Growth, value or both?

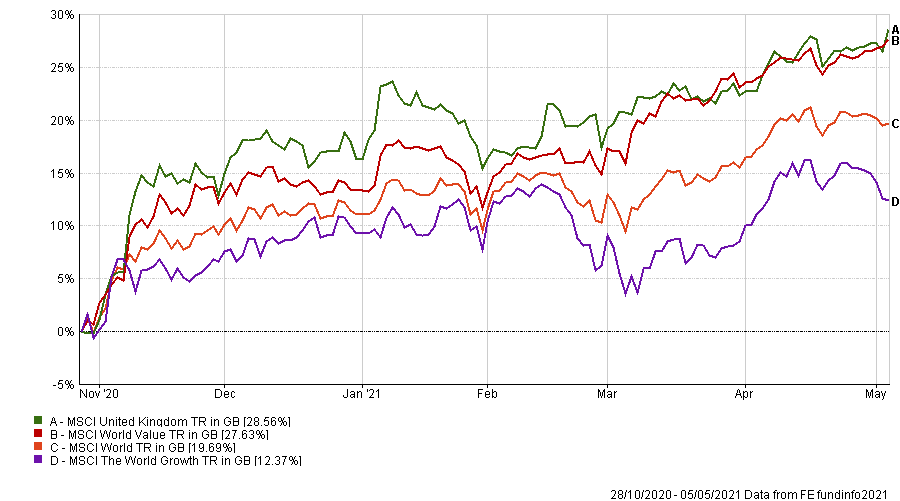

The first three weeks of April saw a dramatic resurgence in growth stocks, but rather than at the expense of value, they were both making solid absolute returns. The last week of April and the first few days of May, however, saw value reassert itself and with it came the continuing domination of UK stocks (fig.1). Some of the most successful growth and momentum styled funds have been hit particularly hard. As an example, the previously prolific Baillie Gifford American fund which is still up over 360% in the last five years fund has lost over 7% year to date and is down over 18% in the last three months against the S&P which is up 7%.

MSCI Growth Vs. Value – 28th October 2020 – 05th May 2021 (fig.1)*

This relatively new phenomenon has still gone somewhat unnoticed in some quarters, but we feel it should have further to run.

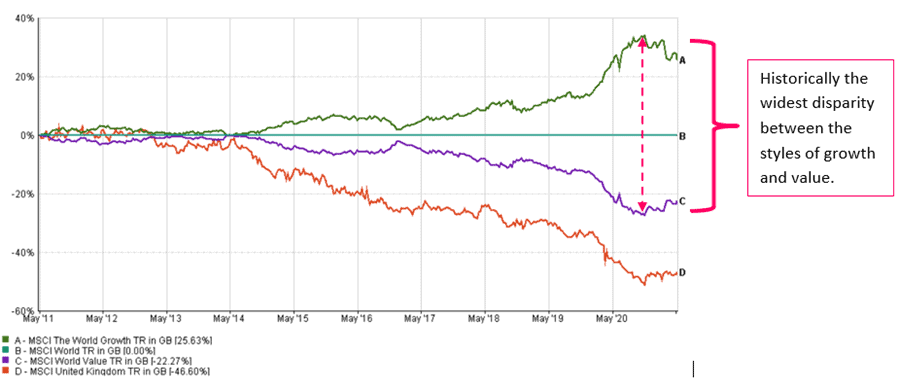

A look at the longer-term date (fig.2) highlights that the reversion towards the MSCI World Index overall of these two styles is reasonably minimal. So, with the successful vaccine rollout by Q3, money printing galore globally and the unprecedented pent up of global demand, we expect inflation and subsequent interest rate pressure to follow in relatively short order.

Though it is never quite as straightforward as this summation might seem to indicate, the overall direction of travel looks to be a reversal of much of 2020.

MSCI Growth Vs. Value – 10 Year Data – 05th May 2021 (fig.2)

