Despite news from the ONS last week that the UK economy fell 2.9% in January, following growth of 2.1% in December, we remain confident about UK equities’ prospects in 2021.

Headlines of economic decline always grab attention, with two consecutive drops technically signalling a recession.

But as lockdown measures hit, the 2.9% drop was better than the 4.9% decline economists had feared. The recent roadmap towards a re-opening of the economy provides investors with confidence that the UK can avoid another recession.

Economists at Deutsche Bank recently estimated that, once lockdown eases, higher-earning Brits will help boost UK GDP this year by spending a tenth of the nation’s £160bn pot of excess savings that were built up over the pandemic.

To adequately explain our reasons for backing Britain, we need to take a quick look at what has worked for investors over the past ten years and why we think change is in the air for good old blighty now that Brexit and the peak of the pandemic appear to have passed.

Momentum plays of the past decade

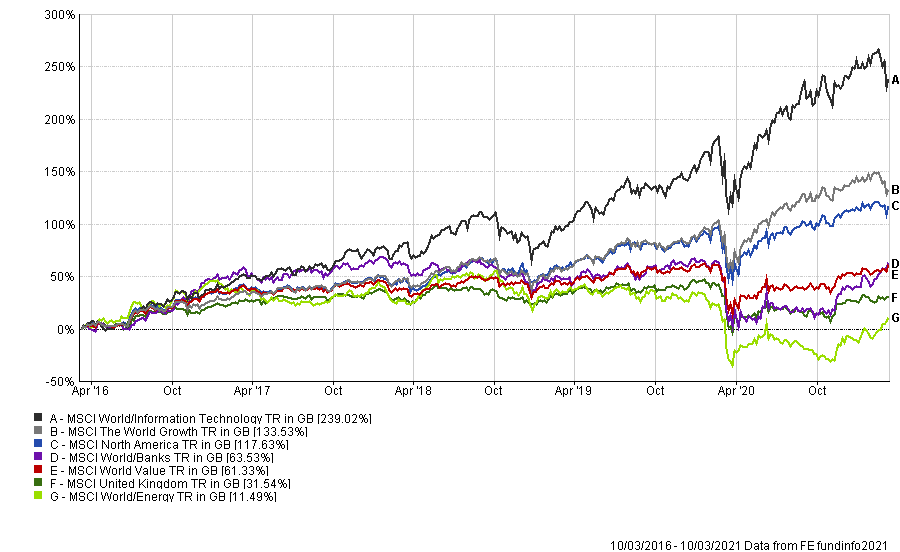

If we ignore stock specifics for most of the past five years, the most successful investment style was growth (fig 1). Generally speaking, and there are exceptions, but the last decade has consistently rewarded investors in both absolute and relative terms for investing in:

– US or dollar-denominated Assets

– Growth stocks

– Technology stocks

We identify these as the actual momentum plays of the last decade.

Growth V’s Value 5 years to 10/03/2021 (fig 1)

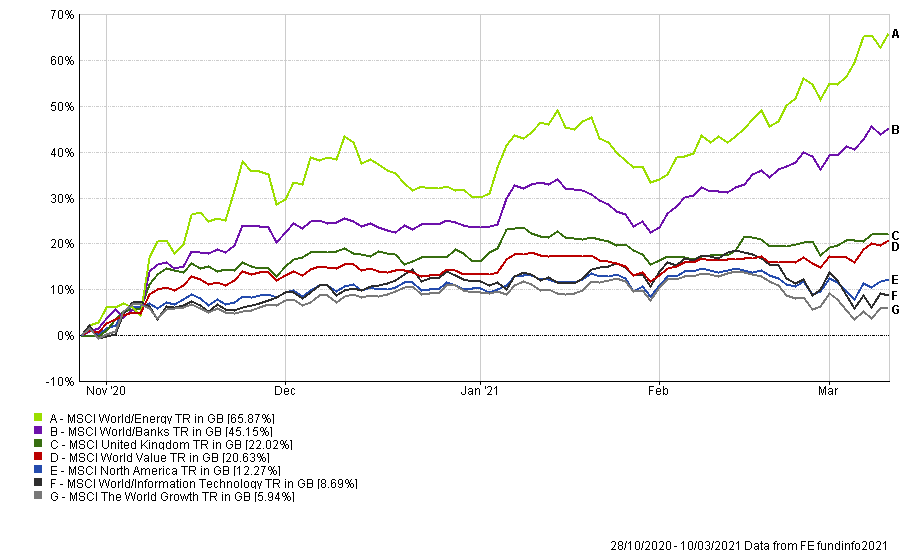

Growth V’s Value 28/10/2020 to 10/03/2021 (fig 2)

