Fixed income has spent much of the past decade out of favour, quietly side lined as investors have increasingly gravitated toward equities. The pattern is not unfamiliar: markets, like cultural tastes, tend to move in cycles, and what once feels essential can quickly become overlooked or ignored all together. Vinyl records, like fixed income assets have become a reduced part of investors’ portfolios and in many cases disappeared altogether, but are they due a comeback?

Equities Become the Default Track

Investors have become increasingly indifferent to fixed income within portfolio construction as equities have become increasingly the asset class of choice.

Over the past 15 years, global equities have been the dominant driver of returns, with the MSCI World index significantly outperforming the Global Aggregate bond index by a cool 440%. As a result, portfolio allocations have shifted meaningfully in favour of equities and all the evidence suggests this has indeed been the right decision.

In 2010, a typical “balanced” portfolio held between 40-60% in equities with the remaining allocated to diversifying assets, predominantly fixed income. Today, that same balanced portfolio is far more equity-heavy, with equity allocations of between 60-80%.

From Vinyl to Streaming, the shift to Passive investing

We can see that bias toward equities by examining which funds were popular 15 years ago vs today. In 2010, investor demand was shaped heavily by the aftermath of the financial crisis. Capital flowed into funds that prioritised income, capital preservation, and active management. These were strategies designed for a world still recovering from the dot-com collapse and the 2008 financial crisis.

2010 best-sellers

- Fidelity MoneyBuilder Income (Fixed income)

- Invesco Perpetual High Income (UK Equity Income)

- First State Global Emerging Markets Leaders (EM Equities)

- M&G Optimal Income (Fixed Income)

- JPM Natural Resources (Commodities)

Fast forward to today, and the picture is materially different, and the bestseller list is dominated by passive equity strategies, as investors have followed returns into an increasingly concentrated selection of regions and stocks.

2026 best-sellers

- Vanguard FTSE Global All Cap (Global Equities)

- HSBC FTSE All-World Index (Global Equities)

- Fidelity Index World (Global Equities)

- Vanguard S&P 500 ETF (US Equities)

- L&G Global Technology Index (Global Tech Equities)

So, we know that over the last few decades investors’ appetite for funds has changed dramatically. Investors were acutely aware of the effect drawdowns can have on portfolios in the 2010’s and today investors are increasingly unconcerned with the risks facing markets.

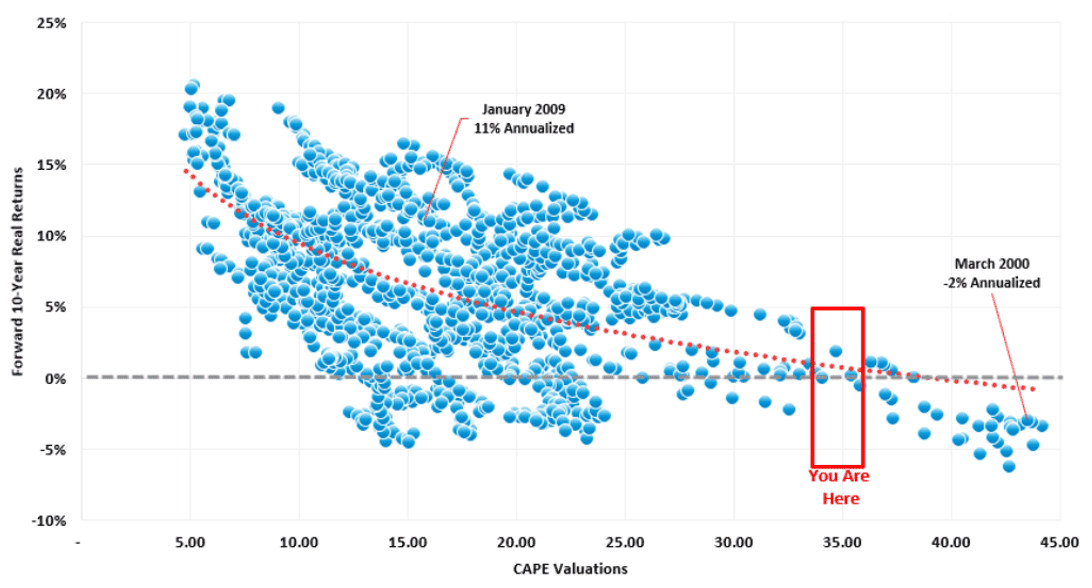

Ignoring the well-publicised concentration of global equities (Where the top 10 companies make up almost a quarter of the global equity index) the chart below shows that equity markets do look expensive on many metrics, and historically investing at these levels has meant poorer returns for investors over the next 10 years.