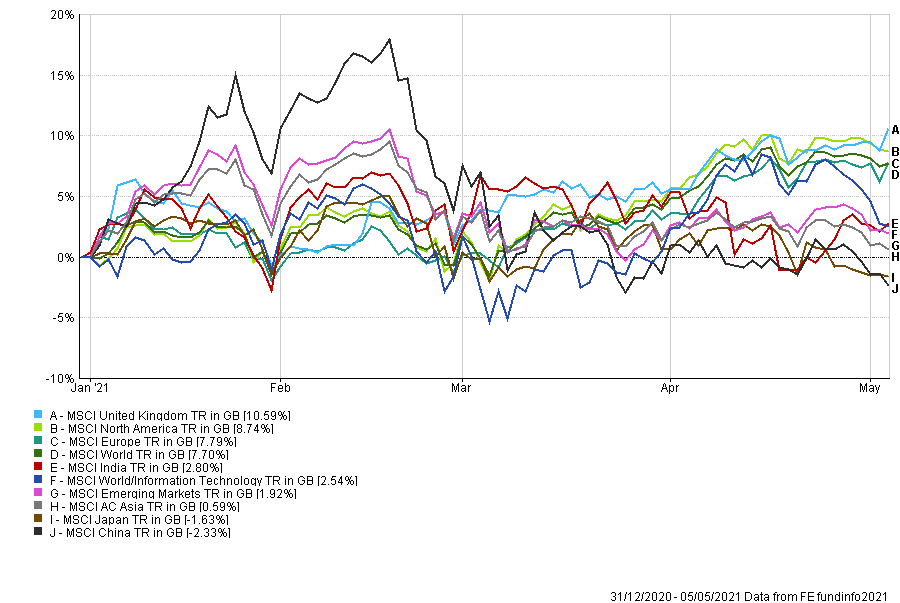

Perhaps the most significant events during April came from the Chinese government when they sanctioned thirteen more of their largest tech firms and reprimanded them for their anti-competitive practices.

Following the earlier high-profile admonishment of Jack Ma’s Ant group, Bytedance, Tencent and JD.Com were amongst the latest group of companies to feel the heavy hand of the Chinese regulators. Not surprisingly, this has hurt the respective stock values (fig.3) and leaves the question about what comes next hanging in the air.

It feels to us that many of the tailwinds for tech companies both in Asia and the US have started to diminish. Many remain well run companies with great products. Still, they are not all going to dominate their respective markets indefinitely, and that leaves considerable downside in their share prices in the event of any bad news. Whilst the US is unlikely to follow the Chinese playbook per se on regulation, anti-trust legislation could prove a vote winner, and therefore it would be unwise to rule it out.

MSCI selected global indices year to date to 5th May (fig.3)*

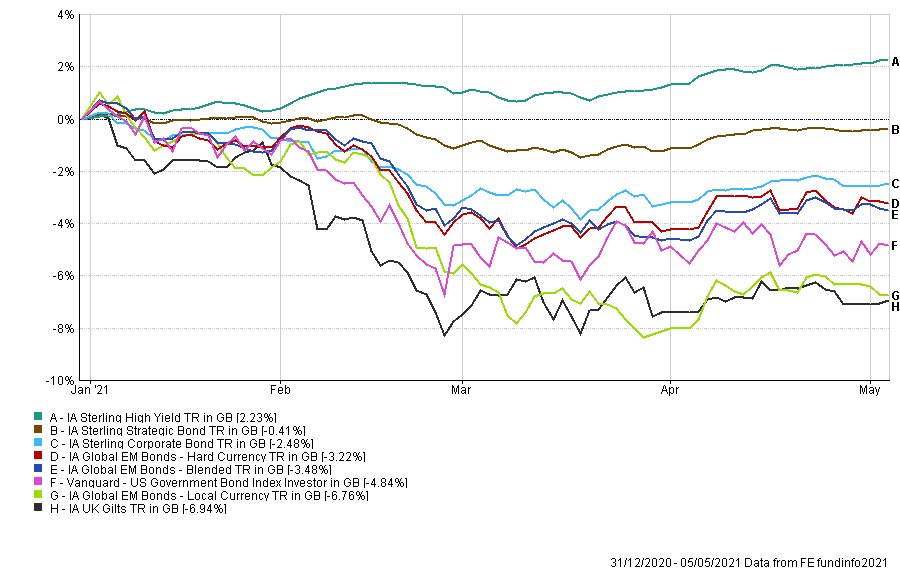

The eye of the storm for fixed income?

In sum, after the rapid sell experienced during January and February this year (fig.4), there has been something of a pause in fixed income market price movements.

IA Fixed Income sectors indices year to date to 5th May (fig.4)*

Only the high yield (junk) sector continued to grind out gains, which inevitably bleeds into parts of the strategic bond sector. What is increasingly concerning is that investors are now getting paid a minuscule amount to hold junk over the respective sovereign; in many ways, the term return-free risk could be made for such a scenario.

We have once again shortened our duration and improved the credit quality in much of our fixed-income holdings. In the event of an equity market sell-off, the high yield sector will almost certainly follow suit, and the current hard-fought gains could be eroded in a matter of days.

The resurrection of the commodity complex

The resurgence of commodities over the last six months has been spectacular. Against the backdrop of a world still reeling from global economic shutdowns and the sometimes deafening ‘ESG now’ mantra from governments, central banks and fund houses it has been some old school sin stocks which have produced the greatest returns.

We believe this trend has further to go and we have brought in our first pure commodity fund for a decade. We have also increased our allocation to funds which can benefit from the new world as it emerges from the global pandemic. Overall, our Core range has a material increase to banks, basic materials and commodities and a reduced exposure to some of the global growth orientated stocks.

In summary, we have sold down some our previous winners to take advantage of a liquidity-soaked global recovery and buy some of the stocks that at this time last year you almost couldn’t give away. Negative oil prices look like a distant memory now, a bit like going to a pub and sitting inside the actual building.

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 155.5.21