From Westminster to Washington: A Tale of Stability and Volatility

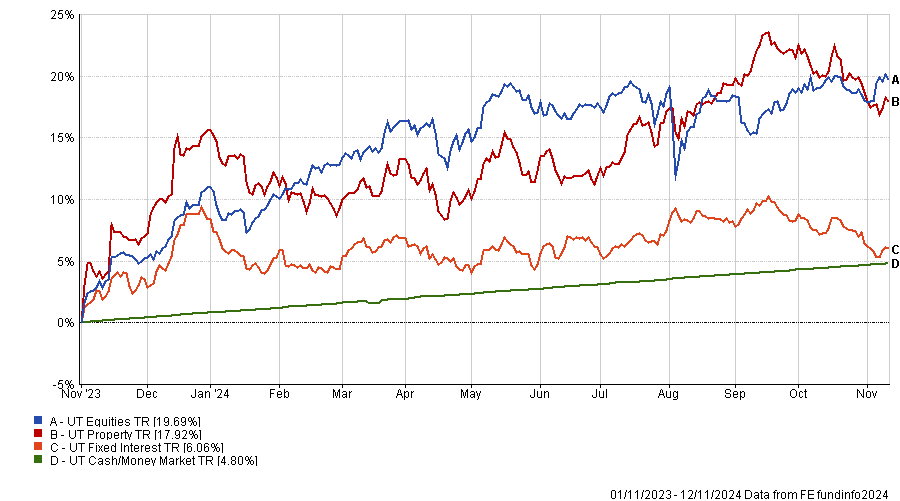

This update covers the period up to November 13th 2024. As usual, we have taken the basic asset class chart (fig.1) back to the end of October last year, the latest full Powell pivot where he signalled victory over inflation and strongly suggested rate cuts were coming, and probably quite a few of them in 2024.

Asset Class Performance- 01/11/2023-12/11/2024 (fig 1)*

Macro & Markets

Since we penned our last update four weeks ago, it’s fair to say quite a lot has happened. In the UK, October 30th saw Rachel Reeves deliver Labour’s first Budget in 14 years; we also saw the Bank of England deliver its second interest rate cut of the year, where it reduced rates by 25 basis points to 4.75%. In the US meanwhile, after a year of elections globally, the nation finally went to the polls and voted Donald Trump back in for a second term in office. More on that to follow.

The UK

So, let’s start at home. Ahead of Reeve’s Budget, and in last month’s investment update, I said that not only what Reeves said would be important, but crucially how she said it. Observers, me included, monitored key market indicators as she spoke – the pound, gilt rates and the AIM market and the initial reaction was relatively calm.

Unlike the volatility created by recent Budgets, there were no significant market spikes, which signalled an overall positive response. The pressing concern for many was whether we’d see another crisis akin to last year’s “Truss moment” and fortunately, the AIM market’s response indicated otherwise, which brought a modicum of relief.

The US

Turning to the Trump result, in the short term the market reaction to his return will likely be positive, but volatile. In the immediate aftermath we saw big rise in US small caps, while, unsurprisingly, large growth stocks also rallied. We have already seen some initial reaction in the currency markets, with the pound falling against the US dollar. However, at the same time, the pound is also appreciating against both the yen and the euro, which suggests investors are positioning themselves based on expectations of potential trade disruptions.

From a macro standpoint, there’s not a single thing Trump has said yet that won’t be inflationary. This will likely keep the dollar strong, but will impact on their ability to cut interest rates going forward, which, in theory, could put a halt to the US small cap rally.

China

One key aspect we must consider is China’s response to a Trump presidency, which remains uncertain. The stimulus package it announced in September is a pretty good indicator they thought this was going to happen, and the fact they moved the National People’s Congress to basically cover the US election allowed them to discuss things real time, with real data.

So, I think unlike Trump’s first presidency, and all the talk of Trade Wars, this time China is more prepared. However, make no mistake it will be a key theme going forward and China’s strategy will be critical in shaping global market dynamics. As with the comment above, we expect markets in China to remain volatile, but they may offer more opportunity considering the increased government impetus.

Performance and Positioning

Set against this backdrop the portfolios continued to perform well in general. Our lower risk portfolios are worth particular attention, largely thanks to the active managers we hold in the fixed income space. Within this weighting we hold emerging market debt (EMD) which has done well over the period, while we also holding a bit more in cash. Again, the message is that we remain fully diversified, hold experienced active managers, and remain shorter duration than many of our peers.

At the higher risk end of the scale, given the rally in equities, anything we have held in fixed income would have detracted from relative returns. What we have really seen in the last couple of weeks is a reversion to the previous period, namely pre-June, when investors were getting paid for being concentrated in US growth assets. The real question is whether this will be sustainable.

Within the UK, we have rebalanced our holdings to focus on selective opportunities within the market. We continue to hold a mix of funds that provide exposure both large-cap stability and mid-to-small-cap growth potential. Additionally, the portfolio has a slight bias toward value investments, which aligns well with the current market dynamics and favourable starting valuations in the UK.

Lastly, despite a recent pullback in price, we remain bullish on the case for holding gold. We have maintained a gold allocation across our portfolios for many years, typically holding around 1-2%, depending on the risk profile. Our core philosophy revolves around diversification, and we believe gold offers something fundamentally different from equities, bonds, and cash, with minimal performance correlation to these asset classes. This holds true especially during periods of heightened market volatility, as we’ve seen recently.

Outlook

Having been bullish on the UK equity market for many years, heading into last month’s Budget we did have concerns. Indeed, in last month’s market update I made the point that had it gone badly, we would have become a lot less positive on the asset class than we have been.

Instead, Reeve’s confident handling, but more importantly the market’s relatively muted reaction to the Budget delivery suggests a cautiously optimistic outlook. The UK currently presents attractive valuations, especially when compared with global markets, creating a compelling case for investors with a long-term perspective.

In the US, where we remain underweight, I do believe it would be a mistake to expect the market reactions of the next couple of weeks to play out for the rest of his presidency. As a Trump America becomes more isolationist and further dismantles the globalisation narrative, new relationships will be forged between countries and economic blocks, and it is too early to say how it will look.

Finally, despite the recent pullback in China, we know they have the power to fix things, and for that reason we remain bullish on valuations.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.