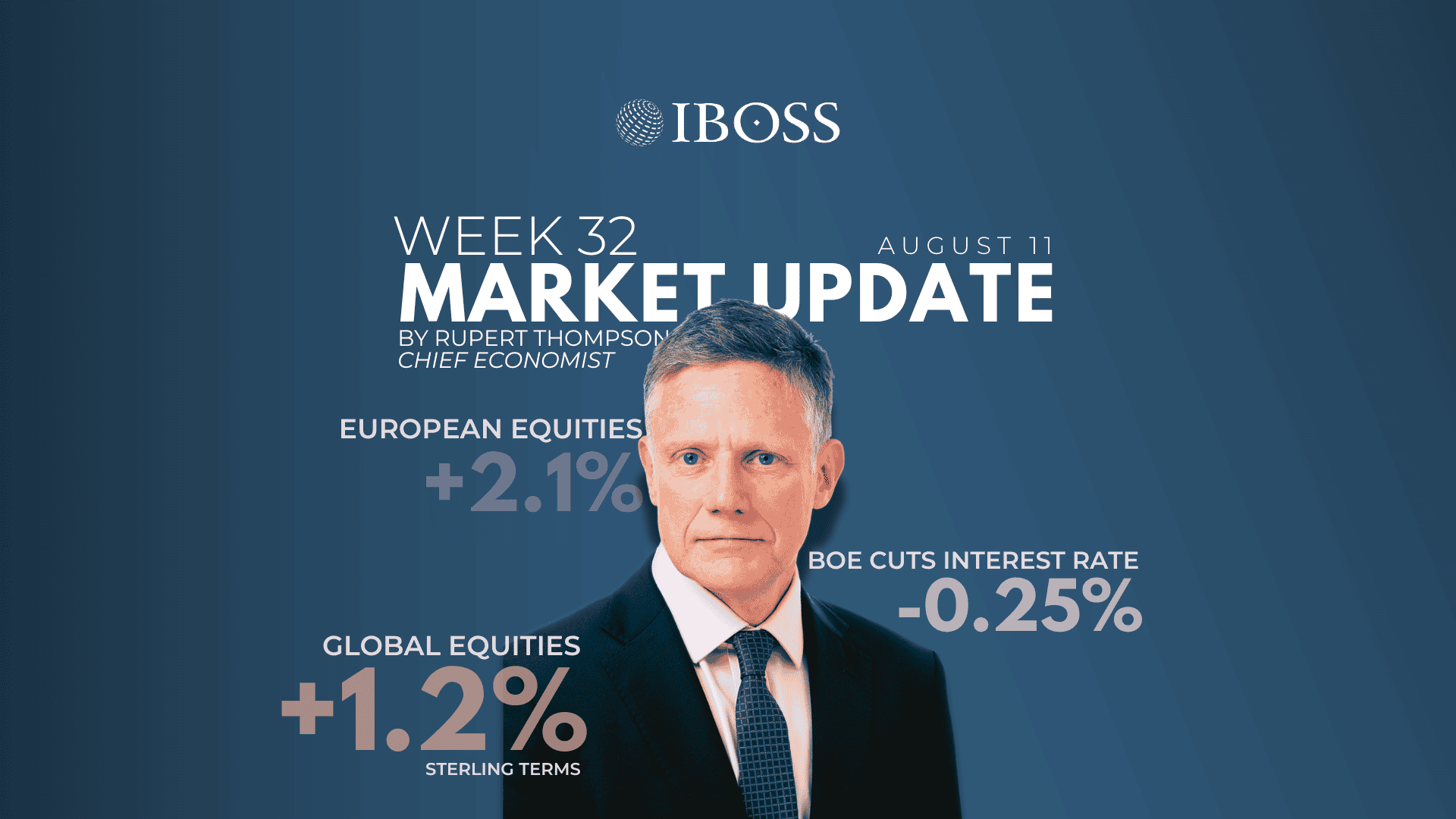

Global equities last week regained almost exactly their losses of the previous week with markets gaining 2.3% in local currency terms and 1.2% in sterling terms. Europe was the top performer with a gain of 2.1%, having been bottom of the pack the week before.

Bonds also unwound some of the previous week’s gains, as yields edged higher. Finally, the dollar turned down again, unwinding its 1.3% rise against the pound a week earlier.

The improved mood in equities came on the back of investors switching to look on the bright rather than dark side of the recent unexpectedly weak US payroll numbers. Instead of worrying about the marked slowdown in growth implied by the employment data, the focus turned to the prospect of increased rate cuts….and maybe forthcoming summer holidays.

These hopes were fanned by Trump’s latest hiring and firing decision. Whereas the sacking of the head of the statistical agency behind the displeasing payroll numbers had caused some unease, last week saw Trump appoint one of his acolytes to the Federal Reserve to replace the governor who has just resigned.

Stephen Miran will be in place until January when he will be replaced by Trump’s chosen successor to Chair Powell whose term ends in May. He will almost certainly reinforce calls within the Fed to cut rates and the market now expects rates to be lowered 0.25% in September with a further reduction by year-end.

The US earnings season has also been a background support for equities. With 90% of the S&P 500 now reported, earnings look set to post a healthy 13% gain on a year earlier, considerably more than anticipated at the start of reporting.

Tariffs were once again a source of headlines – and some confusion in the case of a potential 39% tariff on gold imports from Switzerland. Thursday saw the reciprocal tariffs announced the previous week implemented as planned in a rebuttal of the so-called TACO trade, not that this was a surprise or seemingly of any concern to the markets.

While the endpoint for US tariffs is now much clearer than it was, there are still some key points to be resolved. Most importantly, will the US-China 90-day trade truce which expires tomorrow be extended? Most likely it will be, given the positive mood music of late.

There are also still Trump’s threats to impose 200% tariffs on pharmaceuticals and also now 100% on semiconductor chips. But in both cases, the ultimate tariffs could be significantly smaller with big exemptions for companies (such as Apple) willing to promise large enough investments in the US and/or other sweeteners to appease Trump.

The mood in the UK was rather more sombre with hopes for future rate cuts being scaled back somewhat. The BOE lowered rates as expected by 0.25% to 4.0% but the decision was surprisingly close-cut with five members voting for a reduction and four for no change.

While slow growth and a weakening labour market argue for lower rates, the unexpected stickiness of inflation is driving the Bank’s increased caution. Inflation is now forecast to edge up further to a high of 4% in September, only slowly returning to its 2% target over the next two years.

The BOE continues to believe the path for rates remains downwards but is highlighting the uncertainties and that any future cuts will need to be made gradually and carefully. Although it still looks more likely than not to end up sticking to its pattern of cutting rates once a quarter with another 0.25% before year-end, the risk of a pause has clearly risen.

In an unhelpful repeat of last year, attention is also increasingly turning to the tax hikes looming in the autumn Budget. The size of the black hole now needing to be filled if Reeves is to stick to her fiscal rules was put last week as high as £41bn by one think-tank (or £51bn if she maintains her current £10bn headroom) although the more general view is that the hole will be a more moderate £20-25bn.

This coming week, Tuesday will be the main focus for markets with US inflation numbers out and the China-US trade truce expiring. But US retail sales and consumer confidence numbers on Friday will also be important given the recent slowdown in consumer spending. Here in the UK, we have the latest labour market data out on Tuesday and second quarter GDP figures on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 233.8.25