Independence, Teamwork or Interference?

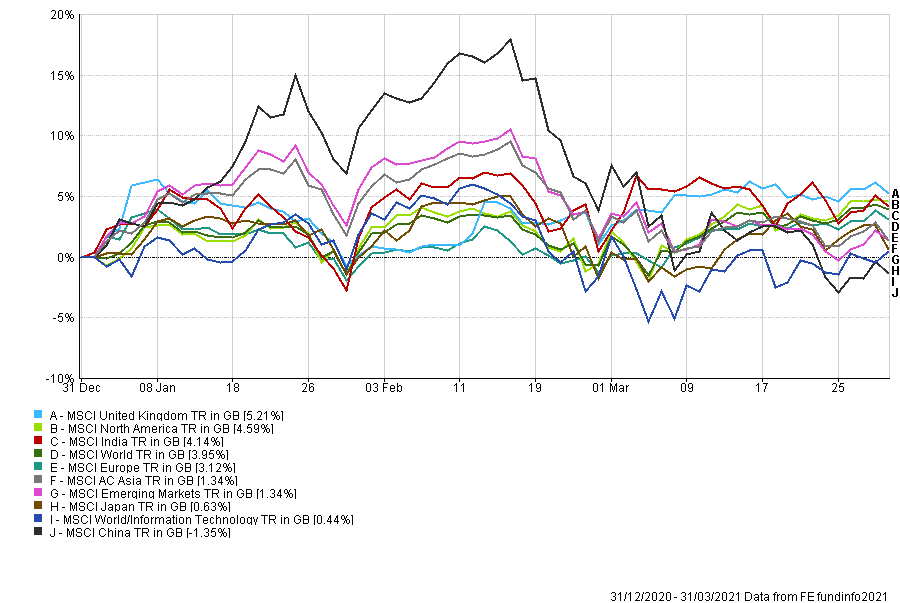

Unlike in January and February most equity markets held on to their gains in March, giving positive returns for Q1 2021, except China, which lost circa 5% and has produced a negative return for 2021 (fig 1). The Chinese government has seemed to be less accommodative to financial markets and has begun reigning in some of its largest tech firms.

MSCI Equity Markets – Quarter 1 2021 (fig 1)*

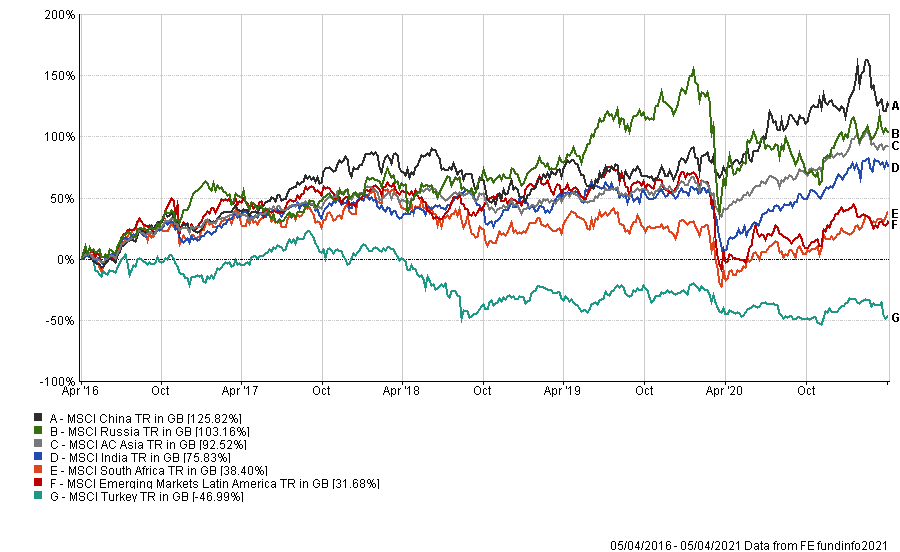

However, one country that managed to score a spectacular own goal and wipe over 15% of its stock market value at a stroke was Turkey.

In our opinion, most of whatever global central bank independence there was from governments largely disappeared after the GFC. This autonomy was further depleted during the collective panic brought on by Covid-19. This caused governments and central bankers to work together in a more direct way as they began to explicitly reference the need for teamwork.

In Turkey’s case, the firing of another central bank governor by the President brought into question the case for investing in Turkish assets domestically and by international investors. The most significant factor in the Turkish debacle is the loss of confidence in Turkish economic and currency policy, and here there are lessons for all countries. The global equity rally, fuelled by the investor perception that central banks have investors backs, could be de-railed if enough people think this is no longer the case, and in Turkey, it is not (fig 2).

MSCI Emerging Markets – 5 Year Data to 5th April 2021 (fig 2)

The UK – Finally in the sweet spot?