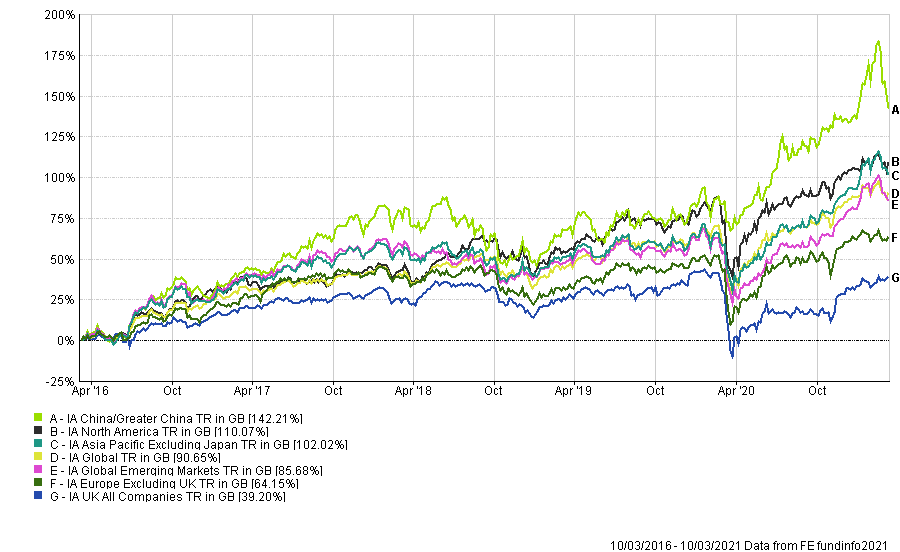

One asset that ticks all of these boxes is US equities (fig 3). Tech companies dominate the US Index, and many of the best performing funds have had concentrated positions in an ever-narrowing selection of these now costly stocks. To put this in perspective, 21% of the US index comprises of only six firms (Apple, Microsoft, Amazon, Facebook, Alphabet, Tesla). The pandemic catapulted these tech stocks into the stratosphere as many were seen to be direct beneficiaries of the increasing working from home culture.

Our concern remains that if we get a change in market circumstances, such as a weakening dollar, inflation, increased tech regulation, or a return to pre-COVID freedoms, these particular assets could significantly underperform.

We understand it’s tempting to extrapolate from US equities’ past performance and expect ongoing outperformance, but we do not expect this to be the case. We would caution that many of these US positions are highly-priced relative to history. According to the CAPE ratio (a measure to assess how expensive a market is comparable to historic valuation), US markets are the second most expensive they have been on record. We would suggest, at the very least, this should give cause for concern about future growth from here.

Global Equity Performance 5 years to 10/03/2021 (fig 3)

A new chapter

We have seen evidence of this more recently, as the investing world changed at the end of October 2020 (fig 2), and the changes are beginning to increasingly look like a new investing era.

This new chapter is not about the US versus other geographies or even a simple investing style change from growth to value. Global energy and financial stocks, especially the banks, are currently having a significant period of success. This is all about the post-pandemic global economy, which is likely to be led by the US and Asia.

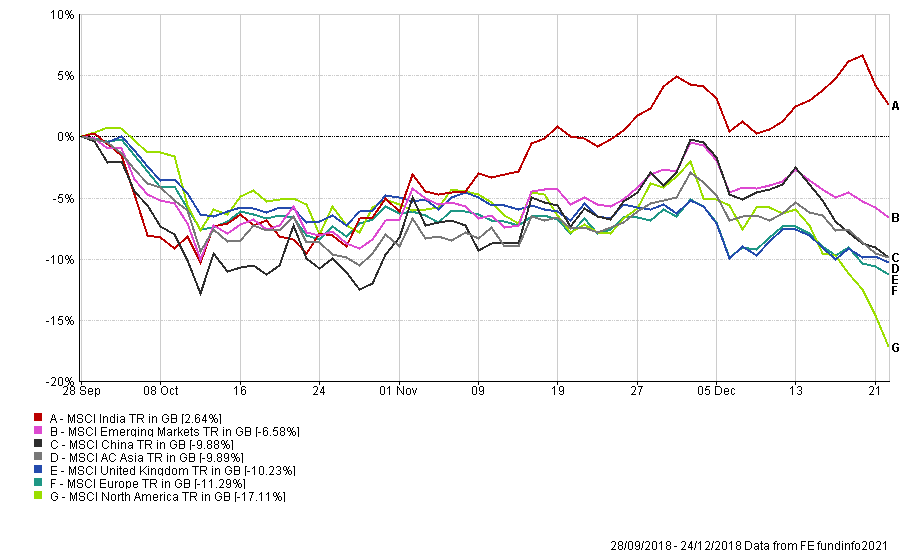

The US has just passed a $1.9 trillion stimulus package with the promise of a further $2-3 trillion infrastructure package to come on top of that. We believe this will be inflationary and potentially set up a clash between those worried about inflation and the Federal Reserve. The chart below (fig 4) shows what happened the last time the US tried to ‘normalise’ interest rates.

The Now infamous ‘Powell Pivot’ – 28/09/2018 to 24/12/2018 (fig 4)

The Powell Pivot related to the final quarter of 2018 when the Federal Reserve Chair, Jerome Powell, had told the markets there would be a normalisation of interest rates and balance sheet roll-off. The US equity market led global equities into a tailspin, with its tech stocks falling even more dramatically.

