Putin thought his ‘Special Operation’, which was meant to invade and seize power in Ukraine, would be over in a matter of days. What he got instead was a protracted bloody war that is now in its fourth year. The reality is he has little to show for the huge toll of human misery the conflict has brought to Russians and Ukrainians alike. It’s very possible, if not almost certain, that had he fully realised the resolve of the Ukrainian people and what would transpire over the following years, the attack on Ukraine would never have begun.

We can only hypothesize, but would Donald Trump have bombed Iran had he realised that yes, the Strait of Hormuz could actually be controlled and effectively shut by the Iranian Revolutionary Guard? It’s a very different conflict to the one in Ukraine, but like the Russian war, it is once again a heavily armed global superpower, with enough nuclear arms to destroy the planet many times over, discovering that things are rather more complicated than first assumed.

This all matters first and foremost for the future of humanity, but it also matters greatly to the investment landscape. The Russian invasion of Ukraine gave us a strong indication of why countries need to control as much of their national energy supply as possible. The ongoing battle over the Strait is surely the final piece of evidence any nation could need that supply chain resilience and energy security should be among the very highest priorities of any government, regardless of where they sit on the political spectrum.

So, what’s the Plan?

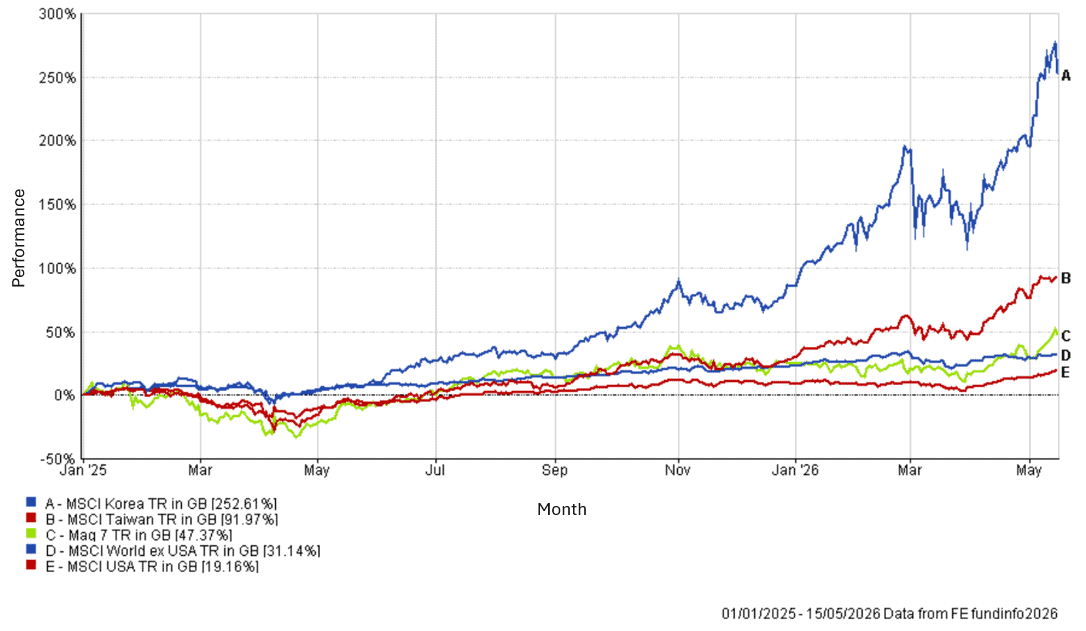

The other significant factor driving total returns in investment markets is the latest bout of AI euphoria. Net net, the positive impact of the AI related story is currently winning out, and some markets, most notably Taiwan, the US and Korea, are making new all-time highs. It may seem counterintuitive that a single factor such as AI can more than offset the impact of a potential global collapse in energy supply, but part of the reason lies in the sheer size of the stocks involved and their outsized weighting within their respective indices.

The idiosyncratic risks are clearly building in many of the AI related stocks, but simultaneously so too are the risks of not having exposure to the most exciting area of investing and the one which continues to captivate people whether they are investing in it or not. We feel it is precisely these kinds of huge sectoral and geographical divergences that highlight the benefits of regular rebalancing. This is something we do quarterly, and it means we can maintain exposure to these exciting growth companies without taking too much downside risk or leaving clients overly exposed to an area of the market which already looks expensive by many metrics. This discipline of rebalancing is something many non-advised investors fail to appreciate. After all, it is difficult to trim your winners when the CEOs of these companies are all telling you just how strong their outlook remains.

