Most income investors choose dividend stocks by looking at a company’s current dividend yield and history of payments. They base their choices on historical trends and hope the dividends will keep on coming, even when the economy takes a turn for the worse.

However, many businesses became victims to the Covid pandemic, and while it was actually a tailwind for some types of stocks, it was a disaster for others, with dividend paying stocks some of the hardest to be hit.

So, as global economies begin to recover, and because Halloween is just around the corner, we answer the question many investors want know: are dividend stocks dead or undead?

How did we get here?

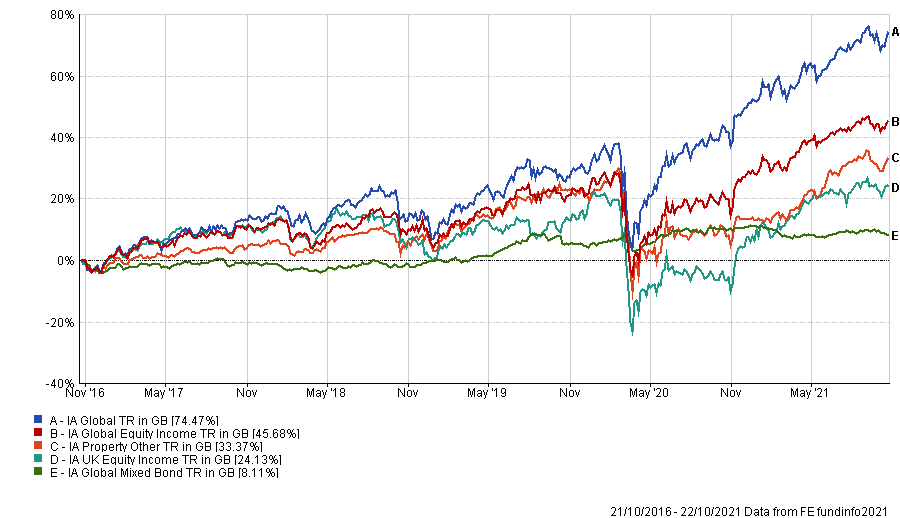

Over the last five years, the IA Global Equity Income sector has produced solid absolute returns. As ever with risk asset returns, the journey over that period has been somewhat more complicated. If you invested at the start of the five years to the 23rd October 2021, you would have realised gains of over 45%. However, if you sold out at the end of the Covid-19 sell-off in March 2020, you would have been nursing a loss of circa 5%.

Selected IA Sectors

5 Year > data to 23/10/2021

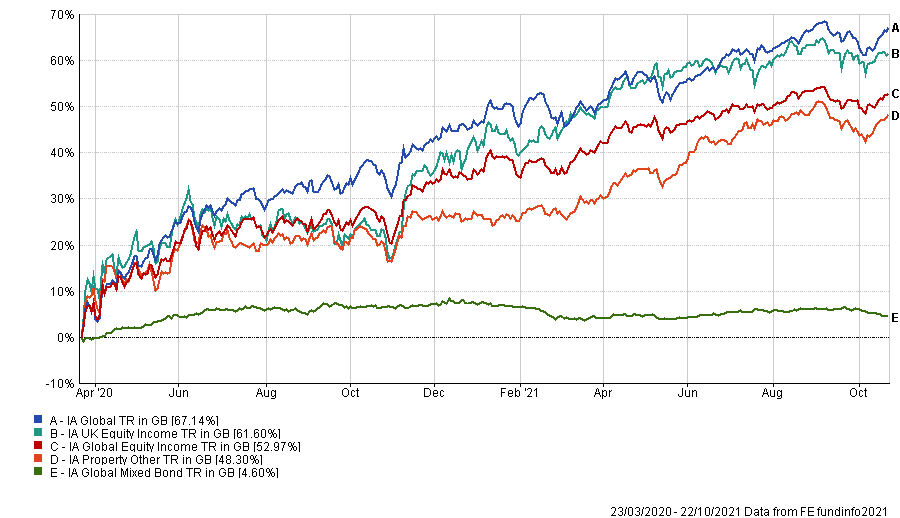

Post Covid Sell-off > 23/03/2020 – 23/10/2021

There is a perception amongst many investors that the kind of companies that make up the majority of income funds should give more protection than their more growth-orientated peers in market drawdowns. Whilst this held true for two out of the last three drawdowns, it didn’t apply in the Covid one. As global dividend policies suffered from emergency regulation and hastily reconstituted payout ratios, many companies found themselves in unchartered waters.

