July was a much more positive month for markets as global equities made a stellar return of 7.72% (MSCI World), the highest monthly return since November 2020 and only the second month this year to post positive figures (the other being March). However, it was not only equities that surprised the upside, as a broad range of fixed income assets posted positive returns of circa 3.54%. In short, both bonds and equities rose together.

Perhaps the most interesting point to highlight about these returns is that the market backdrop has not fundamentally changed from prior months. Inflation remains high across a broad swathe of developed market economies, supply issues continue to impact several industries, and geopolitical tensions remain elevated.

Amongst these issues, there has been an ongoing debate about whether we are facing a global recession and, strangely, what exactly constitutes a recession. Meanwhile, the Fed, and other developed market central banks, continue their path of interest rate tightening.

Fighting the Fed & Buying the Dip

Value stocks have consistently outperformed throughout the majority of 2022, and against the backdrop of rising rates. Data up to the end of July shows that value stocks have made a positive return of 2.5% vs the tech-heavy growth index return of -10.5% in 2022.

Perhaps most peculiar about July is how this pattern has reversed. Global value stocks posted a respectable 4.4% return but paled compared to the 11.3% made by global growth stocks in July. The reversal could show that many investors are looking to buy the dip in the popular retail assets that have previously dominated headlines and outperformed in a low-rate environment. But instead, these self-same investors are now, perhaps unknowingly, buying the dip in the face of relatively straightforward central bank policy. Essentially, these investors are now fighting the fed, an approach to investing that has been remarkably unsuccessful since central banks became intrinsically linked with asset prices many years ago.

We cannot say how long this will last and what the result will be, but we would caution investors against being too exuberant considering the fundamental market backdrop. Conversely, we would also caution investors against being too pessimistic. July has demonstrated how quickly markets can turn around, and missing the best days can greatly impact client valuations. As ever, we feel that diversification is increasingly essential as the wider range of potential outcomes develops.

China & Emerging Markets

July saw far less market exuberance in China as investors seemed disappointed with the lack of action from the Chinese authorities, following the supportive comments in the middle of March of this year. Though the Chinese market fell by 10% in July, it is worth noting that they have outperformed global equities by 20% since March (15.03.2022) on the back of the announcements. Conversely, India was one of the few regions to outperform developed markets, but both India and China have proven to provide meaningful diversification benefits against developed markets (fig 1).

Regional Correlation with Global equities over 3 Years to 31.07.2022 (fig 1)*

Source: FE Fund Info

Past performance is not a reliable indicator of future performance, please refer to our important information on the back page for a full list of risk warnings.

UK Pessimism

There has been much discussion over recent weeks about the comments from Andrew Bailey, governor of the bank of England, and their pessimistic outlook on the situation facing the UK economy. We will not comment too profoundly, other than to say that much of the developed world faces many of the same headwinds as the UK. The critical difference is that our central bank has perhaps been more honest than some.

It is also worth remembering that markets and the economy rarely move hand-in-hand. As with the pandemic, markets can price in economic uncertainty much faster and ultimately recover more quickly. Considering this, we remain positive on the outlook for UK equities. Not only do UK companies still look relatively well valued against many other developed nations, but the make-up of the UK is markedly different from areas like the US. The FTSE 100, for example, has large holdings in oil/gas and financials, all of which could perform well if inflation and interest rate rises continue. After all, the UK is still the best performing developed market this year.