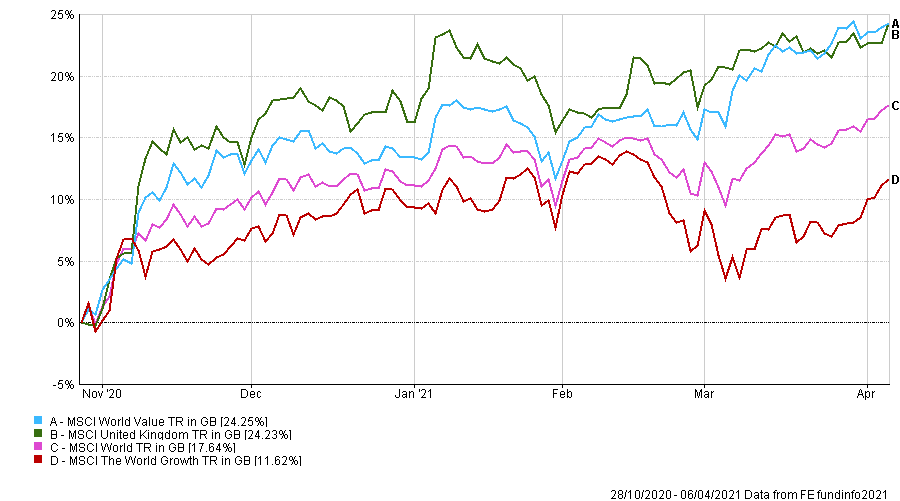

Quarter 1 of 2021 saw an extension of market trends which started to develop at the end of October 2020. Whilst we believe the growth and value labels are far too simplistic to be of much worth in selecting funds, it would be fair to say that the style indices can indicate broader market movements.

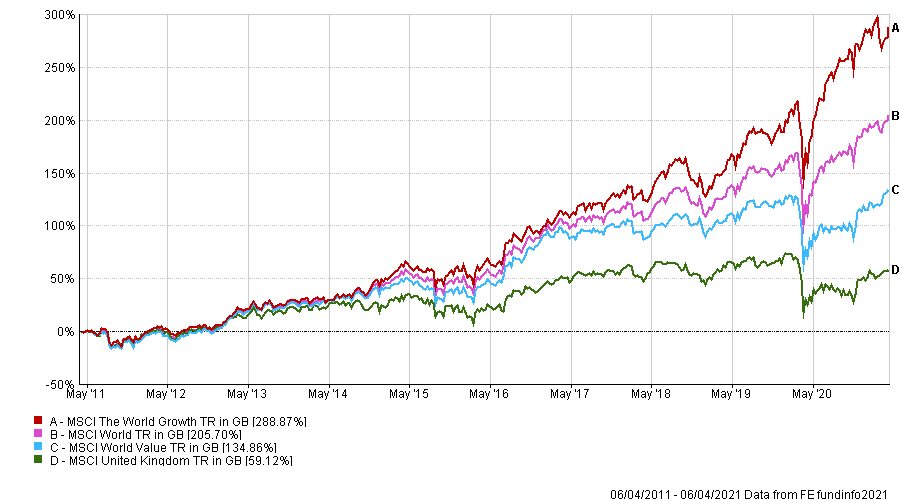

MSCI Growth Vs. Value 28th October 2020 to 6th April 2021 (fig 3)

It is widely cited that the UK’s largest stocks are a proxy for the value trade and this continues to be borne out in the data (fig 3). On top of being considered a value play (as is much of Europe), the UK has benefitted from some Brexit clarification and the stunning roll out of its vaccination programme. This rollout sits in stark contrast to the government’s chaotically inept response during the first few months of the global pandemic. We remain the most bullish on the UK in a decade, and whilst there has been some degree of catch up, the UK remains one of the worst-performing geographies over the last ten years (fig 4).

MSCI Growth Vs. Value 10 Year Data to 6th April 2021 (fig 4)

The Fixed Income Market – the return-free risk?

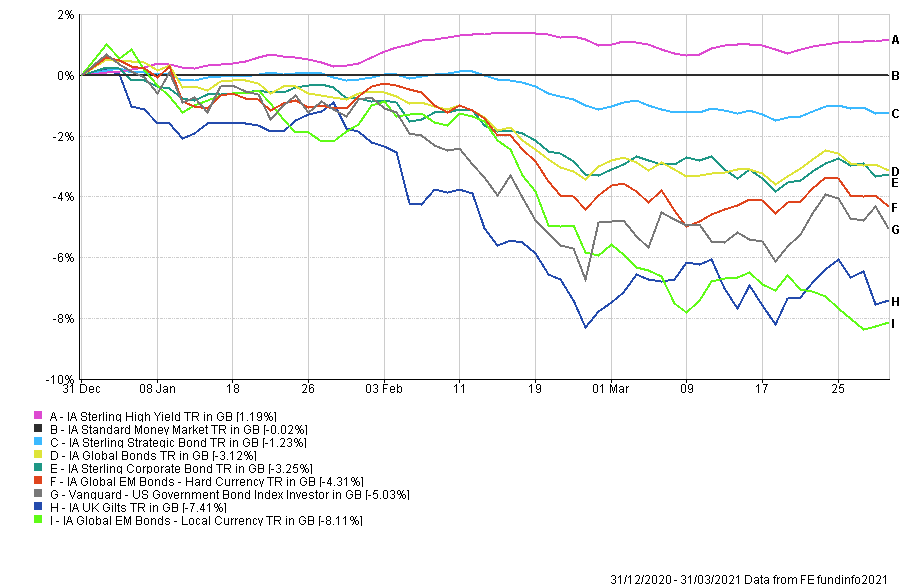

Within fixed income for the whole of Q1 the ideal assets were either high yielding or short duration bonds. The worst performing assets continue to be sovereign bonds, especially the US (-5%) and the UK (-7.5), and local currency emerging market bonds (-8%) (fig 5).