We can make both a bullish and bearish case for pretty much every asset class and geography right now. What the two conflicts in Ukraine and Iran also show us is that the future warfare is about drones and technology and that means the global conflict playbook pre the Russian invasion is largely obsolete. So, we have increasing global conflicts, with cheaper weapons and powered by AI. What this situation calls for in our opinion is an unprecedented level of humility and an acceptance of the very limited visibility on the shorter term outcomes. Longer term we believe that there are investment opportunities in all parts of the globe and in all asset classes and we need exposure to them but as we have said many times, the rear view mirror is not your friend here. The tectonic plates of the investing world are changing more than at any time since the GFC back in 2008 and old allocations just like pre-drone conflict playbooks are now obsolete, regardless of how things break from here.

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

IBOSS Performance Update

April was a more challenging month for the portfolios on a relative basis, as a concentrated selection of stocks outperformed the broader market, many of which remain closely linked to the AI story.

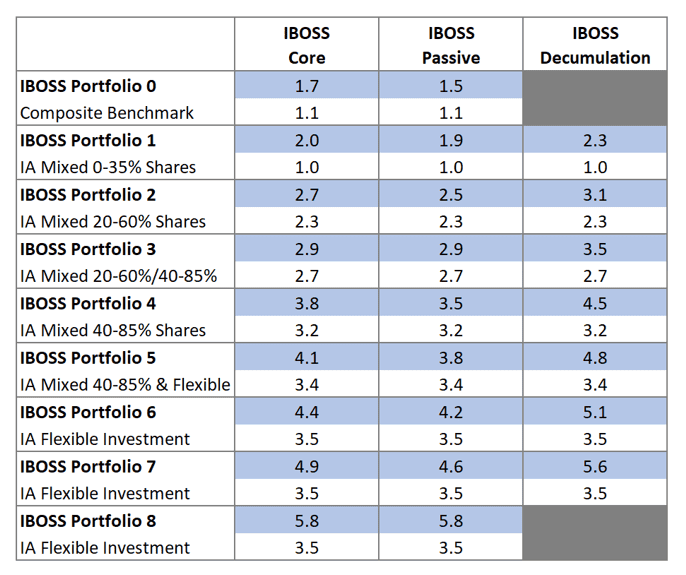

That said, all IBOSS portfolios delivered positive absolute returns for clients, ranging between 1.2% and 5.4% depending on the portfolio. It is worth noting that whilst our portfolios remain highly diversified across regions and sectors, they also retain meaningful allocations to the AI mega-cap companies, including Taiwan Semiconductor, Samsung and the US mega caps, all of which contributed positively to portfolio returns through the month.

This was reflected in the best performing sectors over the month, with Asia ex Japan (11.87%) and North America (11.50%) leading the pack. On the flip side, the weakest performing assets were largely Fixed Income related. In many cases bonds produced negative returns for investors and, at the time of writing, are now offering increasingly attractive yields relative to recent history, but in some case such as Jpan the most attractive yield for several decades. Other diversifying assets such as Property, Infrastructure and Commodities also lagged the strong rally in certain global equities though again many of these areas still produced positive returns. Looking longer term, all IBOSS portfolios have outperformed this year and across most cumulative time periods, including 1, 3 and 5 years, reflecting the reality that diversification continues to be beneficial for client returns, especially through the volatility seen since Trump took office for his second term.

Whilst certain investment markets have been relatively kind to clients, it is worth noting that the global economic backdrop continues to look uncertain and some areas of the market appear increasingly expensive. Though clients have been rewarded for staying invested, we know it might be it might be tempting to pile into certain subsectors of the market. As ever, we are looking to ensure that the portfolios remain well diversified in order to help protect against the undeniable downside risks. At the same time we are maximising the opportunity set that exists as the tectonic plates of the investing world continue their most Significant moves since the GFC back on 2008.

Year to Date Portfolio Performance (to 30/04/2026)

Source: FE FundInfo

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

149.5.26