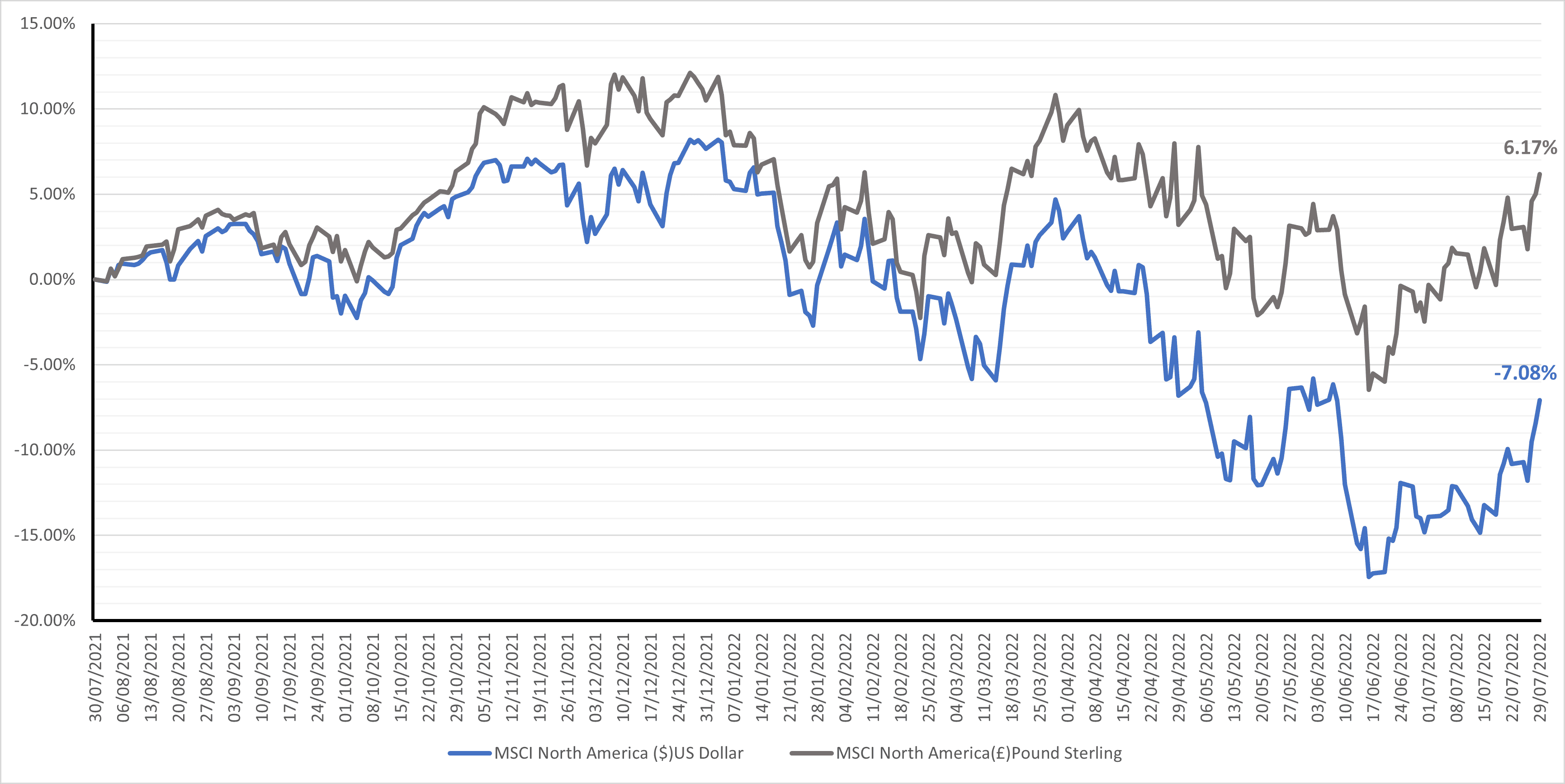

Finally, it is worth mentioning currency and the place of sterling in an investor’s portfolio. Over recent years, the dollar has strengthened significantly against a basket of other global currencies and has been highly beneficial to UK investors investing in, the US, for example. However, there is a benefit to holding a variety of currencies within a portfolio, and having sterling-denominated assets will help soften the blow if the dollar was to face a period of weakness. The chart below (fig 2) demonstrates how poorly US equities would have performed over the last year without the tailwind of a weakening pound, with currency moves equating to a circa 13% difference in returns.

US Equities 1 Year to 31.07.2022 (fig 2)*

Source: FE Fund Info

*Some information displayed may be short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years. Past performance is not a reliable indicator of future performance, please refer to our important information for a full list of risk warnings.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 206.8.22