The Value Trend Continues

The central narrative didn’t differ much in May from the rest of 2021, as the longstanding tailwinds supporting global growth and technology stocks continue to lessen.

A substantial component of some of the world’s largest companies’ eye-watering valuations is predicated on unprecedented low-interest rates provided by the world’s central banks. With inflation fears rising, it seems these low or zero interest rates might not be forever after all.

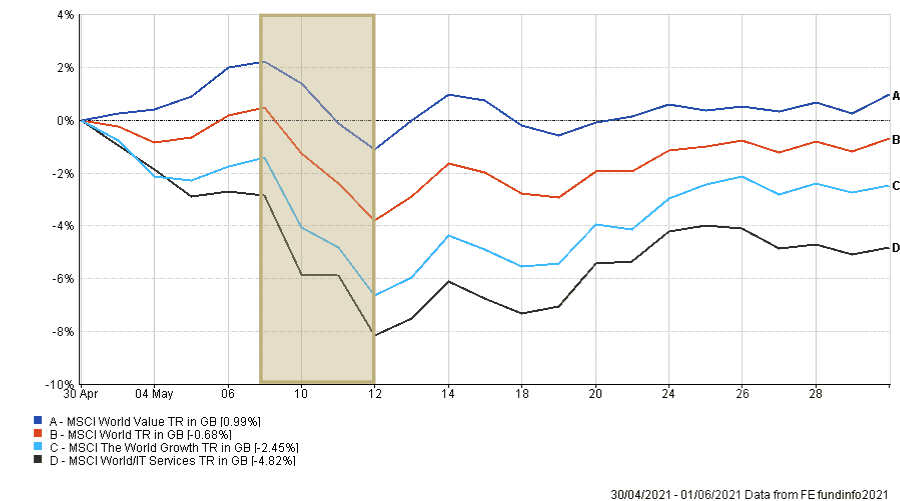

In the chart (fig.1), you can see that when equity markets briefly sold off in the second week of May, that value was a more resilient style. One always needs to be careful extrapolating from short periods of time, but it would seem to reflect where many market participants feel the risks currently reside.

Our view is that if this interest rate policy and pandemic home working enforcement are both coming to an end, the stocks that have benefitted from these two extraordinary pillars of support are now the most vulnerable ones. Conversely, we expect further support for pretty much all the previously unloved sectors such as big oil, banks and mining companies. We have in the past discussed the coming clash with the prevailing ESG agenda; well, the conflict has begun for all intents and purposes, and we have to see how the economic realities play out.

