impact Nvidia’s stock price and, by extension, the broader market.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 152.7.24