The markets, and then President Trump, tested Powell’s resolve and he capitulated in the final few days of December. After several market calming speeches by Powell and other Fed members, the long-enduring narrative of ‘the Fed has got your back’ quickly returned. 2019 went on to be an exceptionally strong year for global equities led by the US and in particular tech stocks; basically, 2019 was Q4 2018 in reverse.

An emerging market?

In 2016 the UK was the second most highly rated market in the world, today it is the second-lowest, trading at a 27% discount to the rest of the world, with only Latin America being cheaper.

The UK has suffered in recent years from its lack of technology stocks and a proliferation of ‘sin stocks in the form of oil, gas and tobacco. The large-cap UK equity market has a relative overweight to bank stocks which had been a further headwind, but over the last six months the banking index is up over 50%. These are a couple of reasons why the UK has been trading like an emerging market, but we now believe this makes the UK uniquely positioned to benefit from the re-opening of the economy.

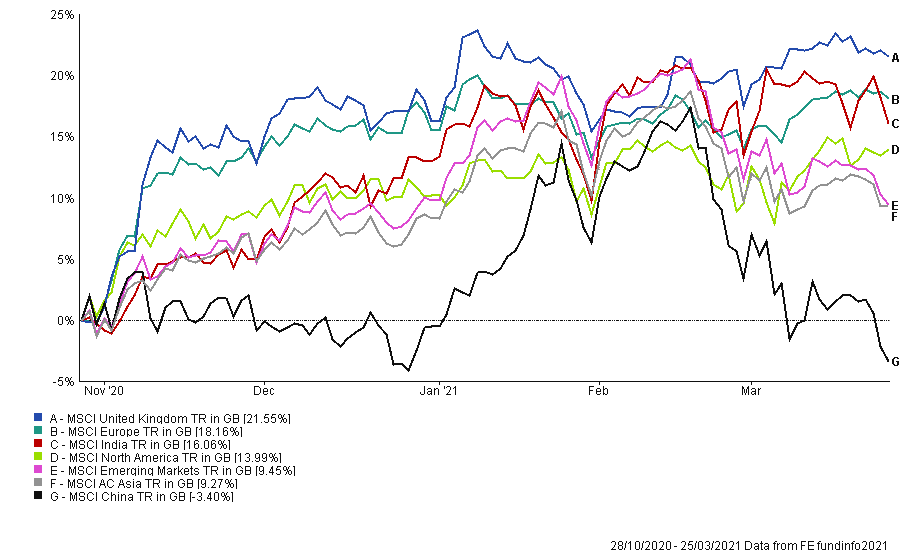

UK equities have outperformed other developed markets since October 2020 (fig 5); despite this prosperous period, we believe many UK equities still look to offer good value from here, and the UK discount from an asset allocation perspective should continue to shrink.

Global Equity Performance – 28/10/2021 to 10/03/2021 (fig 5)

Rule, Britannia!

We increased our allocation to UK equities in May 2020. One year on, we are looking to expand our UK holdings even further in May 2021, as we increase our beta to the UK equity sector and tilt towards more active managers.

The UK has just emerged from the uncertainties over Brexit, and while there will be enduring disagreements with the EU, the actual deal itself has been completed.

This is the main reason we have seen Sterling appreciate significantly so far in 2021 and if the higher forecasts are correct for Sterling against the Euro and Dollar throughout the rest of the year, it could provide a headwind for the UK exporting companies, but as ever, there will be winners and losers.

More importantly than the Brexit resolution though, in our opinion, is the vaccine rollout’s speed and efficiency. The UK health services vaccinated a total of 26.8 million people between 8 December and 19 March with first doses; this equates to half of all adults in the UK, while 2.1 million people have had their second dose of the COVID-19 vaccine so far.

Compared to our EU neighbours, whose vaccination program has been far from efficient, it will allow us to open up our economy much sooner, which you would also expect to benefit us from a GDP point of view.

Current IBOSS positioning

Our other current overweight allocations are in emerging markets and Asia, particularly China, along with UK equities. We are looking to invest in what we see to be the future winners, rather than those of recent years.

That said, it is worth noting that US equities could continue to perform well for some time longer, and we still hold circa 15% in North American assets within the IBOSS Core MPS Equity portfolio. Also worth highlighting is our exposure to US infrastructure, which is an area that will benefit from unprecedented government support.

As markets move into unknown post-pandemic conditions though, we expect diversification to be more critical than ever.

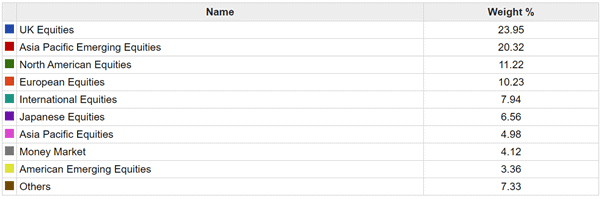

Core MPS Equity Holdings as of 11/03/2021

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information that a proposed investor may require to decide whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise, and investors may get back less than they invested. Risk factors should be taken into account and understood, including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct, but FE neither warrants, neither represents, nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 113.3.21