MSCI Growth Vs. Value – 30th April – 1st June 2021 (fig.1)*

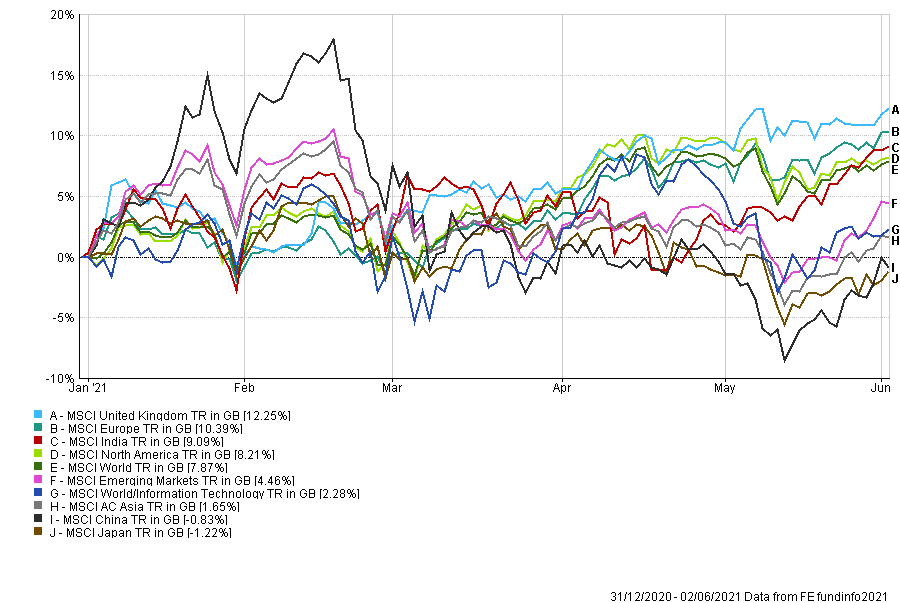

And the Surprise Winner for May… India

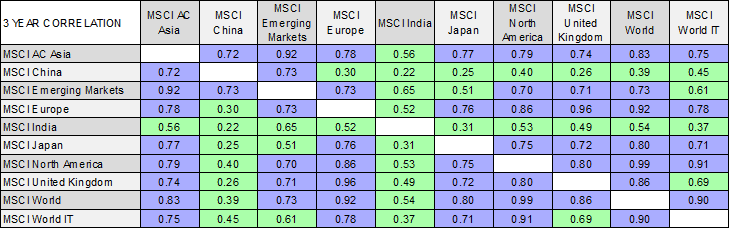

Not surprisingly, the growth-heavy US markets have continued to underperform their more value-orientated developed peers, such as the UK and Europe. However, two countries are considerably less correlated with the rest of the largest global equity markets. Those are India and China (fig.2), which makes them popular with many asset allocators, including ourselves, as the search for non-correlated assets intensifies.

3 Year Correlation of the Worlds Largest Equity Markets (fig.2)*

MSCI Global indices > Year to Date to 2nd June (fig.3)*

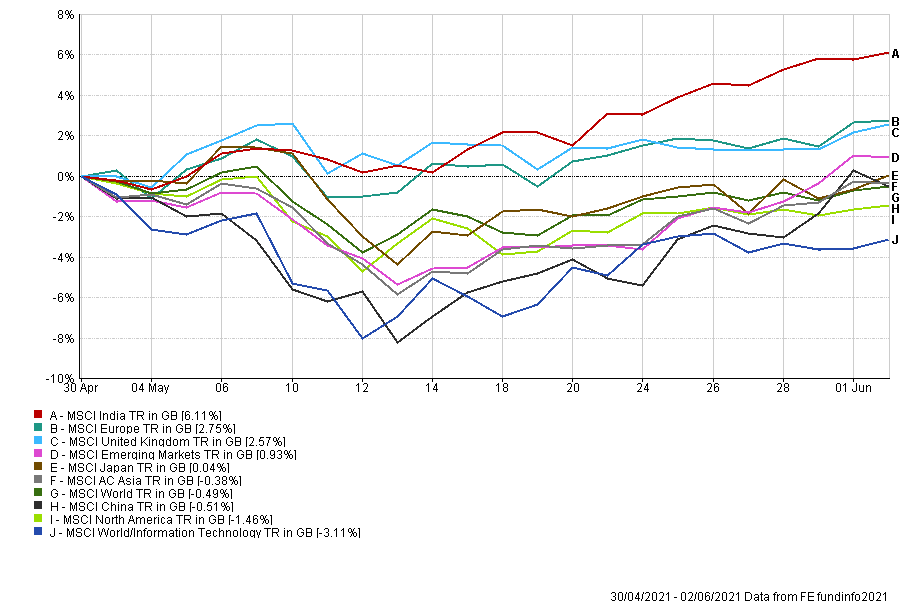

MSCI Global indices > 1st May to 2nd June (fig.4)*

Indian equity markets continue to surge, led by unprecedented levels of fiscal and monetary support, coupled with substantial foreign investment and an ever-increasing retail demand for stocks (fig.4).

While the mainstream media, both inside and outside of the country, have quite rightly been following the unfolding and heartbreaking Covid situation over recent months, markets remain mainly immune to human suffering. In some cases, and this is particularly disconcerting on a human level, they often prosper in times of the most extraordinary hardship.

