Was January 2021 even more chaotic than anyone could have anticipated?

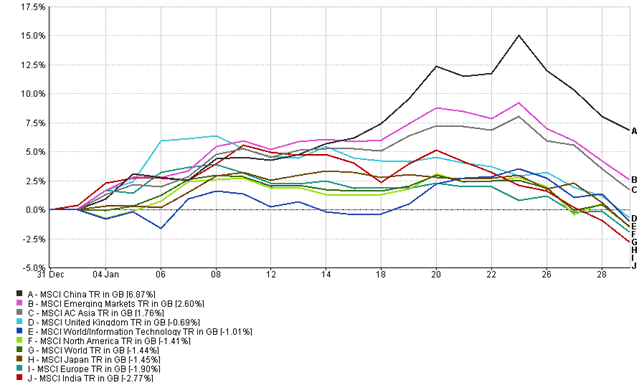

We wouldn’t usually highlight a one month chart, but we feel it is deserved in this case (fig 1).

Equity markets came strongly out the blocks lead by the UK, Asia and Emerging Markets. The UK resurgence quickly faded, but right up until the last week of the month Asia and GEM, spearheaded by China, were on course for one of their best starts to the year for some time. The last week, however, dramatically changed the return profile. The US stimulus package was once again tangled up in the weeds of partisan politics, the chaotic vaccine situation in the EU and worse than expected global economic data, combined to halt the rampaging bulls.

Then, in the last few days, a new spoiler came in; a bunch of alleged retail investors decided to go after people shorting stocks collectively. The narrative was the little guys sticking it to Wall Street, in reality, it was anything but that. On the whole ‘market makers’ did exceptionally well out of the situation and whilst some hedge funds got burned, the effect was to panic the broader equity market.

Joe Sixpack and Mom and Pop were the real losers, as the value of their pensions and savings went down. Just a guess but I doubt that’s the kind of thing which would have impressed the original Robinhood. The ‘Occupy Wall Street’ movement did little to change the pervading narrative of the rich and powerful fixing the investment game for their own ends, and so far this latest attempt has had a lot of media coverage but changed very little.

A large and growing group of people feel disenfranchised and bitter about their current economic reality, and those they see as abusing their power. Governments, central banks and the world’s financial regulators have a responsibility to address these concerns and if they don’t those who feel aggrieved will continue to seek their version of justice in any way they can. The warnings are unequivocal, but the future methods of attack and the responses of those in power are as yet unknown.

MSCI World Indices January 2021 (fig 1)

The Good News

Despite market turmoil and vaccine chaos, there is much to be positive about for the global economy.

Firstly, Israel, a virtual petridish for the pandemic’s unfolding events, has vaccinated over 35% of its population at the time of writing. As importantly, despite understandable scrutiny from some and the search for malicious gossip from others, the vaccine’s efficacy is excellent. It is an amazing piece of human ingenuity to have created the range of vaccines as quickly as has been achieved, in fact, its unprecedented.

It is also worth remembering for future bad economic situations, that usually the direst predictions are based on selecting negative factors, but with no allowance for the human response mechanism to overcome them. It is always easier to put the negative case together, becoming self-fulfilling if enough people believe it to be inevitable.

We are not out of the woods yet, but there is every reason to be more optimistic for Q2 and beyond, especially for the UK, one of the vaccine rollout leaders.

The Outlook

Whilst we have much better news on the pandemic, it has to be borne in mind that the stock market has come a long way since March 2020.

In addition, sovereign bond yields remain low, and the spread over them of most corporates is wafer-thin. The coming months can potentially offer an attractive backdrop for the best active managers and passive investment solutions where managers change the geographical equity allocation, and the duration and credit quality of the bond element.

We see one of the most significant risks as buying more of the winners from the last few years at both a country and sector level. We see opportunity in some of the value stocks that have previously been left behind, and areas such as Asia (including Japan) and the emerging markets. Again, we would highlight the UK that should now benefit from the partial resolution to the Brexit saga and its natural value orientation, as well as its vaccine rollout speed and efficiency.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 59.2.21