Forward 10-year real returns

Source: Real Investment Advice, Feb 2025

There is a huge amount of nuance here that the chart doesn’t capture, however it should perhaps lead investors to question whether they are buying equities because of the future outlook or due to recent history.

Fixed Income: The Record Left in the Attic

Many investors are still nursing the hangover from 2022. As central banks raised interest rates aggressively to combat inflation, fixed income experienced one of its worst periods in recent history. Assets traditionally viewed as lower risk, particularly government bonds, delivered losses that surprised even many seasoned investors.

Understandably, some investors packed away their fixed income vinyl and left them gathering dust in the attic. But it may now be time to dust them off.

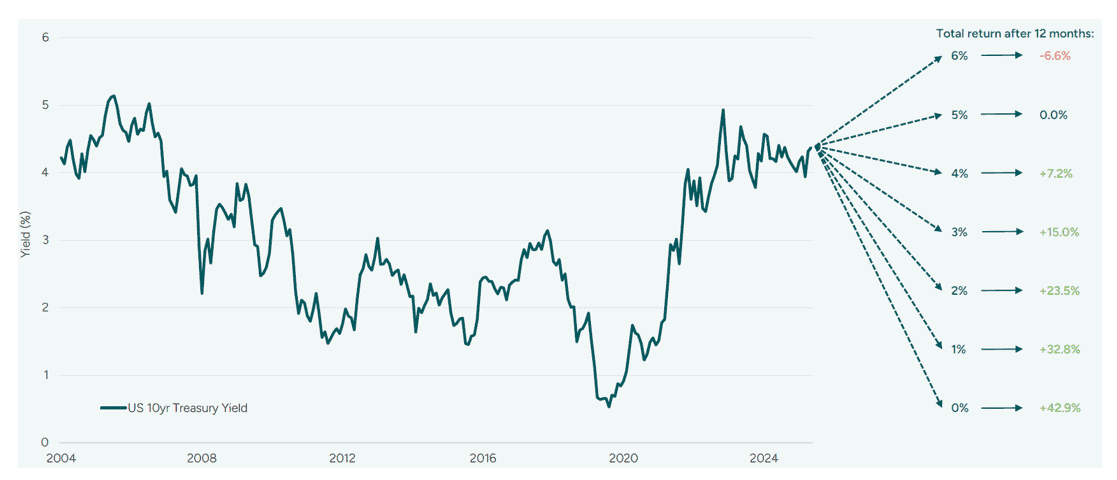

The chart below, produced by M&G, illustrates how the return profile for fixed income has fundamentally changed. Government bonds now offer yields of around 5%, which is attractive in its own right, but importantly, investors once again have meaningful scope for capital appreciation should interest rates fall, or economic conditions weaken.

This is in stark contrast to the pre-2022 environment. When policy rates hovered near zero, bond investors received very little income and had limited room for further capital gains. Today, the asymmetry looks materially more favourable for bonds.

Government Bond markets: an asymmetry in return outcomes

Source: Bloomberg, 30 April 2026.The scenarios presented are an estimate of future performance based on evidence from the past on how the value of this investment varies, and/or current market conditions and are not an exact indicator.

Of course, not all fixed income is created equally. As with equities, parts of the bond market, particularly segments of credit, look increasingly expensive. But in a market where many asset classes appear richly valued, investors may wish to make the trip back to the attic and revisit some of their old defensive favourites.

After all, whilst equity markets could continue to soar, market leadership is never permanent. Following the dot com bubble, equities underperformed fixed income for 19 years. That is a holding period even committed high risk investors might find difficult to endure. It is always difficult to invest in an asset when the data from the last few years has been so poor but it so often proves to be an opportune time to buy.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.