The reality was virtually all fixed income assets lost money, and even the small gain of 1% for high yield was, in our opinion, paltry given the additional risks. In the US, the spread of high yield (junk) over treasuries is the lowest for over a decade.

Although much maligned as an asset class, we continue to expect money market funds to outperform almost if not all fixed income sectors in 2021. In each of our last several reviews, we have shortened our bond duration (sensitivity to interest rates) as we expect governments globally to throw unprecedented amounts of cash at what we hope to be essentially a post-pandemic world by Q3 this year.

Fixed Income Quarter 1 2021 (fig 5)*

Rebuilding the world with free Money

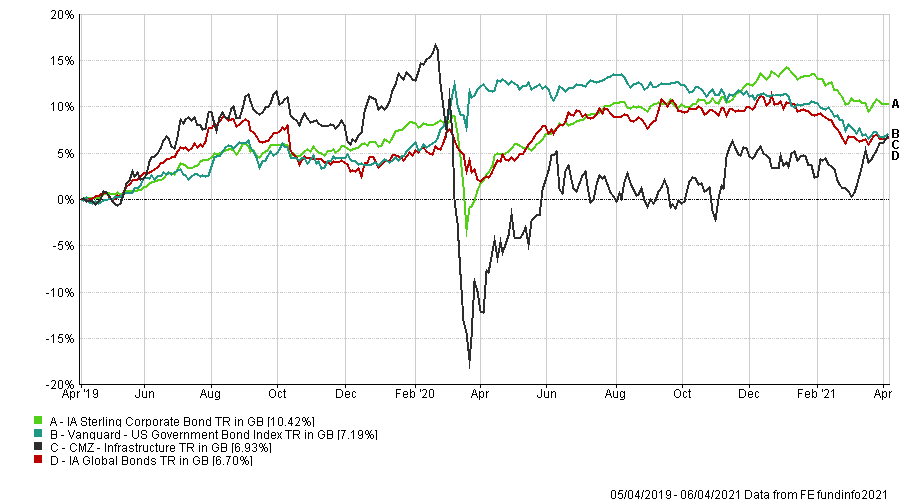

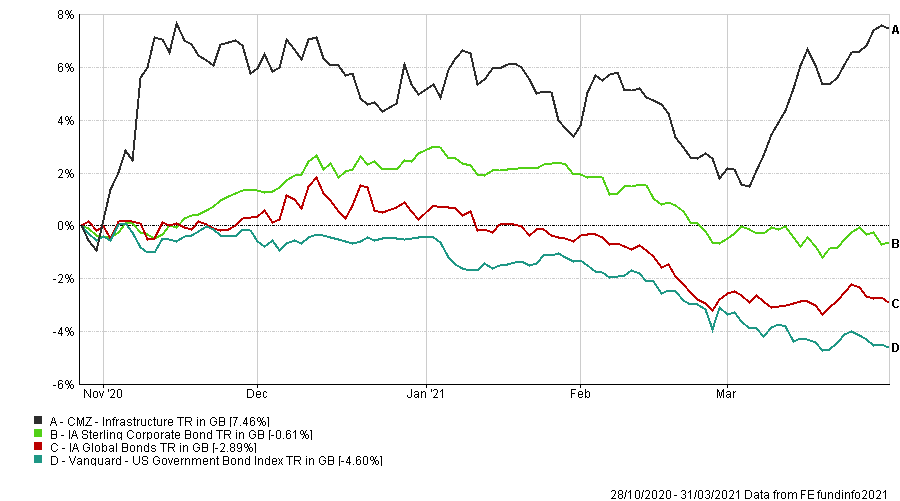

The vaccine had already boosted investor hopes of new infrastructure spending, but the arrival of the Biden presidency added fuel to the fire. As if that was not enough good news for the asset class, Biden hired Janet Yellen as US Treasury Secretary. Of course, it is not just the US that promises to throw money around like confetti, but they are certainly one of the countries best placed to carry out such fiscal largesse.

The latest US government promise is for another $3 trillion, which comes on the back of the $1.9 trillion Covid-19 recovery fund. Even with the most generous definition of ‘infrastructure’, some of the new proposals seem outside of the realms of what most people would deem infrastructure, but the fact remains there will be a lot of money looking for a home. (In the charts, the item labelled CMZ Infrastructure is twelve of the largest or best-known funds in this loosely defined area) (fig 6).

Infrastructure 2 Year Data & 28th October 2020 to 31st March 2021 (fig 6)*

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 134.4.21