On the 7th April we ran our third webinar since the COVID-19 outbreak and this time it was held in conjunction with Rathbones Head of Fixed Income, Bryn Jones. As not everybody subscribes to the webinar format, we thought it might be useful to highlight some of the issues discussed and some subsequent points raised by advisers.

Obviously, the overriding issue was the ongoing effects of the Coronavirus and its effect on global risk assets. Everybody is acutely aware of the human health tragedy, but we also need to consider the economic impacts of the virus and the associated lockdowns.

We started with some better news on the virus statistics from multiple European countries, including Italy, Spain, Germany and Switzerland. We also highlighted that several Asian countries including South Korea, Iran and, most notably, China appeared to be winning the new cases fight on a sustained basis; good news indeed.

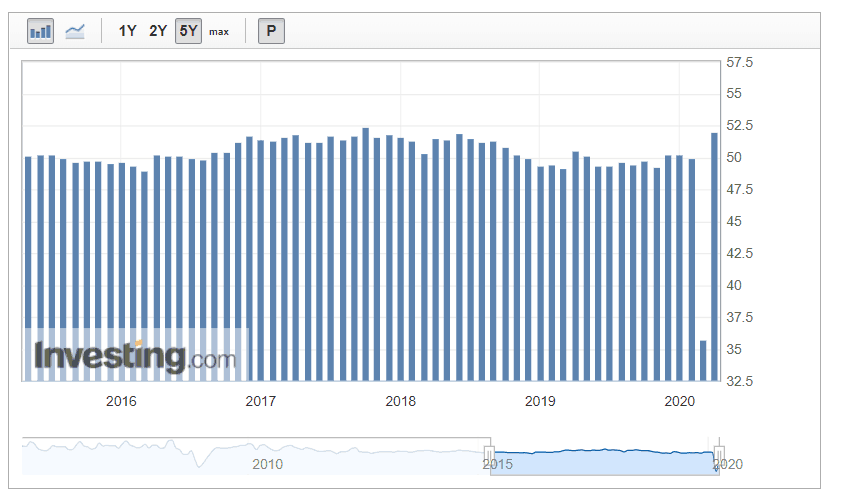

China Manufacturing Purchasing Managers Index (PMI) provides an early indication each month of economic activities in the Chinese manufacturing sector.

Chinese data

The Chinese Manufacturing data collapsed pretty much as expected in February, the big question though was would it rebound and if so to what level. Whilst accepting that Chinese data has a reputation for being unreliable, it seems to us unlikely that the results shown are not of sufficient validity to be taken seriously on both sides of the equation. A much broader, yet unanswerable question is – will this kind of sharp contraction and expansion be replicated in other countries?

The Currency Effects

We thought it important to once again highlight the part that currency is playing in the returns of different investors around the world, looking at it through the prism of a UK investor. If we take the MSCI World Index, the returns year to date (to 6th April), then the loss is -13.77% in Sterling terms but -20.22% in Dollar terms. As with the equity losses around the time of Brexit vote, the Pound’s weakness against other currencies, most notably the dollar, has helped cushion the blow for UK investors. As we always caution, this situation can and probably will reverse at some point, and many market observers have commented on Sterling’s relative cheapness against other major currencies.

Bryn Jones – Rathbone Ethical Bond Manager

Our special guest Bryn Jones walked us through his deliberations for assessing which companies will be the ones to survive the pandemic and which ones may not. Both myself and Bryn agreed on a fairly dire outlook for much of the commercial property market. Retail will come under even more pressure with the virtual enforcement of online shopping and some habits won’t revert post the virus. Added to retail’s systemic issues, we are likely to see office supply and demand dynamics come under considerable strain as both employers and employees re-evaluate the need for their current levels of square feet of office space. In time, there might well be pressure on the City and West End of London. With many companies looking to save costs, do they really need luxurious high-end space to house people who are mainly sitting at computers which they could do at home or in cheaper geographical areas?

Elevated risk

Bryn brought our attention to some areas of the bond market which have potentially oversold in the blind panic of the February/March rout. Times like this in market history are rare, with opportunities to buy risk assets at prices that only a few weeks ago seemed extremely unlikely. Our belief is that the best active managers will thrive in these conditions. Along with Bryn, we would also highlight Chris Bowie at TwentyFour and Torquail Stewart at Baillie Gifford, who are managers we hold across our investment ranges and who have demonstrated strong risk adjusted returns over many years. Due to the obvious increased risks of managing in these testing conditions, we take comfort in our multiple funds in a sector approach.

Governments and Central Bank Intervention

All governments effected by the virus continue to come up with new aid packages for their companies and citizens. There isn’t a day that goes by without a new initiative designed to offset the worst ravages of the economic effects of the virus. Although the American Democratic and Republican politicians differ vehemently about almost all aspects of government, they have managed to pass pieces of legislation and, along with their Central Bank (the Fed), they have thrown the proverbial fiscal and monetary kitchen sink(s) at the American economy, and there is more aid promised. As usual, it has proved trickier for the European countries within the EU to agree on the right fiscal course of action. At the time of writing (8th April) ministers cannot agree on the issues such as the Corona bond concept which would be mutualised debt. The countries are divided on pretty much the usual lines and in their usual camps, though it can roughly be captured as a North vs. South issue. Like most sensitive EU issues, the debate will roll on. Spain’s agriculture minister echoed words used earlier in the week by German chancellor, Merkel, when he warned the EU’s future is at risk, “this is a crucial issue on which the European Union’s future is at stake.” Regardless of any supranational fiscal progress, we can expect individual counties to do whatever they can to save their own economies. Nothing is off the table in the current economic climate.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested.

Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.