As the summer draws to a close and countless people have had European holiday plans disrupted by the government’s traffic light system, many of us are still left dreaming of that foreign beach getaway.

However, to make sure we didn’t miss out on any investment opportunities around the continent, we sent our Senior Investment Analyst, Chris Rush, on a virtual trip, looking beyond the headlines and seeking out some of the best funds Europe has to offer.

Asset Allocating to European Equities

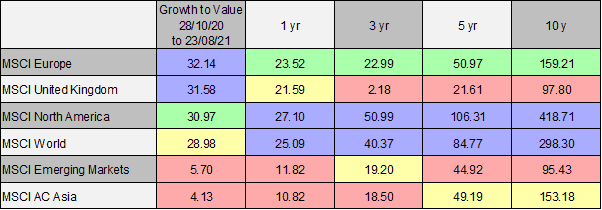

It is often quoted in investment circles that asset allocation drives 90% of returns. So it is relatively easy to see why investors have overlooked European equities for several years with this figure in mind. On the face of it, European equities, just like UK assets, have been on investors theoretical ‘red list for travel’ for much of the last decade, underperforming the MSCI World index by, a not so insignificant, 139% over the period (fig1).

Cumulative MSCI Performance to 23/08/2021 (fig1)

Quartiles key:![]()

For investors looking to generate returns through geographical asset allocation alone, the lesson, in hindsight, has been straightforward. Any allocation to a European equity Index has had a significantly negative impact on performance over almost all cumulative periods and relative to a passive global equity position.

Finding Alpha in European Equities

The headline figures do not provide the whole picture. Whilst an index position in European equities has hindered performance, it has been possible to outperform the index by selecting certain active managers.

Survivorship bias aside, the various Euro Stoxx 50 trackers and ETFs in the IA Europe Ex UK Sector have underperformed over 85% of the sector through the last decade. An indication that broad exposure to the largest companies in Europe has been a net negative to overall performance. Therefore, the opportunities of the previous decade were often outside of the most prominent names in the index, an enviable position for many active managers operating in areas where this certainly has not been the case, for example, the US and emerging market equities.

Much like the rest of the world, Europe’s best performing areas have been growth and technology stocks, which most certainly will have made it on to investors’ ‘amber watch lists’ at the very least. European growth stocks have kept up with global equities over the last five years, and European technology stocks have outperformed global equities by 66% over the same period.

Despite the oft-cited rhetoric that Europe (including the UK) lacks all things tech, it is not actually true. The MSCI Europe Index currently has an 8% weighting in technology firms. While this is far lower than some other indices, there have been plenty of tech opportunities for active managers.

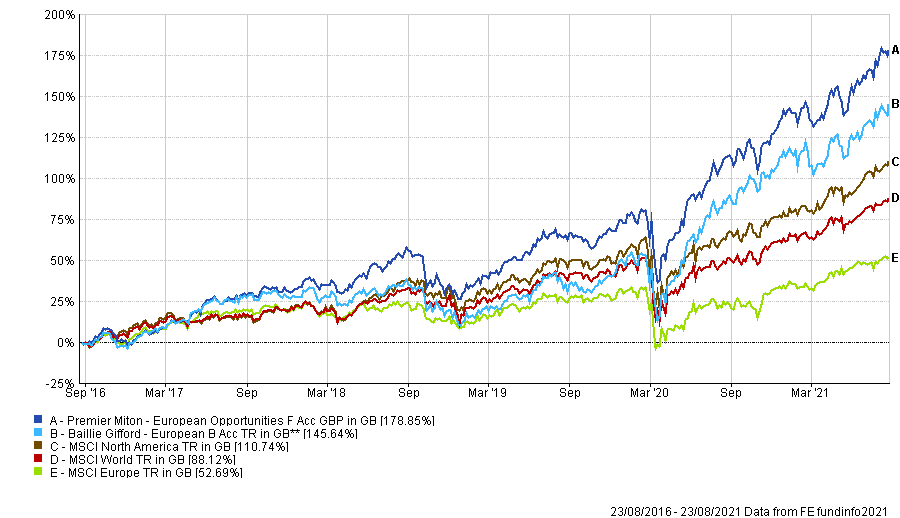

We have held two funds that benefited from these tailwinds: the Premier Miton European Opportunities and the Baillie Gifford European funds. Both have outperformed the European Index, the Global Index and even the North American Index over five years (fig 2).

Demonstrating that whilst broad index exposure to Europe has largely had a negative impact, exposure to Europe through the right active managers has had a distinctly positive effect relative to the rest of the world’s equities. Simply put, most of the alpha generated during the last decade has been sector not geographically based.

5 Year Performance to 23/08/2021 (fig 2)

Much needed diversification

Hopefully, the information here goes toward dispelling the myth that holding European equities has acted solely as a detractor to multi-asset portfolios. However, just like the traffic light travel system, the investing landscape changes, and we would urge caution when extrapolating the stellar active manager returns into the future. We are under no illusions that the strong performance of European growth/ tech is highly correlated with many of the industries that have performed well in the rest of the world.

Having benefitted from these European superstars over recent years, we have begun to shift our European holdings to take advantage of the unique make-up of the European Index. The indices significant exposures to financials, industrials and consumer-facing products have been persistently out of favour for several years, but, in our opinion, these sectors are currently on our ‘green list’ offering attractive valuations and diversification opportunities relative to other geographies.

As the expectations for inflation increase and the demand for physical/real assets rise commensurately, we suspect that many of these out of favour areas could see a resurgence of interest. We have shifted toward a more significant index weighting and incorporated managers with more flexible views on the relatively narrow growth versus value debate.

In short, if you had carried out basic sector attribution analysis, Europe presented ample opportunities for investors over the last decade. Still, we believe there will be as many opportunities in the next decade. However, we feel these opportunities could be in different sectors to the winning ones of the past. Our current European holdings are HSBC European index, Baillie Gifford European, Premier Miton European Opportunities and Janus Henderson European Focus.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information that a proposed investor may require to decide whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise, and investors may get back less than they invested. Risk factors should be taken into account and understood, including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct, but FE neither warrants, neither represents, nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 283.8.21