The Improving Backdrop for Dividend Policy

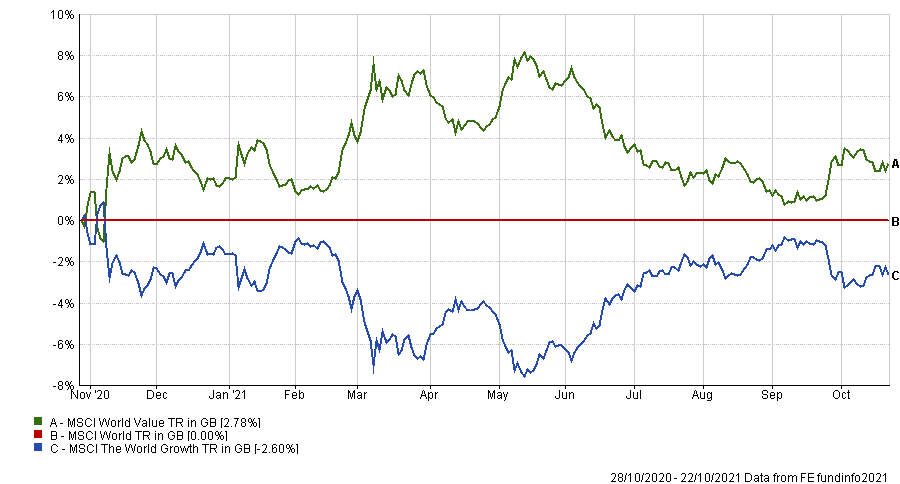

Since March 2020, the dividend backdrop has been slowly improving, albeit very much on a sector by sector basis. From October 2020, and post the first successful vaccine breakthroughs, there has been a material change in investor sentiment towards value stocks which make up a significant proportion of the global equity investable universe. While the dramatic rotation toward relatively cheap value stocks from their expensive growth stock peers stopped in May 2021, any style bias has been noticeably less discernable in recent months.

MSCI Growth Vs. Value > 28/10/2020 – 23/10/2021

The recent earnings season has brought a relatively continuous stream of positive dividend newsflow, as companies are starting to release capital hastily allocated to cash buffers designed to offset the previously unquantifiable effects of the pandemic.

Banks and the new era of higher interest rates

In a separate, but potentially almost as significant, development is the upward pressure on interest rates and the effect that this could have on banks earnings and their respective dividend policies. The hottest topics right now are inflation and the endless debate about whether it is transitory. The Fed continues to argue it is a temporary phenomenon, but rates markets, many companies and investors seem to see things somewhat differently.

Banks and financial stocks more broadly make up a significant portion of many income funds. The end of the ‘lower for longer’ era of global interest rates will bring more opportunities than they have experienced in over a decade.

Another positive factor for Global income orientated stocks, is that despite the recent removal of the aforementioned headwinds, their valuations still look attractive on a relative basis. It could, of course, be argued with some justification that very few stocks look cheap based on ratios such as P/E multiples. However, on the grounds that asset allocators find it necessary to continue investing in equities, then income stocks do look attractive.

Recency Bias

One of the prevailing headwinds for income stocks is that they have been out of favour for such a long time that it can take a while for investors to adapt to a new macro backdrop. The investment approach that has undoubtedly worked most profitable over recent years has been the ‘buy the dip’ strategy, applied whenever growth stocks sell off. This method championed by as many retail clients as institutional ones has achieved incredible success, but much of that success has been created by central banks and, in particular, the US Federal Reserve.

This period where it was primarily assumed the central banks had your back and investors could almost never lose, does appear to be coming to an end. There have already been approximately sixty rate rises globally in 2021. Many of the counties that have raised them are not seen as significant global players. This has led inevitably to interest rate policy changes going under the radar, but they can be seen as the proverbial canary in the coalmine.

The coming period which heralds inflation, an end to tapering and interest rate rises in the largest economies in the world, could potentially tip the balance for investors, finally towards income stocks. In any event, we feel that a sensible approach is a rebalancing towards dividend payers and accepting that in investment terms, the next few years will probably have little in common with the last ones.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

These are the views of the IBOSS Investment Team at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available.

IAM 335.10.21