The Post Pandemic Global Economic Rebound?

From an economic standpoint, the US and UK continue to lead the economic rebound due to their successful ongoing vaccination programmes. After many false starts and much finger-pointing, many countries in the EU have also now ramped up their vaccination efforts.

Unfortunately, many countries, especially in Australasia, which might have thought they had avoided at least the worst of the economic repercussions of Covid, are now experiencing new lockdowns.

There remains a stubborn reluctance to be vaccinated in France, with 33% of the population still not wanting a vaccination. That decision, if left unchanged, will potentially cause more problems further down the line and in more countries than France alone. To put that in context, according to data from the beginning of April, the figure of those not willing to be vaccinated in the UK is only 12%. The UK already has circa 60% of its population having received at least one dose, and 40% have already received a second.

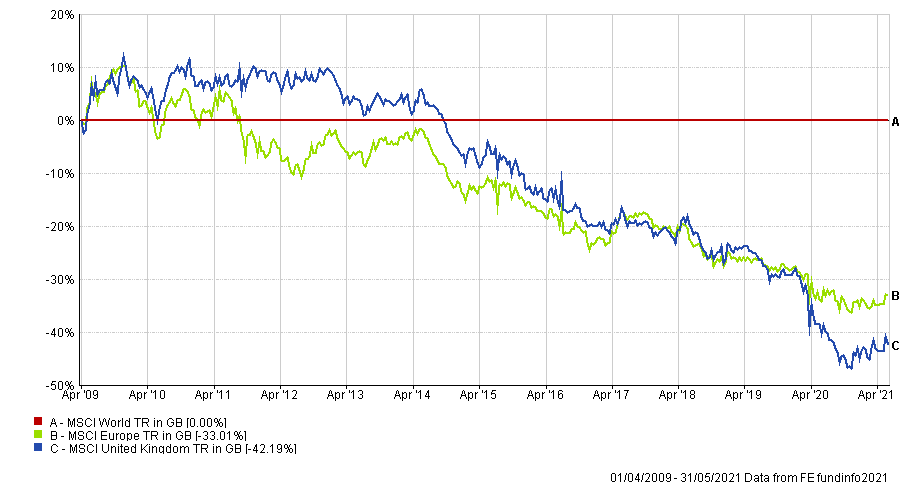

On a historical basis, it is worth remembering the considerable length of time that the UK and Europe have been left behind in performance terms by every market, except Japan, ever since the market recovery post the global financial crisis (GFC) (fig.5).

The Tricky Part

It will come as a surprise to some, but the UK has the fastest growing economy in the G7 and it is expected that it will continue to lead the way into 2022 and beyond.

The positive re-opening economic backdrop, coupled with the UK’s weighting to the kind of stocks we expect to see flourish in the coming months, is why we remain particularly bullish in our home market. This stance should not be confused with a home bias, as it is based on the evidence of the UK’s value/commodity weighted markets, the relative valuations and the vaccine roll-out.

Other countries have some of these positive factors, but no others have all three, and the relative valuation point is probably the most important of all.

Whilst the Brexit mudslinging continues in both the social and mainstream media, the reality is that the UK is once again an attractive market to invest in for both domestic and, increasingly, international investors.

As the many pages in behavioural finance written on the subject of ‘anchoring’ can testify, it is notoriously tricky to invest in previously poor performing markets such as the UK. It will be equally problematic, no doubt, for some investors to contemplate that US tech stocks are not the answer to every market requirement.

Let’s suppose US tech, and tech more broadly, outperform in market conditions that are diametrically opposed to the last ten years. In that case, everybody might be forced to accept that diversification away from them is unnecessary and expensive, and we utter the famous words ‘this time is different.’

MSCI Europe & UK vs MSCI World Since the Global Financial Crisis (GFC) (fig.5)

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 199.6.21